Where does management believe PV-10 currently resides regarding the view of the drug by key opinion leaders and the medical community? Early Majority.

In 2011, before Moffitt researchers were paid by Provectus for their pre-clinical work, Moffitt conducted its own unsponsored work on PV-10's immune response. Researchers, following their reproduction of Craig and the team's work, identification of PV-10's quintessential immune response, and the broader and deeper follow-up work, purportedly said (paraphrasing): "We know our place in history."

In 2012, Steven Koevary, Biomedical Sciences and Disease, New England College of Optometry and Department of Cell Biology, University of Massachusetts Medical School, concluded rose bengal (PV-10) may not only suppress ovarian cancer cell growth but also induce their apoptotic cell death, justifying the further investigation of the effects of RB in an animal model of ovarian cancer. He also noted "Thus, even when optimally debulked, many patients still exhibit tumor nodules too small to have been resected by even the most skilled surgeon that likely seed future growths. In light of the above data, it is theorized that injection of these nodules with RB at the time of surgery may prove to be an effective strategy for not only their elimination, but for vaccinating patients against the future regrowth of gross tumors. This notion is supported by data that showed that PV-10 treatment increased the levels of tumor infiltrating lymphocytes and that the overall survival of ovarian cancer patients was greater in patients whose tumors contained T cells." This blog post is here.

It is rumored unsponsored PV-10 pre-clinical work is being done at Rockefeller University, which, interestingly enough, is the first institution in the U.S. devoted to biomedical research. It is rumored several other institutions inside and outside the U.S. are also conducting unsponsored pre-clinical work.

Yesterday's PR of Craig et al.'s poster at SITC highlighted additional data that demonstrated the use of PV-10 in combination with systemic chemotherapy. The combination cancer treatments, whether chemotherapy, radiotherapy or immunotherapy, is a growing theme within the medical community. In the case of the work presented at SITC, PV-10, the immuno-chemoablative therapeutic agent, was combined with a systemic chemotherapeutic.

Pre-clinical and clinical data has shown PV-10 generates immunity even in patients afflicted with very late stage cancer. The immune system, however, can be overwhelmed by cancer (and infections). Management thinks the key, for very late stage disease, is to use a chemotherapeutic or another systemic immunotherapeutic agent (like Yervoy/Ipilimumab) to wound the cancer (the infection) just enough so the PV-10-generated immunity can finish it off. Like antibiotics, PV-10 and the application of other therapeutic agents in this manner (i.e., to wound cancer, before PV-10 finishes it off) would not cure anyone. Rather, they hold or bound the infection until the body's natural immune mechanisms can do the job of curing it.

Next up should be the results of combining PV-10 and anti-CTLA-4 system immunotherapeutic agents like Yervoy/Ipilimumab.

Note the importance of Provectus joint patent application with Pfizer for combining local and systemic therapies for enhanced treatment of cancer. More questions arise: How good were the pre-clinical results from combining PV-10 and Yervoy/Ipilimumab? What would the beneficial impact be on very late stage metastatic melanoma cancer patients from this combination? What would the implications be for Bristol-Myers Squibb, and for Pfizer (which retained the right to certain combinations of therapies with tremelimumab?

This Provectus work foreshadows Moffitt's subsequent murine results, having initially reproduced Craig and the team's work and identified the quintessential immune response: a more complete assessment of PV-10's immune-mediated response, demonstration on multiple cancers and in combination with other therapies, and the durability of the immune response (through various challenge studies).

Ultimately, the “orthogonality paradigm” demonstrates PV-10 is orthogonal to (neither impacted by nor having an impact on) other therapeutic agents. This is important because PV-10 would be used first, second and at all times during patient treatment.

As the events of the week of October 15 fade into memory, do we know more than less?

Peter's sense of value. I was gratified to confirm Peter's valuation expectations during his discussions with prospective financial leads investors like Aisling Capital and OrbiMed Advisors. You will recall I blogged about my thoughts about PVCTP "IPO" terms on September 23rd. I characterize them as "my thoughts," but I think of them as what Peter may have thought/did think at the time. My expectation of the PVCTP share price was too high (he was at $4, while I thought $5-6). I met expectations with the conversion ratio (he was at 1-to-1, and I thought the same) and the warrant coverage range of 40-60%. These parameters suggest a pre-money valuation of $614MM (using a fully diluted share base of 152MM as at June 30) vs. a $96MM pre-money figure using Friday's $0.63 common stock closing price.

Are we clear? Yes sir. Are we clear? Crystal. Peter was clear as crystal about his pricing expectations for the PVCTP "IPO," were he to utilize it for Provectus. That one other person with whom I interacted during that period of time had a good handle on this suggested Peter kept his cards very close to his vest about his discussions with prospective lead investors (other than to repeatedly say he would not do a bad or dumb deal) and angered or frustrated shareholders who could not or did not successfully read or believe him.

Greedy or sabotage? Did certain shareholders try to sink the PVCTP "IPO" purposefully or inadvertently? Earlier this year I wrote a blog post where I calculated (very roughly) Provectus' pre-money valuation before several investment rounds it consummated with institutional and accredited investors, going back several years. My intent was to highlight how I thought management approached fund raising, which was to raise the amount of money they needed for various reasons and ensure there was some cushion of cash available, and no more. The PVCTP "IPO" was, in my view, a much more of a formal raise, where the process of fund raising was as visible and awareness generating as the ticker symbol was to have been. There is no doubt Maxim Group made mistakes and Network 1's Keith Testaverde did Provectus no favor with his e-mail, but did certain shareholders actively push down the stock either to get a more favorable deal (thinking Peter indeed would do a dumb or bad "IPO") or simply kill the vehicle to which they were vehemently opposed for philosophical (?) reasons?

Value is as value does. I think I learned my/a lesson about trying to have a constructive e-mail dialogue with angry longtime Provectus shareholders. Next time, I won't give out my first name. I jest, and I digress. One such shareholder (angry, "long suffering" and, in my view, intellectually inconsistent) thought I must have been smoking something green, white or otherwise pharmaceutical if Provectus would be sold for $50-60 per share. I draw inspiration and cogency from a large shareholder who frames his view on valuation this way (paraphrasing):

If I am dead wrong about PV-10 (i.e., it is "only" a loco-regional treatment), the stock is worth $5.

If I am wrong (i.e., it's got systemic treatment "potential"), the stock is worth $10.

If I am right (i.e., it is a systemic treatment), well then...

While $50-60 per share is the price for which Craig would sell the company, I think he is a pragmatic individual about valuation. He does not strike me as idealogical about this topic. I am sure he, together with Provectus' board of directors and well-heeled financial advisers (Bank of America/Merrill Lynch, not Network 1), will evaluate bids from Big Pharma companies and make the right decision for shareholders and management.

At the same time, the man understands what he has created. And day by day, the world of Big Pharma is catching on to it.

In my head exist many different kinds of trading and investing personalities, because different situations demand different approaches. Those personalities need data and information to inform their decisions. I cannot say with conviction, yet, what I think Provectus is truly worth and for what others would pay. I need more information. I am, however, guided by management's views on the topic, which are informed by others.

Provectus issued a PR today about Craig et al.'s poster presentation at SITC 27th Annual Meeting. I have a lot of blogging to do on this topic this week. The time to progression graphs caught my eye at the outset.

You mention that management believes the company is worth between $7-10 billion. At 113 million shares outstanding, that would indicate a price per share between $62 and $88. Is this plausible?

The figure you should use in the denominator is about 155 million shares fully diluted, which would includes preferred and common shares, stock options and warrants. Using, for example, the 2011 10-K:

3,531,665 preferred shares,

110,596,798 common shares,

14,890,956 options, and

25,119,247 warrants.

$7 billion ÷ 154 million = $45 per share. At $10 billion, $65.

Since there will be a difference between the strike or exercise price and the share price at the time either a stock option or warrant are exercised, as well as cashless exercises features, the total number of options and warrants included in the denominator typically would not be the figures above, but a lesser amount. So, the per share range is a rough estimate.

I think you approach the answer to plausibility in two ways by asking: at what price would management sell, and for what price would Big Pharma pay?

You won't pry the company out of Craig's cold dead hands for less than $50-60. That is the easy answer. If you think you have a/the near cure for a number of cancer indications (and can validate it as such), at what price would you sell?

As for what Big Pharma would pay, I think it ultimately depends on the intensity of the auction. The corporate development or M&A folks at a Big Pharma company will do their respective valuation work to arrive at a range of valuations for Provectus (e.g., Comparable Company Analysis, Discounted Cash Flows Analysis, Precedent Transactions). They will use this (and knowledge about the size of their respective checkbooks) in their discussions with the company, but also in the context of negotiating against other Big Pharma companies interested in buying Provectus. Management's valuation work along these lines informs their own expectations of value.

Why did they need the IPO for a Nasdaq listing if a derm or geographic deal was in the cards? Or the SPA, for that matter?

I think management thought they could secure a NASDAQ listing through the PVCTP "IPO" for the sake of the listing itself: the greater awareness it would bring the stock and company, and the greater accessibility to the stock for a wider swath of buyers. Management had a valuation threshold below which they would not consummate a deal (i.e., pricing) for the IPO. If they got the terms they wanted, they would do an "IPO." If they did not get acceptable terms, they would not do an "IPO," and continue exploring deals for dermatology or oncology in certain geographies. The latter, of course, is what transpired.

You stated in your blog entry that the company doesn't need money save to conduct key clinical trials. I'd characterize that as needing money. They are in a corner. They can't do a smart financing with the stock at these levels, they can't use LPC, and they can't fund the Phase III melanoma. What about this is not a corner?

As at June 30, the company had cash and cash equivalents of $4.1MM. Less total annual cash salaries of $500K per Provectus principal (but neglecting benefits) equals ~$2MM, and less projected fixed costs, and less certain variables costs, equals a positive number through early August 2013.

Management can wait for the SPA to arrive, for certain PH-10 toxicity studies to be completed, for the end-of-Phase 2 meeting for psoriasis, for more Moffitt data to be released or revealed, and/or for other events to occur before striking an average (at worst) to good or great (at best) license deal, whether dermatology or oncology in China, Japan, India or Australasia to garner the monies necessary to fund and run the pivotal MM Phase 3 trial (or having the share price rise to a point where a focused secondary offering might have merit) and other oncology trials. These events should occur within several months or less rather than several quarters or more.

I do not share your view that management is in a corner.

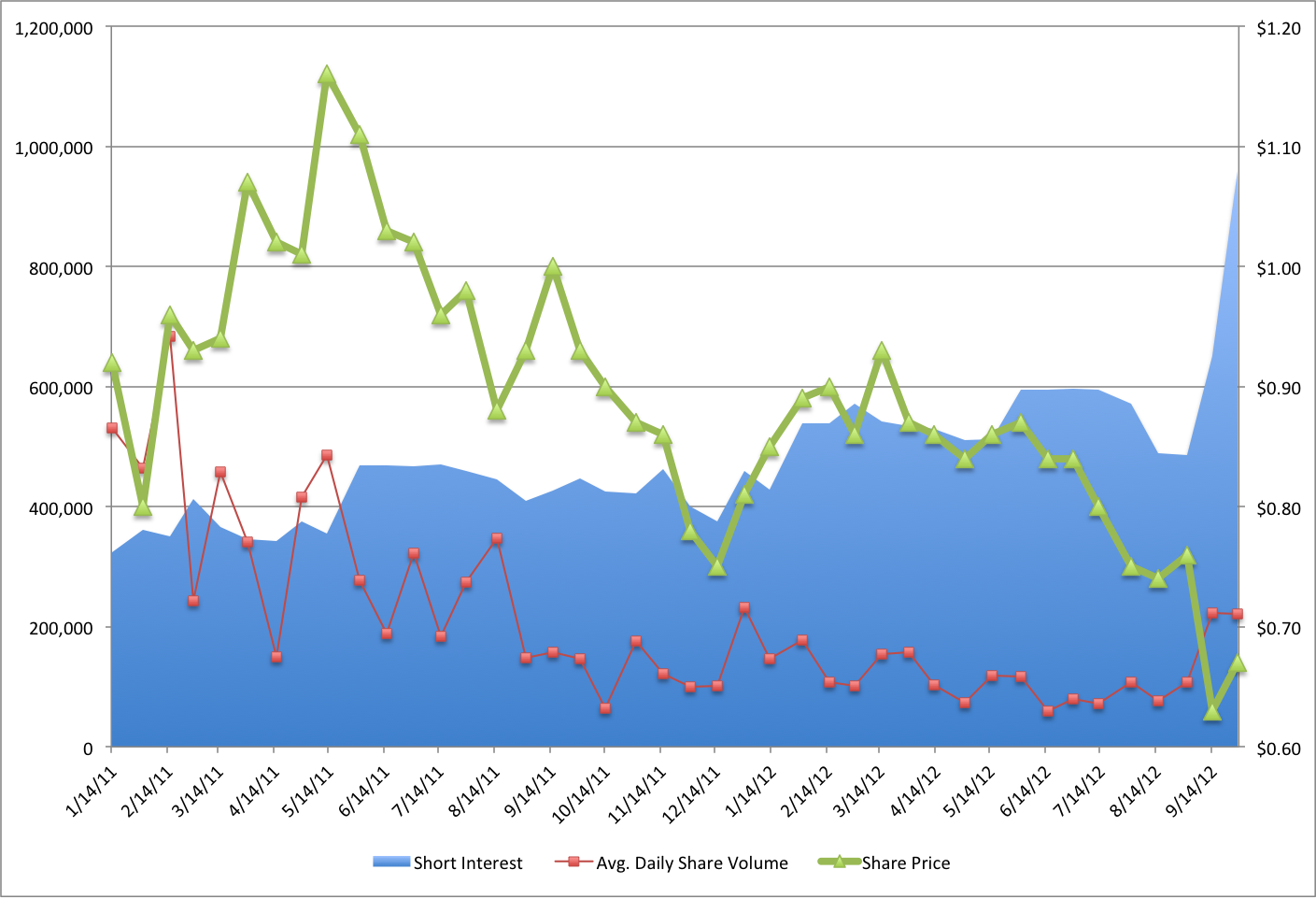

Short interest as at October 15, reported today, was 1,230,229 shares -- up 28% from the September 28 reporting period (959,298), which was up 48% from the September 14 period (650,550), which was up 34% from the August 31 period (486,559). I hope, in a few paragraphs, you will understand why I am framing the short interest this way. See the graph below.

I there there has been a historical "structural short" (i.e., closer to the beginning of the measurement period) of about 400K, give or take, resulting from or necessary for market making activities. The float of the company increased, from about 97MM (12/31/10) shares to 115MM shares (6/30/12) over this time, an increase of about 20%. The structural short figure should have increased in some similar proportion, which I will estimate at 480K.

Management tells shareholders it watches short interest very closely, utilizing a variety of tools including (i) various reports from Provectus' transfer agent, (ii) the SHO list (the Threshold Security List), (iii) FINRA-reported short interest, (iv) DTCC reports and, periodically (v) market intelligence consultants. While they cannot track intra-period period shorting, other than from trade, price and volume behavior, management says it has a very good handle on inter-period shorting when it occurs (i.e., I think they know who's shorting the stock and holding the short when it occurs).

Why has short interest increased since the end of August? Note: The "IPO" supplemental prospectus was made available on September 4.

If you agree with me my assertion of some amount of market maker structural shorting or short interest, an amount equal to or about the amount of short interest at the end of August (i.e., 480K shares), then "active" short of one reason or another should be:

164K shares as at 9/14,

472K shares as at 9/28, and

744K shares as at 10/15.

When asked about short interest as at 9/28 (959K shares), management replied they had a good handle on the reason(s) for this increase -- 472K above the structural short threshold -- but needed 1 (10/15) or 2 (10/31) reporting periods to confirm their expectation(s).

One reporting period has come and gone, and short interest has increased to 744K above the structural short threshold. This represents 270K above the reason(s) management thinks to be the cause(s) of the 9/28 increase.

The "IPO" was terminated on 10/17, with a heavy volume day on 10/18 very likely involving some inter- and intra-period short covering, but we will not have a better perspective until the 10/31 reporting period. There likely will be more, as time moves on and the market understands the company does not need money save to commence pivotal, key and other clinical trial work.

There is a market adage that "dumb money" buys and sells in the morning, and "smart money" buys and sells at the end of the day. Take yesterday, for example. Was yesterday's end-of-day pop short covering? The lack of price action for most or much of the day, combined with the pop at the end, puts into perspective the supposed disgruntled shareholder buyout "rumor." More rumors over the next few days, eh?

I think we will get some additional short covering, but I am not sure how much. If management is right about their thought(s), then true outstanding (or unclosed) shorting is perhaps a few hundred thousand shares (i.e., 270K). If management is incorrect in their initial assertion(s), true shorting probably is much higher (i.e., 744K). Either way, those amounts should be enough to move the share price a few to 10 cents or so.

The 10/31 reporting period will publish on November 9.

At 2010 ASCO, Adam Feuerstein conducted a live online chat at the conference during which he addressed Provectus after viewing their poster. The relevant portions from the chat are below.

Craig's abstract and poster will be presented at the SITC 27th Annual Meeting this weekend. I am very much looking forward to learning what data and information is on the poster. I hope we learn more about:

His bystander mechanism of action work in mice, which should parallell or foreshadow Moffitt's work and their results yet to be released,

Others cancers to which he has applied PV-10 besides melanoma, which should again foreshadow Moffitt, and

Combinational therapies involving PV-10, particularly for very late stage disease and heavy tumor burden.

Why didn't you mention a dermatology deal as a financing option? Do you think that the company, having embarrassed themselves and backed themselves into a corner, will be inclined to quickly ink a deal of some sort? Also, if the drug is so helpful to cancer patients, why don't they sell it to a big pharmaceutical company and get it in more clinical trials?

I previously mentioned a dermatology license deal as a financing option here.

According to management, Provectus does not need money for the foreseeable future (i.e., into August 2013), save to conduct pivotal, key and other clinical trials. Proof of this should be available to confirm or refute around early-November when the 10-Q is filed and available. As such, I do not think management views themselves as backed into a corner. They are keenly aware of what PV-10 and PH-10 are worth, and will strike deals accordingly. The PVCTP "IPO" was primarily about securing a NASDAQ listing, and obtaining money only at the right price and terms.

Management certainly wants to get the drug into the hands and bloodstreams of as many cancer patients as they can. An acquirer like Pfizer would very likely immediately commence multiple clinical trials to expand the number of indications to which PV-10 would be applied. At the same time, however, management understands the next several quarters are about further demonstrating the size and scope of PV-10's applicability to secure the $7-10 billion they believe the company is worth and the $3-4 billion they expect as an upfront payment in the end-game.

Most rumors I hear are not remotely close to being true. There is not even a grain of truth in them, which all good rumors typically possess. If interesting and germane, I try to confirm the substance of a good rumor with separate and distinct shareholder groups with whom I communicate (the PVCT "town" is a small one). I solicit feedback from management, too.

An interesting rumor, from several perspectives, is the one I heard today: a certain group of shareholders is interested in taking/will take Provectus private (i.e., a buyout) at $3 per share. Management is aware of the situation.

I am very skeptical for several reasons including but not limited to:

I doubt this group or, for that matter, any syndicate or group of existing Provectus shareholders owning a large number of shares can pull this off.

You have to wonder if you and I will hear more of this kind of talk, whether out of frustration with management or simply to pump up the share price on helium in order to close or in hopes of closing out a share position at a lesser loss.

Give or take the number of shares this group might own, a buyout at $3 would price the company at about $400-450MM. That is a lot of cheese for a group of existing shareholders.

The journey to a buyout begins with several initial steps. Typically, one starts with at least a 5% ownership or thereabouts. Revelation (formerly Osmium) was the last entity (actually, the only entity, not counting Dr. Adams) to file a beneficial ownership greater than 5%. The filing was a passive one. Their investment style/strategy was/is event driven. They are not activist investors. And we have not heard from them in quite a long time.

From a 5% position, a shareholder (or group) could either agitate for change or launch a full blown tender for shares (among other things it or they could do). Unless a buyout group -- whether a cadre of existing shareholders or prospective new ones -- has the real ability to manage the science, regulatory and science communications processes here, among other necessary and needed experience sets to take the company to the end-game, the notion of buying the company for $3 and "flipping it" to Big Pharma is just fanciful.

A more interesting scenario develops if Pfizer or another Big Pharma currently watching the company closely fears a move towards a buyout would forclose the opportunity for them (PFE or another Big Pharma) to buy Provectus. Rumors or hints of a buyout might provoke Pfizer, among others, to act. While you should not hold your breath, it is worth paying a small bit of attention to see if anything more develops.

I had a very nice e-mail exchange with another share holder, which inspired this post. It might help to simplify the situation, as least the simplicity I see.

The drug works. While getting the drugs approved and bringing them to market are of course no small feats, I think, now, a sufficiently large number of key opinion leaders are on board with how good these drugs are and can be.

Get the SPA. The SPA defines the approval path for PV-10 for a focused label.

Get the funding. Management must consummate either a smart financing or a good geographic license deal to fund the pivotal MM Phase 3 trial.

Get the interim analysis. The interim analysis from the MM Phase 3 trial should be a major but not exclusive step to sell the company.

I asked a lot of questions this week of and also did a lot of listening to management and fellow shareholders. My takeaways:

The IPO appears to be off the table for now. Provectus did not come to terms with a(the) lead investor(s) on pricing and others terms. Thus, management terminated it. Ultimately, their approach to this process was consistent with my expectations of it.

Check to make sure you still have your ring, watch and wallet if you ever visit Maxim's offices.

More seriously, after learning of/hearing the conversations of many shareholders with Maxim executives and institutional and retail reps, I think Peter did indeed treat Maxim folks like mushrooms: he fed 'em s@$% and kept 'em in the dark. As such, Maxim's "alleged" behavior reverted to the mean during the terminated "IPO" process. He could not control their behavior and actions; however, some mud remains on Peter's trousers because of it.

The opportunities for PV-10 and PH-10 are bigger than ever. Frankly, to understate the obvious, management knows more about how well the drugs work than you and I do. Breast cancer anyone? Just sayin'...

I would like to see what more information emerges on several fronts next week and through October 31.

Dr. Stephen Maturin: They're exhausted. These men are exhausted. You've pushed them too hard.

Capt. Jack Aubrey: Stephen, I invite you to this cabin as my friend. Not to criticise nor to comment on my command.

Maturin: Well, shall I leave you until you're in a more harmonious frame of mind.

[he stands and is about to leave]

Aubrey: What would you have me do, Stephen?

Maturin: [turns back to him and knows what to say] Tip the ship's grog over the side.

Aubrey: Stop their grog?

Maturin: Nagle was drunk when he insulted Hollom. Did you know that?

Aubrey: Stop 30 years of privilege and tradition. I'd rather have them three sheets to the wind than face a mutiny.

Maturin: You see I'm rather understanding of mutinies. Men pressed from their homes, confined for months aboard a wooden prison...

Aubrey: I respect your right to disagree with me, but I can only afford one rebel on this ship. I hate it when you talk of the service in this way. It makes me feel so very low. You think I want to flog Nagle? A man who hacked the ropes that sent his mate to his death? Under MY orders? Do you not see? The only things that keep this wooden world together are hard work...

Maturin: Jack, the man failed to salute. There's hierarchies even in nature. There is no disdain in nature. There is no...

Aubrey: Men must be governed! Often not wisely, but governed nonetheless.

Maturin: That's the excuse of every tyrant in history, from Nero to Bonaparte. I, for one, am opposed to authority. It is an egg of misery and opression.

Aubrey: You've come to the wrong shop for anarchy, brother.

After discussing this with a large shareholder whose opinion I respect and often seek, I think the share price should move at least into the $0.70s tomorrow and perhaps as high as the $0.80s. The latter price level is where the stock resided in late-spring and early-summer.

We should see short covering specifically related to the driving down of the share price in anticipation of an at market conversion ratio for the "IPO." I do not think short interest is as high as many folks think when adjusted for historical shorts positons related to market makers and a temporary or structural short in September that should go away in October. Short interest related to the "IPO" likely is in the 500K to 1MM share range.

There also may be some sellers remorse (i.e., those who sold because of the share decline might buy back some or all of their holdings).

There is much to which to look forward. Looking back:

The finance industry can be the valuable grease that enables the gears of the global economy to operate more efficiently and effectively. A piece of the industry also is a cesspool. Investment banks, white shoe, boutique and, er, other, have bet against their clients since time immemorial (okay, that is hyperbole, but you get the idea). The "good" banks are not obvious about it. If you are going to bank Provectus (i.e., if you are going to provide, in this case, investment banking services like IPO underwriting and equity research coverage), could you not be more discrete about the other part of your bank trying to drive down the share price (for the betterment of prospective "IPO" buyers)? Allegedly, of course.

I have asked the company to open an investigation into the illegal solicitation (i.e., sell recommendations or "suggestions") and shorting of Provectus common stock: Claims of illegal recommendations by certain Maxim executives and retail reps to existing and prospective clients to (a) sell their common stock and/or (b) short the common stock in order to (c) profit from the subsequent share price decline and (d) ultimately benefit from their participation in the "IPO" from enjoying a better conversion ratio resulting from the premeditated driving down of the share price. There are undoubtedly much more productive uses of company time, resources and dollars; however, at a minimum, I hope FINRA knocks on a few Maxim doors.

The PVCTP "IPO" process hurt management's credibility.

Management's decision to terminate the offering helped its credibility.

Bidirectional bridges between shareholders and management should be redesigned and then rebuilt.

I think it is a little bit interesting Adam Feuerstein tweeted about the company. His intimation of "Um...," to me, for now, merely is as a very casual observer of Provectus, but certainly within his purvey as a biotechnology industry journalist.

Data points, nevertheless, are important to collect. Data, data, data. People are paying attention.

Over the course of my many discussions with shareholders today, I have encouraged all of them to share their views about the PVCTP "IPO" and, what appears to me to be, an attack on the common share price with Peter. I have shared my own thoughts with Peter multiple times today, as well as many times prior to today.

I have heard from multiple non-company sources that an "IPO" will not be done at these share prices, if one is done at all.

There has been the feeling by some (experienced Wall Street veterans) that either or both of Maxim Group and Network 1 Financial have been "double dealing:" working with Provectus in appropriate, necessary ways to facilitate the "PVCTP" IPO, while at the same time (in other areas of the respective firms) contributing to driving the PVCT.OB share price down for the benefit of firm clients (the math here is simple: if these firms assume Pete will agree to an "at market" conversion ratio, the lower the common stock share price at "IPO" pricing [if the "IPO" goes off], the better the value proposition for the preferred stock).

In the case of Maxim, as lead underwriter of the PVCTP "IPO," Paul LaRosa, Executive Managing Director - Capital Markets, works with Pete in this regard. See my previous comments here.

At the same time, Maxim's retail side appears to have been tasked to seek 300+ prospective buyers (since the key NASDAQ listing requirements are a $15MM raise, minimum $4 per share price and 300+ round lot holders). There have been no pricing or other details for the "IPO," because, according to Peter, these parameters continue to be worked out between prospective investors and him. Maxim retail reps have been telling folks, allegedly, the "actual details" of the IPO, which appears to have contributed to the downward pressure on the common stock.

Have other parts of Maxim been talking down the stock down or facilitating its drop? Communications from Leonard Greenbaum, Maxim's Managing Director - Equity Derivatives, to Dr. Adams appear to indicate such activity or behavior:

Beginning last week, Mr. Greenbaum appears to have advised the initial sale of common stock (of an existing position) as soon as possible to avoid further losses because the share price was falling rapidly. It appears he also suggested taking an aggressive short position concurrently to take advantage of the greater share price decline Mr. Greenbaum believed was to come because the lower the price of PVCT, the greater the benefit to the eventual holders of PVCTP. It appears he also concluded all existing shareholders had the opportunity to participate in the "IPO," so this was fair.

Share your Maxim stories with Pete at pete@pvct.com. Please be accurate, and document as many details as you can.

One of my most vivid capital markets memories was of my first introduction to market expectations. It was a Friday morning during late autumn, and I was sitting on the T-bill desk of a bank trade floor. As an apprenticing trader for this bank, I went through rotations on different product desks. It was non-farm payroll Friday. Chatter quieted to murmuring and then became silence as the clock approached 8:30 am EDT. At the designated time, non-farm payroll data burst across the newswire. The number greatly exceeded the consensus figure by (I think) several hundred thousand. As far as I can recall, the number caught nearly everyone by surprise. Traders and salespeople on a floor that housed hundreds of employees reacted differently (much more, more or less animated, or not at all) depending on how their respective books were positioned in advance of the number in accordance with their belief of whether market expectations were going to be exceeded, met or not met. The traders on the interest rate derivatives desk, where my eyes were fixed at the time, were jumping up and down, high fiving one another and slapping each other on the back.

Friday, ironically, cannot come soon enough. The negativity or negative energy I have experienced and felt since the beginning of the PVCTP "IPO" process is unproductive. There is so much to the science of and patient benefit from rose bengal and PV-10, and to the stock and its eventual purchase by Big Pharma that I wish to blog more about. The last several weeks seemingly have stolen attention (understandably) from more interesting, more substantive topics.

The market anticipates, generally speaking, a PVCTP "IPO" at company unfriendly terms (i.e., expectations). Potential outcomes for Friday essentially include:

A PVCTP "IPO" at company friendly terms (e.g., $15-20MM raise, a 2-to-1 or lower conversion ratio, 50% warrant coverage). The market does not expect this;

A PVCTP "IPO" at company unfriendly terms (e.g., $15-20MM raise, an at or near at market conversion ratio [i.e., 6- to 8-to-1], 50% warrant coverage). The market expects this and is pricing some or most of it into the current share price; or

The PVCTP "IPO" is killed. The market does not expect this.

Should #1 or #3 occur, the common stock share price would jump higher to varying degrees (#1 > #3) on Friday, and ascend next week.

If #2 were to occur, I think any initial sell-off of the common stock (presumably or likely by retail investors) eventually should turn into an upward move later (J-curve effect) because the presumption of the "IPO" is a steady stream of news and media awareness following its launch (and the spectre of the punitive effect of the "IPO" on the common stock will have disappeared).

While it is possible we may repeat whatever this is one more week, this Friday cannot come soon enough.

We may have a much better perspective on the "IPO" and others things Provectus sooner rather than later. There seems to be a convergence by the folks who make-up the PVCTP book running group -- American Trust Investment Services, Maxim Group, Network 1 -- pointing to the end of this week for the "IPO," if it happens: Thursday afternoon pricing, Friday morning trading. Update (via Maxim): Terms would be released, if a deal is consummated, after 4 pm EDT on Thursday.

We know what the market anticipates the terms to be. The question is: what will they actually be?

Fratres! Three weeks from now, I will be harvesting my crops. Imagine where you will be, and it will be so. Hold the line! Stay with me! If you find yourself alone, riding in the green fields with the sun on your face, do not be troubled. For you are in Elysium, and you're already dead! Brothers, what we do in life... echoes in eternity. -- Maximus Decimus Meridus in Gladiator

I want to:

Share my speculation about what I think happened towards the end of the third quarter and how it relates to the temporal nature of the PVCTP "IPO,"

Explain why I will invest a token amount of money in the "IPO" if it happens, and

Write about management's poker hand, the hand they have dealt shareholders, and how both of them might be played.

I think management was convinced the SPA would arrive by the end of Q3 and the PVCTP "IPO," which was supposed to have been in the right place at the right time, was being teed up to follow it.

As we know, Provectus and Peter have been working several financing options:

The "IPO,"

A dermatology license deal,

One or more geography-specific oncology license deals, and

A strategic investment from a Big Pharma entity like Pfizer as the sale of common stock at a premium to the share price (or, as mentioned above, an "IPO" led or co-led by a Big Pharma company).

Each of these has its own value proposition (i.e., pros and cons), but the propositions are temporal, having greater or lesser value as a function of time.

For example, the best option today for shareholders would be an optimally valued (i.e., net present value) and structured (i.e., upfront, milestone and royalty payments) dermatology or geographic-specific oncology license deal yielding an upfront payment sufficient to at least pay for the pivotal MM Phase 3 trial. Optimality, however, might be more likely to be achieved later rather than sooner, in November or December.

A sale of common stock to a Big Pharma company would be "more optimal" if the price at which these shares would be sold was much, much higher than Friday's close of $0.59, like at least $4. But why approach or ask a Big Pharma company like Pfizer for this kind of strategic investment unless you have or need to ask? In my view you ask after the SPA is in hand and if you determine (a) the PVCTP "IPO" is not feasible and (b) dermatology or mini-oncology optimality is later rather than sooner.

Up next is the PVCTP "IPO," which, for a certain period of time, provides attractive and pragmatic ways to begin driving company valuation dramatically upwards:

Attractively: A NASDAQ listing would facilitate new buyers, who could not buy the common while it remained an over-the-counter stock, and more national media attention from major journalists and reporters, who would not cover Provectus until it traded on a major stock exchange and was in Phase 3 trials.

Attractively: A smart IPO, led by Pfizer (and J&J or a life sciences investor like OrbiMed) and with a conversion ratio and warrant coverage good for existing common shareholders, would draw many more new buyers to the preferred stock listing itself over time.

Pragmatically: A $15-20MM raise at an acceptably high valuation, while creating dilution that a dermatology or a so-called mini-oncology license deal would not, fully funds the pivotal MM Phase 3 trial. There would be no need to force or rush dermatology or oncology deals, nor completely rely on them to commence the MM trial. The trial could start within 30 days of the SPA PR and move Provectus and its shareholders closer to the interim analysis of at least the first half of the trial's patient population.

A smart PVCTP "IPO" is a better temporal option in October than a dermatology or mini-oncology license. In November, it might not be.

Back to the SPA PR. It was the first domino to have fallen in a hoped for series of them, whether the next temporally best one was a license deal or the "IPO."

But the SPA did not arrive by the end of September, despite very ernest and serious expectations set to the contrary by folks directly interacting with the FDA. It is coming, but it was not nor is not here yet.

To compound these missed expectations were:

Shorting of the stock (end-of-September short interest was nearly 100% greater than the end-of-August figure) for whatever reason(s),

Selling of shares (September's monthly amount of traded shares was nearly double that of August's) for whatever reason(s), and

The PVCTP "IPO" process, and particularly the aspect undertaken by Maxim Group's retail banking side.

Th "alleged" sloppy "IPO" process was made much more so by "alleged" disgusting behavior by some Maxim retails reps spreading baseless "facts" about the "IPO's" details. I used "alleged" because, while Paul LaRosa from Maxim's capital markets part of business agreed Maxim reps should not have been saying what they were saying, the reps themselves probably would say they were doing nothing wrong. "Alleged?" I crack myself up.

The rep revenue model is predicated on the number of transactions they encourage and facilitate. The revenue model is not based on asset appreciation.

I now have what I think is a better handle on the increase in short interest, and will wait until October reporting dates to confirm this. In the interim, am I concerned? No. Am I annoyed and irritated? Yes.

There is the thought one very determined seller has been and is getting out of the stock. Could he/she/it have thrown in the towel for whatever reason(s)? Most likely yes. Does he/she/it know something we do not? I am betting my share ownership (note: no sales of any shares bought) the answer is "no."

Funds holding Provectus preferred and/or common shares have much different pressures than entities and individuals. The quarter-to-quarter reporting to investors and limited partners funds in this group (as opposed to a venture capital or private equity fund) are required to provide make it difficult to hold to an investment thesis because of complaints of poor performance by these very investors and LPs. Such theses turn into trading ones, if they did not start out as such. Did someone's patience runout? Probably.

So, here we are today, observing an IPO that keeps getting pushed out, from the week of:

October 1st to

October 8th to

October 15th to, likely,

October 22nd.

While the preferential path to financing might be a dermatology deal, the "IPO," for the reasons I presented above and others, is temporally better. I think, however, it needs an SPA PR to launch it, and I do not see the "IPO" occurring until after an SPA PR is issued. As such, if the "IPO" does not occur in October, management will probably pull the plug on it because other financing options would have become temporally better.

2.I got your initial public offering RIGHT HERE! (w/gesture)

If the PVCTP "IPO" goes off, I will participate in a very small way. I prefer buying common stock.

I work hard to maintain an objectively dispassionate investment case to buy and hold Provectus stock, but I am not always successful as emotion does creep in from time to time. I have an emotional attachment to this situation. Seriously folks, who blogs this much about one company or stock if they are not part of it? Participating in a token way in the "IPO" is something to add to "the box" that holds the collection of my life memories.

Emotion aside, however, the ROI from buying common stock should exceed the ROI of buying preferred stock (when compared together and presented as a choice of whether to buy the "IPO" or spend the equivalent amount of money buying the common stock), irrespective of what a Maxim retail rep tells you. Of course, you could always trust Chris Varick.

Let us make some assumptions to frame this analysis -- and please let me know if you disagree with my work below (as I am open to feedback and being corrected). I will toggle these later under certain circumstances to make some illustrative points. Nevertheless, the key assumption underlying my belief of a better common share ROI is that Provectus will not do a dumb IPO.

Let us assume you have $100,000 to either spend on the "IPO" or just buy common stock. In this analysis, you cannot buy both. Furthermore, since you do not know if and when the "IPO" goes off, you have to make a reasonably timely decision: wait for the "IPO" to happen or buy common stock before the SPA PR is issued. The SPA, which management surely knows they now have, should not affect the terms of the "IPO" but should increase the price of the common stock post-announcement.

Do you buy the "IPO" whenever it goes off, or do you buy common stock, say, starting Monday?

I assume about 150MM fully diluted number of shares of non-listed preferred and common stock, stock options and warrants. PVCTP deal terms then suggest some more shares. "As converted" means I used the conversion ratio above (i.e., 1) to convert the PVCTP shares and warrants on PVCTP shares into the appropriate but requisite number of common shares.

On an as converted basis, your $100,000 gets you (a) 35,000 PVCTP-derived common shares or (b) 166,500 common shares.

Let us assume the company is acquired for, among other things, a $1B upfront payment (i.e., the preferred shares you bought when converted into common stock or your common shares you bought are exchanged for your pro rata share of $1B) on December 17, 2013. Let us also assume the IPO still happens: you either participated in it, or you bought common shares and did not. I make this assumption only to simplify the analysis in some ways. If you buy common stock and the IPO does not go off (i.e., it is November and Provectus completes a license deal), the fully diluted shares outstanding figures remains at $150MM and your common stock ROI is higher.

Let us also assume you convert & exercise/sell your preferred shares and warrants, or your common stock, when the acquisition transaction occurs.

The outcome makes sense. A smart IPO implies a healthy valuation at which PVCTP "IPO" shares were sold and, thus, a substantial uptick (about an order of magnitude) from today's market capitalization. Under this scenario, one should of course buy the common stock, say, starting Monday, then wait and buy the IPO.

Hold on a second! Didn't your stock broker, er, Maxim retail rep "allegedly" tell you to flip the preferred shares and hold onto the warrants as "a lottery ticket?"

The flipping-your-preferred-shares ROI is less than the hold-your-preferred-shares ROI, which should be much less than the buy-common-stock ROI.

Maxim's "alleged" story only works -- that is, you make out like a bandit by indeed cashing in a lottery ticket -- if the conversion ratio and, to a lesser extent, warrant coverage is very punitive to existing common stock shareholders, such as 6- or 7- or 8-to-1 and 60%, respectively. That is, the "IPO" is a dumb "IPO."

A 2-to-1 conversion ratio (and, say, 50% warrant coverage), worse than my initial example above but far from punitive more than doubles your return from buying the "IPO;" however, one makes more money, again, by just buying common stock soon.

To be fair, a dumb IPO produces a result where buying PVCTP and eschewing the common stock is the better course of action.

3."Poker is not a game of cards played with other people, it is a game of people played with cards."

Right now, Provectus only needs money to literally keep the lights on and the water running (note: hyperbole). Fixed costs are low. The burn rate can be turned down and compensation deferred, with a focus on those activities, and whatever variable costs are associated with them, that drive value (e.g., the end-of-phase 2 meeting with the FDA for psoriasis, remaining toxicity study parameter elucidation, etc.) until money targeted for key, pivotal and other trial work is raised or obtained.

In this game of poker, management will play the hand they think they have the way they see fit. I think:

The company's hand is very strong,

Management thinks the hand is a royal flush (I think the hand is a royal flush, too),

Provectus has enough chips (cash on hand, and temporal cash needs) to play it well, and

Management will play it well (i.e., not raise money in a dumb way).

I am betting my share ownership on this. Of course, I could be quite wrong (note: the usual economist's conviction of "on the one hand, ..." but "on the other hand, ...," which is why we need more one-armed economists).

Now, what kind of poker hand do you think it is: a straight flush, four of a kind, a full house, worse or one that can be beaten? Which hand you have is up to you to determine. How you play it also is up to you.

There is no doubt of the battering the share price has taken since the beginning of September, let alone this year or over the last several years. I see it. I feel it. I understand it.

You got to know when to hold 'em, know when to fold 'em, Know when to walk away and know when to run. You never count your money when you're sittin' at the table. There'll be time enough for countin' when the dealin's done.

The company needs money, but not in the way the markets and most observers think Provectus does. Management has indicated they will do a smart IPO if they do one at all, and that raising money below $1.12 is not in the cards (pardon the pun). Anonymous wrote "[p]oker is not a game of cards played with other people, it is a game of people played with cards."

Playing your poker hand requires you to ask yourself how management will play their hand.

Disclaimer:This blog is neither intended to be nor is investment advice. The author of this blog (the "Author") is not a registered investment advisor. Under no circumstances should any content from this blog be used or interpreted as a recommendation of a trade or investment in Provectus Pharmaceuticals, Inc. Trading and investing can be hazardous to your wealth, health or both. Any investment decision must, in all cases and without exception, be made by the reader or by his or her registered investment advisor. This blog is only and strictly for educational and informational purposes. The Author may have a position in Provectus Pharmaceuticals, Inc. at any given time that is not disclosed at the time of publication. All opinions expressed by the Author are subject to change without notice. You, the reader, should always obtain current information and perform the appropriate due diligence before making any investment or trading decision. All efforts are made to ensure the information contained in the blog and/or a blog post is factual and accurate; however, the Author does not guarantee its accuracy under any circumstances.

Much to Maxim Rep #6's credit, he eventually facilitated a call for me with Paul LaRosa, Maxim's Senior Managing Director of Capital Markets. Paraphrasing:

There was no deal in place.

He had taken Provectus management on a roadshow to 30-40 prospective investors.

Such investors would negotiate terms with the company.

They would meet somewhere in the middle (my note: an illustrative comment), and a deal would be struck.

A final prospectus with detailed terms, numbers, etc. would be circulated a day before the PVCTP security would trade (update: final terms, however, more than likely would be socialized with prospective "IPO" buyers to provide enough time to understand deal terms and the like).

Maxim retail reps should have not been saying what they were saying.

Thought: PVCTP "IPO" pricing has not yet been established.

Non-Thought: Maxim Rep #6 said (paraphrasing) his earlier comments on the call regarding an "at market conversion ratio" as a definitive deal term was hypothetical and he did not know what the conversion ratio was or would be until it was told to him. I said (paraphrasing) I appreciated these latter comments. He must be new to the financial services industry and the Maxim retail desk.

Non-Thought: This same rep said (paraphrasing) Peter told him the conversion ratio was "at market." When pushed on the veracity of such a claim, he said (paraphrasing) Peter implied it to him. When asked for an e-mail of this be sent to me, none arrived. When he offered to set-up a call first this in the morning with the capital markets/investment banker point person on the deal and I said (paraphrasing) "Please do," no call thus far has materialized.

Non-Thought: According to Maxim, the PVCTP "IPO" appears to have been pushed off to the week of October 15. Non-Thought: Maxim Rep #4 empathized with me as a common stock shareholder by saying (paraphrasing) he too felt saddened or aggrieved that "others" were suggesting selling the common stock to buy the preferred stock. An important aspect of customer service indeed is to empathize with a prospective client.

Thought: According to several sources, Maxim has secured the necessary 300+ prospective "IPO" buyers for the security to be listed on the NASDAQ. This item is important because, aside from establishing the appropriate deal terms for the PVCTP vehicle, the confirmation enables Peter to know whether Provectus can indeed use this financing approach if the board and management chooses to do so.

Thought: You will recall management has not raised money through common stock or warrant issuances below $1.12 for some time (I should get around to listing such information in a subsequent post in a few days). Raising money at or above this level for philosophical (they have drawn their own line in the sand on this issue) and mechanical (there are several warrant reset provisions for fundraising common stock share prices below $1.12 and other price levels) reasons is important to them. Thus, doing an "at market" conversion ratio, or a ratio utilizing a common share price below $1.12 and/or issuing warrants with exercise prices (when the exercise price of a warrant on a share of PVCTP is translated into a common stock exercise price) below $1.12 would be contrary to management's current position on fund raising, go against recent historical actions and have a significant impact on the overal capital structure of the company.

Thought: In the month of September, Knight Capital (NITE) appears to have been responsible for less than 25% of traded shares. If, as has been speculated on PVCT stock chat rooms and elsewhere, Dr. Adams' shares are transacted through NITE, more than 75% of selling (and buying) was by folks and entities other than Dr. Adams. I am not focusing on the amount of shares, since there is thoughtful commentary that volume statistics for over-the-counter stocks are much higher than commonly reported (perhaps by as much as half), but rather the relative proportion of transactions.

Thought: I previously expressed my thoughts about the "IPO" to management. In communicating my view on its pros and cons, Peter clearly indicated to me he would take a thoughtful approach to a PVCTP "IPO" (if the company were to use it). I take him at his word until and unless his word, in my view, is not worth taking any more.

"Researchers at Moffitt Cancer Center and colleagues at the University of South Florida and Tianjin Medical University Cancer Institute and Hospital in China have discovered that combining chemotherapy drugs and immunotherapy cancer vaccines results in an enhanced anti-tumor effect." Article here. Abstract here.

This is a corollary to Moffitt's work with PV-10. In connecting several dots outside the company, I will speculate Moffitt could very likely seek an oral presentation of its ground-breaking PV-10-related immunology work at the annual meeting of the American Association of Cancer Research in April 2013.

Short interest through September month-end (click on the chart to enlarge it) is below. Short interest is up nearly 100% month-over-month (i.e., September month-end over August month-end). The prospectus supplement related to the PVCTP "IPO" was filed with the SEC on September 4. There would appear to be some shorting in advance of the preferred stock offering.

A PVCTP "IPO" offering done in the right way – led by strategic and/or financial investors at company friendly terms and conditions closer to or approaching my September 23rd blog – can be a very constructive way of increasing shareholder value in the near-, medium- and long-term. No pricing has been established yet, so there is no likelihood of a closing this week until management determines if and how it would price and utilize the preferred stock offering. Disregard Maxim retail reps for the time being.

I have been gathering data, developing information and gaining knowledge on several items, which I will blog about after the PVCTP hubbub either has been resolved or dies down.

The reps on Maxim's retail desk continue to call around with details of the upcoming PVCTP "IPO:"

At market conversion ratio (i.e., 6-7 to 1: 6 or 7 common shares are received when 1 preferred share is converted),

40-60% warrant coverage (the warrants will remain with the "IPO" participants, so one could sell one's PVCTP shares and still retain upside while making a profit if one flipped one's PVCTP shares after the "IPO"),

etc.

Maxim's retail desk is separate from their investment banking side (the folks working with Peter as underwriters of the "IPO"), so the reps do not have specific deal terms to inform prospective investors they are calling.

Management may not ultimately utilize PVCTP, but these retail reps are sharing the above details and more with certainty.

Deal terms are circulating around Wall Street, in Connecticut and elsewhere.

Some of Wall Street's denizens are paying attention to the situation; the ones who look to turn a quick buck, and have little to no interest in Provectus' long-term story.

A buck is a buck, and their short the common-and-cover through a conversion of the preferred is a viable trading strategy.

My feelings about the strategy, as a large shareholder, are immaterial. It has worked in the past, and it will work in the future.

Should management not go through with a PVCTP "IPO," and I think the probability of an "IPO" has materially lessened, there will be a short-covering rally. Until then, continue to gird yourselves.

When do you now expect the FDA issues an SPA to PVCT?

Do you have any other insight into a possible dermatology deal and/or regional oncology JV? The pressure on the stock due to a lack of clarity on the financing to go forward and announcement of an SPA can at times be very unnerving.

Do we now have the "investors" in the preferred shorting the ____ out of the common for a better conversion rate? A low price helps only the person buying the preferred shares.

It really seems a moment to consider cutting your losses. My confidence is seriously waning. SI poster

The above is a sampling of what I have received recently via calls, e-mail (directly to me or through i.am.a.pvct.investor@gmail.com) and the blog. As much as readership statistics clearly indicate growing interest in and awareness of Provectus and PV-10 (a great thing taking the long-term view of eventual price appreciation), in the short-term increasing numbers of comments such as these anecdotally suggest shareholders feeling more and more unnerved and lost.

These emotions are natural. You feel them when you are considerably underwater in your share cost basis, cannot easily foresee the path forward for the share price to higher and loftier levels, and feel insecure in your investment or trading thesis of the stock.

Proponents and practitioners of behavioral finance would suggest now might be a good time to begin buying the stock. But that will not make some of you feel better.

There is selling: The simplest reason for the drastic drop in the share price is there are more sellers than buyers. Sellers, whether forced, shorting structurally or purposefully, fearful of dilution, having lost the conviction of their principles or belief in their investment theses, etc., are selling. Buyers need more information and clarity, and are not buying enough to offset the selling.

Barring news, it is not unreasonable to expect further pressure on the stock this week and into the middle of next week. More people will get unnerved and more people will sell. You could and probably will be tested further.

PVCTP is not exactly helping: The uncertainty surrounding the PVCTP "IPO" remains. I have heard no specifics regarding pricing, save the speculation masked as certainty from Maxim. If the preferred offering is utilized, having Pfizer and Johnson & Johnson co-leads would mean company friendly terms.

The SPA?: The lack of an SPA PR announcing its receipt has disappointed some.

It is not difficult to see why an agreed upon SPA would be desirable to have...An SPA can be appealing to the industry since it is sometimes difficult to get timely feedback from the agency. Once FDA has indicated it accepts the protocol, a company will assume it has a written contract with the reviewing division assuring acceptance of the proposed efficacy claim if the data fit the prospectively defined success criteria. This is perceived to reduce risk by eliminating the fear that a positive outcome in Phase III might not result in approval if the trial design is not acceptable to FDA. Obviously that kind of risk minimization is alluring to analysts and board members. (Source)

Management is committed to the process. As I wrote yesterday, I am led to believe there is no more negotiating or discussion with the FDA on the trial design. But, the SPA will arrive when it arrives.

It is also important to be realistic about the SPA time frame...[T]he SPA process has, at times, become a protracted early battleground for future efficacy claims. Very often the disagreements are centered on the primary outcome variable and intended statistical analysis. Of course those are intimately related to future label claims and size of the study, possibly the most vital elements in a development program. (same source as above)

Balance sheet?: And concerns remain about the company having sufficient money to begin conducting, let alone completing, pivotal, key and other trial work.

There is no doubt the stock is broken, but the company is not. Broken stocks see their share prices fall despite sound fundamentals; in Provectus' case, very attractive clinical, regulatory and business value propositions (and some aspects of the stock value proposition as well). Broken companies are flawed in one or more fundamental ways, and their share prices are very validly beaten up for them.

Nothing has changed from my depiction of the horserace on Sunday. Timing is an issue, but when is it not. These things will play themselves out. My investment thesis remains. I am not here to hold your hand, but to ask you:

Has PV-10's clinical value proposition and, thus, your investment thesis changed for the worse?

Provectus issued a PR yesterday describing final MM Phase 2 data, providing a copy of the ESMO 2012 poster and describing design parameters of the pivotal MM Phase 3 trial for which the company is seeking an SPA from the FDA.

Phase 2 data. The final MM data was first presented by Dr. Agarwala in Munich on June 22 at At 2nd European Post-Chicago Melanoma Meeting 2012. See the PR here. There some slight differences from the data presented in Vienna on October 1 that may be gleaned from comparing the two PRs. These appear negligible or immaterial:

An Objective Response Rate of 51% (v. 50% in Munich) in subjects' target lesions (25% Complete Response and 26% Partial Response [v. 25%]);

69% disease control (v. 70%) in these lesions (combined Complete, Partial and Stable Response subjects); and

Stage III subjects experienced a substantially higher target lesion response rate (60% OR [v. 58%] and 79% [v. 81%] disease control) versus Stage IV subjects (22% and 33%, respectively);

Analysis of temporal data showed that Stage III subjects also experienced significantly greater mean Progression Free Survival (PFS) of at least 9.7 [v. 9.6] months, versus 3.1 months for Stage IV subjects (median PFS for Stage III subjects was not reached during the 12-month study interval).

What appeared new (in contrast to the Munich presentation was overall survival.

Overall, the Phase 2 data was very strong, particularly for Stage III subjects, who will be the patient population for the Phase 3 trial. It was striking to net out those subjects experiencing early progression prior to the week 8 assessment who were then classified as non‐evaluable (NEV): 66% OR -- two-thirds of subjects -- and 88% disease control -- nearly 9 in 10 subjects, assuming my process and math is correct. The PFS curve is very similar when netting out NEV, although it does improve.

What is even more striking is the expectation the Phase 3 trial will improve further -- Phase 2 bested Phase 1, and now Phase 3 is expected to best Phase 2 -- since Phase 3 investigators will be able to treat all lesions.

The finalization of this data bodes well for its long-awaited publication in The Lancet in 2012.

ESMO poster. The poster itself had a few other useful nuggets. First, the Australian combination therapy study of intralesional PV-10 plus radiotherapy by Foote et al. had enrolled 7 patients as of July. The recent rumor of a double digit number of patients enrolled in the trial makes sense.

Second, the start of the human MOA study by Moffitt was imminent as of the submission of the poster.

Phase 3 trial design. I had thought Dr. Agarwala's Munich presentation had contained the final design. I was incorrect. I am led to believe there is no more negotiating or discussion with the FDA on the trial design, which makes sense. The Vienna PR goes into great detail about the design parameters, as contrasted with the Munich PR, which did not mention any meaningful aspect of the trial design.

The second quote attributed to Eric in the trial design section of the PR is telling. In particular: "This study is designed to demonstrate delay or avoidance of progression of melanoma from a locoregional disease to a life-threatening systemic stage." PV-10 treats disease so well, there will be much less Stage IV disease. Melanoma will not spread to visceral organs because the drug would have stopped it before it does.

There would appear to be no doubt the Phase 3 trial will hit is primary endpoint of PFS. If Provectus hits the same PFS in Phase 3 as the company did in Phase 2, the endpoint is reached. The contemplated hazard ratio dictates almost 6 months PFS for PV-10 versus just less than 3 months for DTIC/TMZ.

The 4-week clinical response assessment (in addition to the 12-week full response assessment) is interesting new design parameter. It is an excellent way for Provectus to measure how effective PV-10 is versus DTIC/TMZ as the study progresses (i.e., a very clear picture of trial success as early as 1Q13 or 2Q13).