ex·cit·ed. Coming out of SSO, there is a palpable sense of excitement in management.

clar·i·ty. Following a call with management earlier today, I think I have never been more clear in my projection for or estimation of the company's trajectory.

CEO letter. I think the letter will come out next week.

Much more later (shortly).

March 30, 2012

March Monthly Trading Volume

The trading (market) quarter closed today. Monthly trading volume for March was 3.43MM, up from 2.07MM for February (+66%). March's figure was the highest in 4 (December, 3.45MM) to 8 months (5.59MM).

Quarterly volume for Q1 2012 was 8.76MM, up from 8.36MM for Q4 2011 (+5%), but with quite a way to go before matching quarters before that.

Quarterly volume for Q1 2012 was 8.76MM, up from 8.36MM for Q4 2011 (+5%), but with quite a way to go before matching quarters before that.

March 28, 2012

Xanthene Dyes Induce Membrane Permeabilization of Bacteria and Erythrocytes by Photoinactivation

Kato, H., Komagoe, K., Nakanishi, Y., Inoue, T. and Katsu, T. (2012), Xanthene Dyes Induce Membrane Permeabilization of Bacteria and Erythrocytes by Photoinactivation. Photochemistry and Photobiology, 88: 423–431.

Abstract

We analyzed the photoinactivation of the membrane functions of bacteria and erythrocytes induced by xanthene dyes. The dyes tested were rose bengal, phloxine B, erythrosine B and eosin B. These dyes induced the leakage of K+ from Staphylococcus aureus cells within minutes of photoirradiation, in the order of rose bengal > phloxine B > erythrosine B > eosin B. The ability of dyes to inhibit respiration was weak, except for rose bengal, and the dyes dissipated the membrane potential in similar time traces with changes in K+ permeability. The xanthene dyes also induced the leakage of K+ from bovine erythrocytes upon photoirradiation in the same order as that observed with bacteria. Furthermore, we found that the ability to cause the leakage of K+ from erythrocytes was associated with dye-induced morphological changes, forming a crenated form from the normal discoid. These results are discussed in connection with the ability of xanthene dyes to generate singlet oxygen and bind to bacterial cells, and further compared with the actions of cationic porphyrins, which induced photoinactivation of bacteria through respiratory inhibition.

Quick hit: As you may know, Craig previously presented work showing rose bengal as a potent killer of Staphylococcus aureus.

[0099]

March 27, 2012

Revelation Special Situations Fund (update)

I previously posted about Revelation (formerly Osmium) Special Situations Fund and the fund's beneficial ownership in the company here. As the only visible name in the stock, it's worthwhile to expend a few brain cells thinking about Revelation from time to time.

Like now. A blog reader made the following comment: "Revelation appears to be in some trouble. 4 key staff quit recently and the fund is seeing redemptions. Caveat Emptor!"

Have staff quit? Yes. Several members of the firm (3 from the market-neutral, event-drive Revelation Special Situations Fund and the head of marketing/IR) left before it was widely reported in December (4 months since publication, 5 months since actual departure).

Seeing redemptions? Likely late last year (i.e., Q4).

I don't find 13Fs to be completely precise, so these figures may not represent the firm and fund's true AUM nor all of its holdings. Also, I don't think Revelation has been sufficiently precise in their filings to include their holdings of Provectus preferred shares and warrants.

AUM goes up and down based on subscriptions, redemptions and market fluctuations. Depending on how the Special Situations operating or investment agreement is written, and depending on notice for redemptions and investor gates (if any), redemptions are more likely to have occurred in the fourth calendar quarter, with the September 30 drop due mainly to the market decline.

In trouble? Hard to tell. Chris Kuchanny founded Revelation (as Osmium), and was a former ABN Amro prop trader. So, the fund has someone who can set the strategy and tactics of the book. There are lots of explanations for staff departures. My favorite is that with the fund underwater and likely having to go some distance before getting above the high water mark before performance fees are charged again, the departing individuals (more so the traders, but also the marketing/IR person) likely did not want to stick around and work for salary (management fees).

Provectus? Revelation's Special Situations Fund holds Provectus' preferred shares and warrants. Its holdings were beneficial and unchanged as of their most recent 13G filing. So, it does not look like 2011 fund redemptions or staff departures was created an impact on their Provectus holdings. The company's most recent 10K filing noted 3.5MM preferred shares remain [unconverted into common stock].

I don't think Revelation has sold any of their position.

Caveat emptor? Always!

Like now. A blog reader made the following comment: "Revelation appears to be in some trouble. 4 key staff quit recently and the fund is seeing redemptions. Caveat Emptor!"

Have staff quit? Yes. Several members of the firm (3 from the market-neutral, event-drive Revelation Special Situations Fund and the head of marketing/IR) left before it was widely reported in December (4 months since publication, 5 months since actual departure).

Seeing redemptions? Likely late last year (i.e., Q4).

- At March 31, Revelation's firm AUM appears to be about $488MM,

- At June 30, Revelation's firm AUM appears to be about $564MM,

- At September 30, Revelation's firm AUM appears to be about $362MM, and

- As at December 31, Revelation's firm AUM appears to be about $297MM.

I don't find 13Fs to be completely precise, so these figures may not represent the firm and fund's true AUM nor all of its holdings. Also, I don't think Revelation has been sufficiently precise in their filings to include their holdings of Provectus preferred shares and warrants.

AUM goes up and down based on subscriptions, redemptions and market fluctuations. Depending on how the Special Situations operating or investment agreement is written, and depending on notice for redemptions and investor gates (if any), redemptions are more likely to have occurred in the fourth calendar quarter, with the September 30 drop due mainly to the market decline.

In trouble? Hard to tell. Chris Kuchanny founded Revelation (as Osmium), and was a former ABN Amro prop trader. So, the fund has someone who can set the strategy and tactics of the book. There are lots of explanations for staff departures. My favorite is that with the fund underwater and likely having to go some distance before getting above the high water mark before performance fees are charged again, the departing individuals (more so the traders, but also the marketing/IR person) likely did not want to stick around and work for salary (management fees).

Provectus? Revelation's Special Situations Fund holds Provectus' preferred shares and warrants. Its holdings were beneficial and unchanged as of their most recent 13G filing. So, it does not look like 2011 fund redemptions or staff departures was created an impact on their Provectus holdings. The company's most recent 10K filing noted 3.5MM preferred shares remain [unconverted into common stock].

I don't think Revelation has sold any of their position.

Caveat emptor? Always!

March 26, 2012

Quick Hits for March 26

Impressive poster results. Although I'd like to use "incredible," I'll stick with "impressive" as the lead-in to this quick hit. With the poster out, takeaways include:

- Severe. I don't think we fully appreciate the severity or harshness of Moffitt's lung metastases model, which makes the result of 0, 1 and 3 tumors in 3 of 5 mice treated with PV-10 versus >250 tumors in each of the control mice indeed incredible.

- Repeated. Independently reproduced results of what already has been demonstrated by the company is important as well: systemic response, t-cell involvement, remote effect, tumor-specific immune response, interferon response, etc.

PV-10 has a specific immune response. "...[A]n immune-mediated anti-tumor response to PV-10 treatment was observed, including induction of tumor-specific interferon-gamma production by splenocytes derived after PV-10 treatment compared to control." (company comments, March 26 PR)

...[I]ntratumoral PV-10 causes both a direct anti-tumoral response of the injected tumor and a systemic tumor-specific activation of the immune system. (Toomey, March 26 PR) This is third party validation and, more importantly, I think essentially reproduces management's work in the area. Repetition is good.

May 16, 2012 now becomes an important date. I think more information on Moffitt's continuing immunology-related work on PV-10 and those results should be revealed and displayed at ASCO 2012, as speculated by Maxim's equity research analyst. The SSO abstract was submitted in the October-November time frame. The ASCO abstract submission deadline was in February.

SSO takeaways are, in some ways, comparable to the takeaways from the ASCO 2010 presentation on visceral metastases. The PIs at ASCO highlighted the correlation between visceral response with response of injected lesions similar to that observed with cutaneous bystander lesions. Using preliminary efficacy data from the first MM Phase 2 cohort of 40 patients, bystander lesion OR for subjects with a positive OR of target lesions was 62%, while the bystander lesion OR for subjects with a negative OR of target lesions was 12% (a statistically significant result).

More answers now create more questions. They include:

- Success with other types of cancers. What else has Moffitt achieved and accomplished? The SSO-presented work or study focused on melanoma and lung metastases. Has Moffitt conducted work on other types of cancers?

- Ongoing accelerated approval dialogue with DOP2. Based on statistically and clinically superior PFS results in the MM Phase 1 and 2 trials and, now, buttressed by Moffitt's statistically- and clinically-demonstrated immunology outcome (that builds upon, validates and reproduces the company's prior immunology-related work), is accelerated approval at some reasonable point in the near-future more likely?

- Human studies to come. When will the human MOA study commence?

- How now Pfizer? I think I am not the only one impressed by Moffitt's publicly announced results to date and inferences of their likely future outcomes.

It's clear there are more layers of the onion to peel. As they say, more to come from Moffitt.

Intralesional PV-10 Treatment Leads to the Induction of Anti-Tumor Immunity

Following its Friday PR -- Mechanism of Action Data On PV-10 Demonstrates Therapy Induces Immunologic Response: (i) Leads to Regression of Untreated Lung and Cutaneous Melanoma Metastases and (ii) Results Detailed in Poster Presentation at the Society of Surgical Oncology Annual Meeting; Details of Poster Expected to Be Released Next Week -- Provectus released the second immunology-/SSO-related PR today.

The poster is below:

I below up some of the portions of the poster.

The poster is below:

I below up some of the portions of the poster.

March 25, 2012

Looking Forward on March 25

Details. What immunology-related details will be provided next week by the company? It will be interesting to see if Moffitt's poster identifies (and discusses) the specific immune response.

Game changer. Some of you may recall that Rodman & Renshaw's Elemer Piros said, paraphrasing, around the time of ASCO 2010, that elucidating the remote bystander effect in visceral metastases could be a "game changer" for the company. At the time, in presenting some of the MM Phase 2 trial results, the principal investigators noted a correlation between the visceral response and the response of injected lesions similar to that observed with cutaneous bystander lesions, and a pattern consistent with a common immunologic mechanism. Fast forward 20 months, Moffitt's published abstract, to use Craig's word from Friday's PR, independently validates a systemic effect for PV-10. Does Piros still consider this a game changer? It will be interesting to see if Piros issues a substantive equity research update on this topic next week.

Comments. I was struck by Craig's quoted (i.e., prepared) comments in Friday's PR: "The data from this independent study validates our belief that PV-10 induces systemic effects similar to those observed with immunotherapy or a vaccine. However, in contrast to conventional immunotherapies or vaccines, PV-10 also leads to a readily apparent and well-documented, rapid destruction of the treated lesions, which appears to afford a unique combination of reduced tumor burden and in situ immune stimulation against remaining tumor tissue." There have been several recent journal and news articles on immunotherapies and vaccines, such as this one and this one. So, his efforts to distinguish PV-10 from conventional immunotherapies and vaccines (as a chemoablative immunotherapeutic) are notable. It will be interesting to see the theme(s) of his Maxim Group conference presentation on Monday.

News cycle. Speaking of news articles, how much, if any, press and awareness can management gin up from SSO? It will be interesting to see if the news cycle can bring immunology-related coverage about PV-10.

Game changer. Some of you may recall that Rodman & Renshaw's Elemer Piros said, paraphrasing, around the time of ASCO 2010, that elucidating the remote bystander effect in visceral metastases could be a "game changer" for the company. At the time, in presenting some of the MM Phase 2 trial results, the principal investigators noted a correlation between the visceral response and the response of injected lesions similar to that observed with cutaneous bystander lesions, and a pattern consistent with a common immunologic mechanism. Fast forward 20 months, Moffitt's published abstract, to use Craig's word from Friday's PR, independently validates a systemic effect for PV-10. Does Piros still consider this a game changer? It will be interesting to see if Piros issues a substantive equity research update on this topic next week.

Comments. I was struck by Craig's quoted (i.e., prepared) comments in Friday's PR: "The data from this independent study validates our belief that PV-10 induces systemic effects similar to those observed with immunotherapy or a vaccine. However, in contrast to conventional immunotherapies or vaccines, PV-10 also leads to a readily apparent and well-documented, rapid destruction of the treated lesions, which appears to afford a unique combination of reduced tumor burden and in situ immune stimulation against remaining tumor tissue." There have been several recent journal and news articles on immunotherapies and vaccines, such as this one and this one. So, his efforts to distinguish PV-10 from conventional immunotherapies and vaccines (as a chemoablative immunotherapeutic) are notable. It will be interesting to see the theme(s) of his Maxim Group conference presentation on Monday.

News cycle. Speaking of news articles, how much, if any, press and awareness can management gin up from SSO? It will be interesting to see if the news cycle can bring immunology-related coverage about PV-10.

Legend

"Myrmidons, my brothers of the sword. I'd rather fight beside you than any army of thousands. Let no man forget how menacing we are, we are lions! Do you know what's there, waiting, beyond that beach? Immortality! Take it, it's yours!"

Who are you? Do you want to be legendary? Or do you want to do something legendary?

March 22, 2012

Quick Hits for Thursday, March 22

Moffitt folks should speak tonight, tomorrow and the day after. The poster sessions for Toomey et al. at which they will speak and/or be available are:

The Moffitt poster will be very important to see and read. I think a copy of the poster will be available as part of one of the company's SSO-related PRs.

Both Rodman & Renshaw and Maxim Group issued psoriasis Phase 2c trial result update notes. R&R provided its note yesterday. Maxim's update came out today. Both are available via Provectus News. Both firms maintained their respective price targets of $3.00 and $3.50 per share (March 21 closing price: $0.89).

R&R's key points: The trial compared safety and efficacy of three dose levels of PH-10. The lower dose (0.002%) of PH-10 achieved the best activity among the three doses tested.

Maxim's key points: Positive PH-10 top-line Phase 2 results in Psoriasis. PV-10 is still the key catalyst.

Provectus has a new lead research analyst covering them at Maxim Group. The Maxim analyst that covered the company, Dr. Yale Jen, has moved on to ROTH Capital Partners. The current Maxim analyst is Dr. Echo Yinghui He.

PH-10 and PV-10 have a robust safety profile don't ya know! Spectacular efficacy should follow. The 2c trial results were very comparable to the 2b trial results for both efficacy and safety. Safety continues to be the mantra (Craig has previously made positive comments regarding the toxicity studies the company is running on PH-10). Think efficacy per unit safety (as much as an investment person thinks about return per unit risk): dermatology risk-reward. The value proposition relies on a combination of both parameters. I think we will see much higher efficacy with no material change in safety (i.e., adverse events) in the pivotal Phase 3 trial.

Of course, my opinion of the 2c trial results does not matter. The only opinions that matter are those of the prospective derm and derm-pharma companies thinking about licensing PH-10. Furthermore, what matters just as much is whether and how well management has made the case I outlined above, among other things, regarding efficacy and safety. Is it enough?

The spin-off process continues. With their Form D filing for Pure-ific Corporation, the company moves a step-closer to spinning off this non-core entity. I think much more information when the S-1 is filed. I have a tentative expectation for the filing as the end of the quarter.

The Moffitt poster will be very important to see and read. I think a copy of the poster will be available as part of one of the company's SSO-related PRs.

Both Rodman & Renshaw and Maxim Group issued psoriasis Phase 2c trial result update notes. R&R provided its note yesterday. Maxim's update came out today. Both are available via Provectus News. Both firms maintained their respective price targets of $3.00 and $3.50 per share (March 21 closing price: $0.89).

R&R's key points: The trial compared safety and efficacy of three dose levels of PH-10. The lower dose (0.002%) of PH-10 achieved the best activity among the three doses tested.

Maxim's key points: Positive PH-10 top-line Phase 2 results in Psoriasis. PV-10 is still the key catalyst.

Provectus has a new lead research analyst covering them at Maxim Group. The Maxim analyst that covered the company, Dr. Yale Jen, has moved on to ROTH Capital Partners. The current Maxim analyst is Dr. Echo Yinghui He.

PH-10 and PV-10 have a robust safety profile don't ya know! Spectacular efficacy should follow. The 2c trial results were very comparable to the 2b trial results for both efficacy and safety. Safety continues to be the mantra (Craig has previously made positive comments regarding the toxicity studies the company is running on PH-10). Think efficacy per unit safety (as much as an investment person thinks about return per unit risk): dermatology risk-reward. The value proposition relies on a combination of both parameters. I think we will see much higher efficacy with no material change in safety (i.e., adverse events) in the pivotal Phase 3 trial.

Of course, my opinion of the 2c trial results does not matter. The only opinions that matter are those of the prospective derm and derm-pharma companies thinking about licensing PH-10. Furthermore, what matters just as much is whether and how well management has made the case I outlined above, among other things, regarding efficacy and safety. Is it enough?

The spin-off process continues. With their Form D filing for Pure-ific Corporation, the company moves a step-closer to spinning off this non-core entity. I think much more information when the S-1 is filed. I have a tentative expectation for the filing as the end of the quarter.

March 21, 2012

Some Thoughts Regarding the Dermatology Deal (Licensure) Process (Journey)

Commentary to follow in a subsequent blog post.

Click on the table below to see a much larger version on your screen.

March 20, 2012

Quick Hits for Tuesday, March 20

Patrick Cox provided an update on Provectus today to his newsletter subscribers. I found his framing of this point to be quite striking: "As you know, Rose Bengal was initially used as a wool dye, but attracted the attention of scientists because of the molecule's ability to bind with unhealthy cells, but not healthy cells. It inspired legendary scientist Paul Ehrlich (1854-1915) to formulate the "magic bullet" theory that drugs could be found that target only diseased cells. It is ironic, in fact, that he never realized the dye that led to the theory was itself a powerful magic bullet capable of attacking a variety of diseased cells without harming those that are healthy."

More information on the immunology work done by Toomey et al. should be available on Thursday. Results, findings and data from poster presentations are embargoed until the beginning of the scientific session in which the research is presented. I think this means Moffitt's work (I hope, beyond what we already know from the abstract) should be available at or around 4 pm EST on Thursday, March 22.

As a result, expect a immunology-related PR from the company, likely on Friday morning, discussing Moffitt's abstract. Thus far, despite the abstract being publicly accessible (see here), management has not yet commented on it. Based on their historical behavior and approach, I assume they are following the communications protocol set forth by the SSO Annual Cancer Symposium.

A second immunology-related PR should follow from Provectus, possibly on Friday morning but more likely on Monday morning, discussing Moffitt's additional work. More work has been done by Toomey et al. since the abstract was submitted in October.

Expect a CEO newsletter from Craig next week. As a reminder, he will present at the 2012 Maxim Group Growth Conference on Monday, March 26 at 4 pm EST. If the second immunology-related PR is issued Friday or Monday morning, I think a central theme of Craig's Maxim presentation will be PV-10's systemic benefit and/or his perspectives on several facets of PV-10's mechanism of immune response Moffitt has validated (based on, of course, his historical research and work).

More information on the immunology work done by Toomey et al. should be available on Thursday. Results, findings and data from poster presentations are embargoed until the beginning of the scientific session in which the research is presented. I think this means Moffitt's work (I hope, beyond what we already know from the abstract) should be available at or around 4 pm EST on Thursday, March 22.

As a result, expect a immunology-related PR from the company, likely on Friday morning, discussing Moffitt's abstract. Thus far, despite the abstract being publicly accessible (see here), management has not yet commented on it. Based on their historical behavior and approach, I assume they are following the communications protocol set forth by the SSO Annual Cancer Symposium.

A second immunology-related PR should follow from Provectus, possibly on Friday morning but more likely on Monday morning, discussing Moffitt's additional work. More work has been done by Toomey et al. since the abstract was submitted in October.

Expect a CEO newsletter from Craig next week. As a reminder, he will present at the 2012 Maxim Group Growth Conference on Monday, March 26 at 4 pm EST. If the second immunology-related PR is issued Friday or Monday morning, I think a central theme of Craig's Maxim presentation will be PV-10's systemic benefit and/or his perspectives on several facets of PV-10's mechanism of immune response Moffitt has validated (based on, of course, his historical research and work).

March 19, 2012

Provectus Announces Top Line Phase 2 Data For PH-10 in Its First Randomized Controlled Psoriasis Study

The company provided top-line data results for its psoriasis Phase 2c trial in a PR today. There is a significant amount of knowledge and information behind the top-line results within the full dataset (by definition), as there were for the atopic dermatitis Phase 2 and psoriasis Phase 2b trials.

Data analysis. Below is a simple comparison of available top-line results from the 2b and 2c trials.

Takeaways.

- Reproducibility achieved: I think the Phase 2b (0.001%) and 2c (0.002%) trials yielded comparable data of consistent disease metric improvement.

- No vehicle effect seen: The vehicle was inferior to all 2c arms and in comparison to the 2b trial. I think there was no clear trend for the vehicle in the 2c trial.

- Continued robust safety: I think there were no significant safety issues or adverse events identified in any of PH-10 dose groups of the 2c trial, which compares favorably to the safety outcome of the 2b trial.

- Continue good efficacy (again restrained by the trial design, by design). The 2c trial (and, by extension the 2b trial) demonstrated all of the active arms were effective and superior to the vehicle. I also think patients did not relapse (i.e., there was no substantial rebound after administration of PH-10 was stopped). It is obvious the 28-day period limited efficacy, so neither the 2b or 2c trials provided optimal or "more optimal" conditions under which to achieve [much] better efficacy. For example, I think the consistent trends across both Phase 2 studies indicate suggest continued improvement is likely with extended treatment of, say, up to 12 weeks.

Observations.

- Good knowledge with which to design a pivotal phase 3 trial design. The 2c trial design was a standard design for the FDA to approve a dermatology product. A pivotal phase 3 trial design simply would be a larger version of the vehicle-controlled 2c trial; however, management now knows, among other things, (a) how to optimize around the .001% and 0.002% dosing (versus higher concentrations, which probably acted like sunscreen and limited the activation of the active ingredient) and (b) how optimize the application period.

Keep in mind. A true assessment of the value of PH-10 is multi-dimensional: safety (risk), efficacy (reward) and price (to the patient to buy)-cost (to the company/licensee to produce).

March 17, 2012

March Madness

I will be paying close attention to what comes out of this conference (March 21-24). Immunology has become a key valuation driver, together with PV-10's robust efficacy and long-standing safety.

Never the twain shall meet. Or shall they?

"Oh, East is East, and West is West, and never the twain shall meet."

A big pharma executive says to you something like: "PV-10? There's nothing on the market quite like it." Buyers and sellers coming together to agree on price makes a market. If you were management, for how much would you sell the company? $1 billion? $3 billion? $5 billion? More?

A big pharma executive says to you something like: "PV-10? There's nothing on the market quite like it." Buyers and sellers coming together to agree on price makes a market. If you were management, for how much would you sell the company? $1 billion? $3 billion? $5 billion? More?

March 16, 2012

Compensation (10K for FY/CY 2011 [update])

My original 10K for FY/CY 2011 post included comments regarding my estimate (educated guess) of FY/CY 2011 management compensation. It is difficult, or not easy, to put an exact number on total payroll (e.g., salary, cash bonuses, stock option awards, other compensation such as paid-out vacation, etc.) as I think payroll is divided up between R&D and G&A based on some estimate of who of management spends what amount of time where.

We'll have to wait until April -- likely late-April, but possibly as late as early-May -- for the company's proxy filing/Schedule 14A for specific compensation information. I think 2011 compensation was comparable to 2010, but the 10-K only specifically indicates that stock option expenses decreased year-over-year:

I still don't.

I understand the consternation some shareholders have with management's compensation, particularly when juxtaposed against the current and historical share price.

I don't disagree with these shareholders.

It's difficult for most people, whether so-called professional investors or retail ones, to view management compensation through the prism of time. Most people look at most things (investing or otherwise) at a snapshot in time, rather than in the much larger context of their investment thesis' monetization component. Management certainly is not helped by the stagnating and decreasing share price over the last 5 or so years. Connecting these dots -- higher than average compensation, a low share price for some time -- it's not unreasonable to wonder and complain about compensation.

If I could point to material bad behavior or questionable actions, compensation might then raise a red flag. But I can't, so it doesn't.

My prism of time can only be judged with the benefit of hindsight in the future, not now. If management does what I think they will do in terms of the magnitude of the monetization (i.e., the sale of the company to Pfizer or J&J or some other big pharma, the enterprise value of which would include the sale/license of the dermatology business), their compensation will have been well worth it.

If the outcome, if any, is far from optimal, then I will share the consternation of those disgruntled shareholders. But until then, if then ever comes, I don't care about that viewpoint.

We'll have to wait until April -- likely late-April, but possibly as late as early-May -- for the company's proxy filing/Schedule 14A for specific compensation information. I think 2011 compensation was comparable to 2010, but the 10-K only specifically indicates that stock option expenses decreased year-over-year:

- Page 31: Research and development costs...for 2011 included payroll of $6,182,147... Research and development costs...for 2010 included payroll of $6,618,532... The decrease in payroll in 2011 over 2010 is primarily due to decreased stock option expense and decreased pension expense.

- Page 32: The increase is primarily due to increased investor relations expense of approximately $850,000 due to the expanded programs to improve investor awareness and visibility of the Company’s clinical progress as well as related travel expenses, offset by decreased pension and stock option expenses of approximately $500,000.

I still don't.

I understand the consternation some shareholders have with management's compensation, particularly when juxtaposed against the current and historical share price.

I don't disagree with these shareholders.

It's difficult for most people, whether so-called professional investors or retail ones, to view management compensation through the prism of time. Most people look at most things (investing or otherwise) at a snapshot in time, rather than in the much larger context of their investment thesis' monetization component. Management certainly is not helped by the stagnating and decreasing share price over the last 5 or so years. Connecting these dots -- higher than average compensation, a low share price for some time -- it's not unreasonable to wonder and complain about compensation.

If I could point to material bad behavior or questionable actions, compensation might then raise a red flag. But I can't, so it doesn't.

My prism of time can only be judged with the benefit of hindsight in the future, not now. If management does what I think they will do in terms of the magnitude of the monetization (i.e., the sale of the company to Pfizer or J&J or some other big pharma, the enterprise value of which would include the sale/license of the dermatology business), their compensation will have been well worth it.

If the outcome, if any, is far from optimal, then I will share the consternation of those disgruntled shareholders. But until then, if then ever comes, I don't care about that viewpoint.

March 15, 2012

Let's Make A Dermatology Deal

A blog reader inquired about why I did not talk about dermatology as a value driver (as I did about PV-10's clinical and business value propositions). The reader asked if I was feeling less optimistic about a deal that could give the share price a much needed boost. A much needed boost? Ain't that the truth!

While I focused on PV-10 and oncology in exploring and crafting the various value propositions, PH-10 and dermatology represent a potentially very valuable asset, the sale of which could serve as a catalyst for a meaningful and sustained increase in the share price and, ultimately, the acquisition of the whole company.

PH-10 and dermatology share common clinical and business value propositions with PV-10 and oncology: efficacy, safety, administration, treatment pricing, cost of manufacturing, cost of scaling manufacturing, IP protection, etc.

The current expectation is a headline deal size of $500 million for dermatology (to include all indications, clinically, pre-clinically or bench tested, such as atopic dermatitis, psoriasis, acne, etc.). The structure of the deal likely would be very traditional:

- An upfront payment,

- One or more clinical milestone payments (e.g., completed pivotal phase 3 trials),

- One or more regulatory milestone payments (e.g., FDA approval for indications), and

- Royalty payments (e.g., a percentage of sales).

$500 million represents a present value assessment of the deal itself, including upfront payments and future milestone and royalty payments, and is based on several assumptions that of course could change and raise or lower this headline expectation:

- An upfront payment, however structured (e.g., cash and/or stock), might range from $10-$50 million. The range is influenced by direct and indirect factors. A higher upfront payment might accrue because of the increasing value of and potential in PH-10 and/or management's desire to take more money upfront rather than in contingent payments. I do not know management's expectations in this regard, but I would hazard a guess that above a certain cash level, like $10-20 million, they would rather get more cash in the future because of their belief in the efficacy and safety of PH-10 (i.e., more royalties from more sales);

- Clinical and regulatory milestone payments measured in tens of millions of dollars. I cannot really hazard a guess as to a range here, but these payments likely would not be insignificant; and,

- A mid- to high-single digit royalty percent over a 10- to 15-year term. This is facet of the deal is where the clinical and business value proposition of PH-10 is put to the test with the hope of the product earning initial market share and then grabbing more -- much more -- based on robust efficacy, dramatic safety and flexible (and perhaps) predatory [to competitors] pricing. Depending on how high interest is, royalty payments might be low double digits and the term might extend out to 20 years.

But, in order to begin to sniff such aspirations, we need to see and understand the psoriasis Phase 2c results (and as they compliment and further validate the AD and psoriasis Phase 2 trials).

The AD Phase 2 Trial

The AD Phase 2 trial showed improvement in all efficacy metrics. There was consistent improvement in all study metrics during 4 weeks of treatment. Such improvements persisted after cessation of treatment.

There was improvement in pruritus (itching). Pruritus (itching) was a leading indicator with dramatic improvement evident from outset.

Subjects achieved “Clear” or ”Almost Clear.” There was a consistent increase in subjects achieving “Clear”/“Almost Clear” over the study interval. There was a comparable reduction in the number of subjects with “Severe” or “Very Severe” disease.

There was a 50 or 75% improvement in the EASI score. There was an increase in subjects achieving 50% and 75% improvement in EASI scores over the study interval. EASI performance corresponded to an improvement in Global Assessment scores.

The Psoriasis Phase 2 Trial

The trial used 0.001% RB for 28 days observed over 8 weeks.. There were substantial improvement in PSI and Pruritus during 4 weeks of treatment.

There was an improvement in PSI Component Scores. The improvement in mean scores corresponded to the subjects achieving “slight” or “none” in PSI components.

Trends in individual PSI scores corresponded to overall improvement in subjects.

Most subjects reported no or only mild pruritus by Week 4.

For a plaque response assessment, most subjects were graded as clinically improved by Week 4.

The Psoriasis Phase 2c Trial...

The trial used a vehicle and 0.002%, 0.005% and 0.01% RB for 28 days observed over 8 weeks. What will be the PSI, Plaque Response Assessment and Pruritus Self Assessment values of the vehicle and the different RB concentrations, and how will they compare to the Phase 2 trial?

10K for FY/CY 2011

The 10-K is out. One point of observation, for now: The cash balance at December 31 was approximately $7.7 million. The filing carries the somewhat stock statement of "At our current cash expenditure rate, our cash and cash equivalents will be sufficient to meet our current and planned needs until 2013 without additional cash inflows from the exercise of existing warrants, stock options, or sales of equity securities. We have enough cash on hand to fund operations until late 2013 with the cash on hand at December 31, 2011."

Clearly "current and planned needs" can have a very broad or narrow meaning, such as depending on what if any pivotal Phase 3 or other trials are conducted (e.g., MM, HCC/liver, psoriasis, immunology).

I will have much more to say later on compensation. I pulled a previous post (some of you may have read it before I "un-posted" it) in order to do some additional analysis on this topic.

March 14, 2012

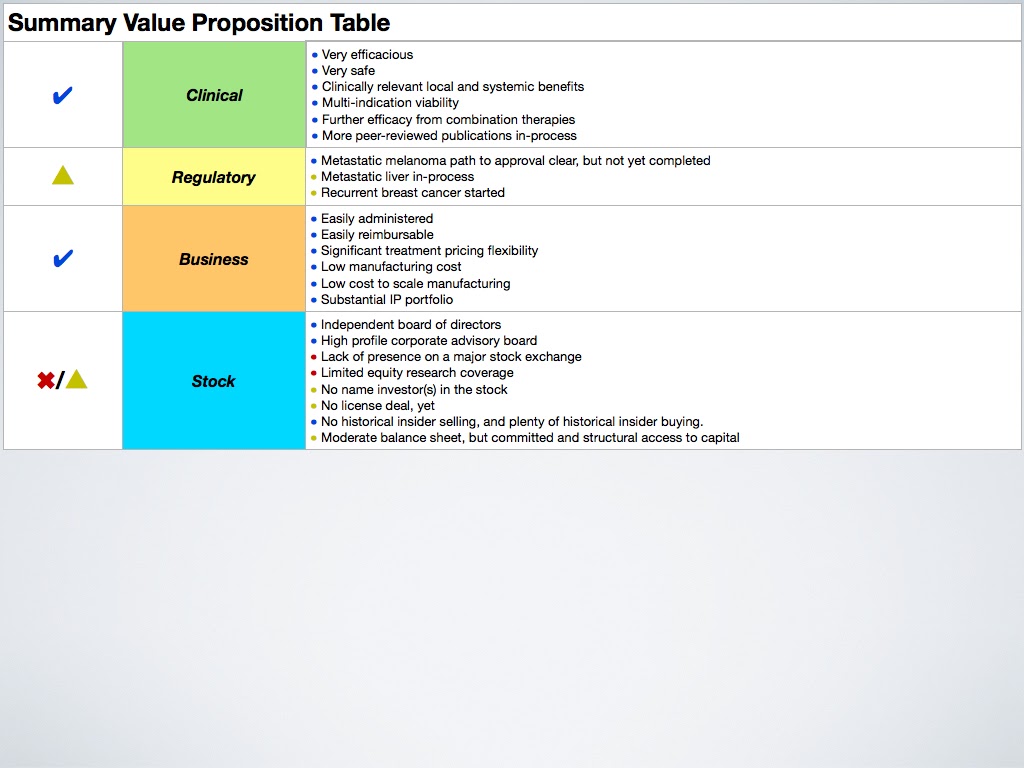

Summary Value Proposition

As you will have seen from the various value propositions I posted, PH-10 and dermatology are not addressed. With the annual meeting of the American Academy of Dermatology starting Friday in San Diego, and with the likely release of the top-line psoriasis Phase 2c trial results this week or next, the dermatology side of the business is quite relevant and germane. There are considerable clinical, regulatory and business commonalities between the dermatology and oncology applications of Rose Bengal. To focus my thinking, I only used oncology; however, dermatology certainly is an important and valuable value driver and contributor to my investment thesis.

Click on the table below to see a much larger version on your screen. Updated February 2013.

Click on the table below to see a much larger version on your screen. Updated February 2013.

March 13, 2012

Clinical Value Proposition

Click on the table below to see a much larger version on your screen. Updated February 2013.

March 12, 2012

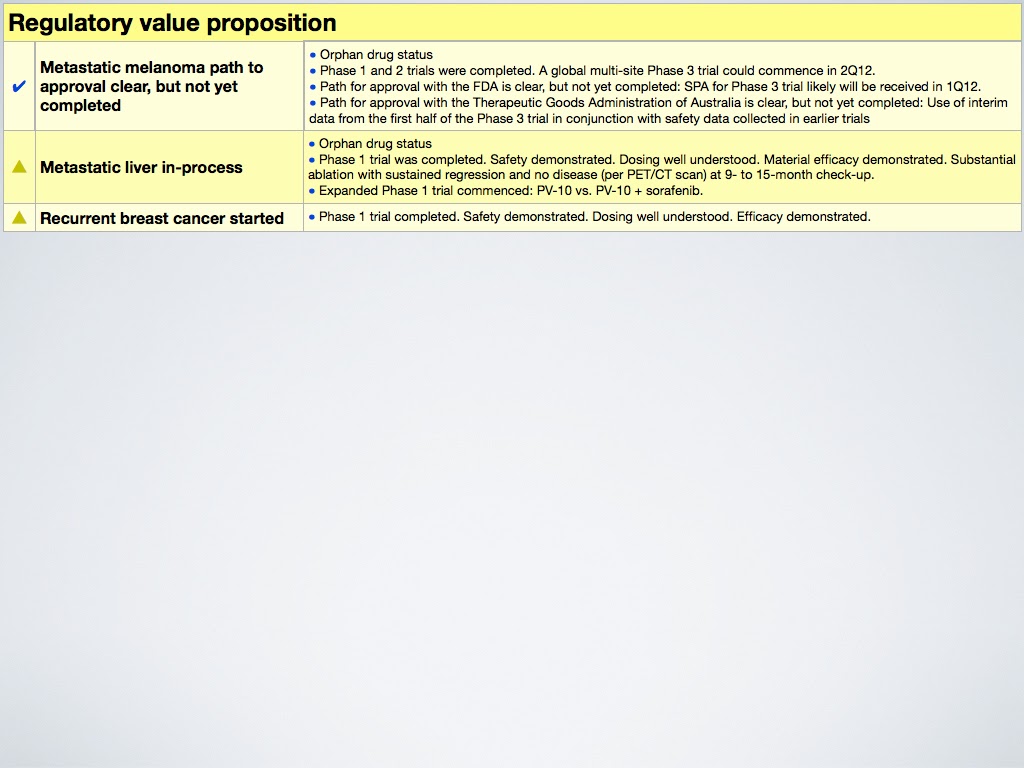

Regulatory Value Proposition

Click on the table below to see a much larger version on your screen. Updated February 2013.

March 11, 2012

Business Value Proposition

Click on the table below to see a much larger version on your screen. Updated February 2013.

Stock Value Proposition

Click on the table below to see a much larger version on your screen. Updated February 2013.

Value Propositions

I've recently been working on refining my investment thesis for Provectus by better and more crisply articulating the underlying value propositions:

- Clinical (a value driver),

- Regulatory (the process),

- Business (a value driver), and

- Stock (a lagging indicator).

I will begin posting the last two now, and the first two (together with a summary table) this week.

March 8, 2012

The Cost Of A New Drug

I want to thank a blog reader for sending me Forbes' Matthew Herper's article, The Truly Staggering Cost Of Inventing New Drugs -- The Print Version, in the March 12, 2012 issue of Forbes Magazine. This is an edited version of his February 10 post, The Truly Staggering Cost of Inventing New Drugs. Herper draws attention to the large expense to bring a drug to market (although the ultimate number depends on the assumptions one uses as to the inputs), from the $1 billion number the drug industry has been tossing around for years (from Herper's article) to the $1.3 billion number an Eli Lilly representative posted the on the company’s corporate blog to the $4 billion number Bernard Munos of the InnoThink Center for Research In Biomedical Innovation estimated (from Herper's article) to Forbes' expanded analysis based on Munos' work of $4 to $12 billion (see table below).

Taking the opposite view, an accounting in the journal BioSocieties claimed drug companies only were spending $55 million. See a Slate article on this here.

One of the attractive features, to me, about Provectus is management's efficient use of capital. In the graph below, I have compared Dendreon, Optimer and Provectus' accumulated deficit as reported on the companies' 10-K filings. Accumulated deficit, a balance sheet item, is a good way of understanding the R&D and "go to market" spend by a company. Note that Provectus has not yet filed its 10-K in 2012 (for 2011), so I used the most recent 10-Q. I also included the total number of shares outstanding (e.g., preferred and/or common shares, stock options, warrants) of each company over the measurement period; however, I plan to use that for a subsequent post.

It's hard not to pick on Dendreon for the staggering amount of money ($1.6 billion) it spent to bring Provenge to market and on whatever other drug/indications it has in the pipeline. Optimer ($215 million) has started making money, so its accumulated deficit in 2011 was reduced from 2010. Provectus' PV-10 has not yet been approved, of course, so the comparison of its accumulated deficit ($102 million) to that of the other two companies is not completely fair.

We can do a back-of-the-envelope calculation by making assumptions of what the MM Phase 3 trial would cost, non-trial operating expenses through that period (assuming Provectus remains independent), etc., and increase accumulated deficit by $30 to $40 million on the high side. Even then, the final number (i.e., <$150 million) still is lower than Optimer and an order of magnitude lower than Dendreon.

Taking the opposite view, an accounting in the journal BioSocieties claimed drug companies only were spending $55 million. See a Slate article on this here.

One of the attractive features, to me, about Provectus is management's efficient use of capital. In the graph below, I have compared Dendreon, Optimer and Provectus' accumulated deficit as reported on the companies' 10-K filings. Accumulated deficit, a balance sheet item, is a good way of understanding the R&D and "go to market" spend by a company. Note that Provectus has not yet filed its 10-K in 2012 (for 2011), so I used the most recent 10-Q. I also included the total number of shares outstanding (e.g., preferred and/or common shares, stock options, warrants) of each company over the measurement period; however, I plan to use that for a subsequent post.

It's hard not to pick on Dendreon for the staggering amount of money ($1.6 billion) it spent to bring Provenge to market and on whatever other drug/indications it has in the pipeline. Optimer ($215 million) has started making money, so its accumulated deficit in 2011 was reduced from 2010. Provectus' PV-10 has not yet been approved, of course, so the comparison of its accumulated deficit ($102 million) to that of the other two companies is not completely fair.

We can do a back-of-the-envelope calculation by making assumptions of what the MM Phase 3 trial would cost, non-trial operating expenses through that period (assuming Provectus remains independent), etc., and increase accumulated deficit by $30 to $40 million on the high side. Even then, the final number (i.e., <$150 million) still is lower than Optimer and an order of magnitude lower than Dendreon.

March 7, 2012

Blog Reader Q&A

Is Provectus still using Numoda's TruPoints platform for PH-10? Yes.

Is Numoda involved in any other capacity? No.

What is the deal structure for the spin-offs? More information should be available when the S-1 is filed. I think the deal structure has changed (from when I reviewed spin-off materials with the intent, at the time, of considering investment in one of the spin-offs), so I won't comment on this topic until I have the most recent information.

Is Numoda involved in any other capacity? No.

What is the deal structure for the spin-offs? More information should be available when the S-1 is filed. I think the deal structure has changed (from when I reviewed spin-off materials with the intent, at the time, of considering investment in one of the spin-offs), so I won't comment on this topic until I have the most recent information.

March 6, 2012

FDA Grants Approval to... Really!?! No, not really.

For those of you who haven't visited today the In The Media section of Provectus' website's home page, you'll see this:

News!?! No.

News!?! No.

Just the title of an article that does not match its content. Normally, In The Media items are e-mailed via Provectus News. The Dermatologist's piece was not.

Just the title of an article that does not match its content. Normally, In The Media items are e-mailed via Provectus News. The Dermatologist's piece was not.

March 4, 2012

Wither a Derm Deal?

Does the lack of a derm deal thus far worry me? No deals materialized after the company completed Phase 2 trials in psoriasis and atopic dermatitis (not to be confused with the psoriasis Phase 2c trial), when there was there expectation of a deal.

Deals, or deal interest, do not materialize because (a) there is (are) no prospective or potential party(ies) with whom or which to strike a deal or (b) the deal(s) is (are) not good enough for the company.

I am not worried.

I was disappointed that management could not strike a deal last year in dermatology. A deal, as expected, in terms of the valuation threshold sufficient for management to agree to a deal, would have increased the share price. It was clear to me at the time, however, that the clinical data was insufficient (i.e., benefit or lack of benefit of a vehicle arm) to get prospective partners to extend a sufficiently attractive term sheet or two. Just because no deal was struck does not mean no term sheets or less formal deal terms were extended. I think what the company saw was unattractive.

I am not worried, because management has demonstrated discipline in not accepting any deal, only a deal above a certain valuation threshold.

You'll recall I've previously blogged about management not accepting sub-optimal oncology deals. Do you want them to do a deal because every "real" biotechnology company has, among other things (e.g., a name investor, written multiple peer reviewed papers, has a management team that has brought drugs to market before, etc.), a deal with some pharma company? Or do you want management to do the right deal?

The stakes are raised for Provectus this time around. We are led to believe the psoriasis Phase 2c results, while they have limitations (see here or here), should produce a deal acceptable to management (the assumption is, of course, that the results are of interest to prospective partners). So, while my expectations have not changed, I am, however, expectant.

Deals, or deal interest, do not materialize because (a) there is (are) no prospective or potential party(ies) with whom or which to strike a deal or (b) the deal(s) is (are) not good enough for the company.

I am not worried.

I was disappointed that management could not strike a deal last year in dermatology. A deal, as expected, in terms of the valuation threshold sufficient for management to agree to a deal, would have increased the share price. It was clear to me at the time, however, that the clinical data was insufficient (i.e., benefit or lack of benefit of a vehicle arm) to get prospective partners to extend a sufficiently attractive term sheet or two. Just because no deal was struck does not mean no term sheets or less formal deal terms were extended. I think what the company saw was unattractive.

I am not worried, because management has demonstrated discipline in not accepting any deal, only a deal above a certain valuation threshold.

You'll recall I've previously blogged about management not accepting sub-optimal oncology deals. Do you want them to do a deal because every "real" biotechnology company has, among other things (e.g., a name investor, written multiple peer reviewed papers, has a management team that has brought drugs to market before, etc.), a deal with some pharma company? Or do you want management to do the right deal?

The stakes are raised for Provectus this time around. We are led to believe the psoriasis Phase 2c results, while they have limitations (see here or here), should produce a deal acceptable to management (the assumption is, of course, that the results are of interest to prospective partners). So, while my expectations have not changed, I am, however, expectant.

vo·lu·mi·nous (update)

I previously blogged on monthly trading volume here (I updated this chart after January, but I can't easily find it, nor the comments I made at the time). Note that I changed the volume axis to thousands of shares (from the prior number of shares).

I am surprised and unsurprised by the continued drying up of volume. While Network 1 Financial's return in December provided a temporary uptick in volume (it is an important market maker for the stock), management's reporting on the FDA's guidance regarding the SPA process clearly was insufficient (while I think they have the SPA, more importantly, the market does not) and, as I have previously blogged, only more news in March will begin to encourage more eyes to watch the stock.

I am surprised and unsurprised by the continued drying up of volume. While Network 1 Financial's return in December provided a temporary uptick in volume (it is an important market maker for the stock), management's reporting on the FDA's guidance regarding the SPA process clearly was insufficient (while I think they have the SPA, more importantly, the market does not) and, as I have previously blogged, only more news in March will begin to encourage more eyes to watch the stock.

Time line? (update)

I previously blogged clinical- and regulatory-oriented time lines. At the request of a reader, I also included conference and transaction-oriented items to this time line table.

March should be a busy month for PRs/news and information. I think the timing of a potential pancreas Phase 1 trial would be pushed out (I don't know how much so), as management completes preparation (e.g., undertake several studies to rule out PV-10 interactions with the sorafenib/Nexavar comparator) for a HCC (liver) Phase2/Phase 3 trial.

Click on the table below to see a much larger version on your screen.

Pushing out the pancreas trial is the only change to this version of the time line. I added (a) a "germination period" in Q2 for a potential derm transaction (i.e., the sale/license of the dermatology side of the business) and (b) the CEO letter, which could come out in late-March, after the 10-K is filed around mid-March.

March should be a busy month for PRs/news and information. I think the timing of a potential pancreas Phase 1 trial would be pushed out (I don't know how much so), as management completes preparation (e.g., undertake several studies to rule out PV-10 interactions with the sorafenib/Nexavar comparator) for a HCC (liver) Phase2/Phase 3 trial.

Click on the table below to see a much larger version on your screen.

Pushing out the pancreas trial is the only change to this version of the time line. I added (a) a "germination period" in Q2 for a potential derm transaction (i.e., the sale/license of the dermatology side of the business) and (b) the CEO letter, which could come out in late-March, after the 10-K is filed around mid-March.

Subscribe to:

Posts (Atom)