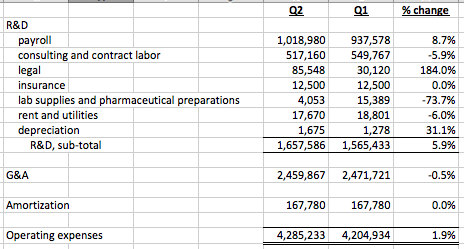

- A. Quarter-over-quarter ("QoQ") R&D expenses increased by 5.9%. QoQ G&A expenses decreased by 0.5%. Figures below are in dollars. Operating expense line items include both cash and non-cash charges.

- B. The QoQ monthly cash expenditure increased by 3.6%.

Should some of the monies raised in the quarter be used to capitalize the spin-off entities, the financing activities figure below would be lower (as spin-off capitalization funds would be segregated on their respective balance sheets), reducing Q2 quarterly and monthly burn figures (where "burn" refers to the burning of cash for strictly operating expenses of the parent corporation).

- C. The fundraising during the quarter, presumably related to the spin-offs, was completed at, roughly, a pre-money valuation of about $76MM. Shares were sold at $1.12 per share (not including warrant coverage). My original post on this topic is here. Click on the figure to enlarge it.

- D. I did some basic modeling on monthly cash burn (cash on hand, in dollars, is the Y-axis), understanding that management has significant discretion over cash expenses and the actual fixed [cost] burn is very low. Click on the figure to enlarge it.

Management notes in the filing's MD&A section: "By managing variable cash expenses due to minimal fixed costs, we believe our cash and cash equivalents on hand at June 30, 2012 will be sufficient to meet our current and planned operating needs until well into 2013 without consideration being given to additional cash inflows..."

I'd hazard a rough guess that "well into" means Q2.

- E. The company notes, for the first time in a quarterly or annual filing: "...geographic licensure of PV-10 on the basis of...[both]...Phase 2 metastatic melanoma and Phase 1 liver results in certain areas of the world."

Such ongoing discussions could refer to, at a minimum, MM in Australasia and HCC (liver cancer) in China. Previous blog posts on this topic are here, here and here.

- F. Provectus notes, for the first time also: "...a strategic investment strategy."

This, of course, refers to a minority equity investment by Big Pharma, such as Pfizer.

It's clear those money managers interested in but uncommitted as yet to Provectus (i.e., those on the sidelines) are waiting for, in their estimation, the inevitable dilution to come. From their perspective, the company will have to raise money to run the pivotal MM Phase 3 trial and money for day-to-day operating expenses in 2013 and beyond. Their likely varying beliefs as to the difficulty or ease with which Provectus would raise such funds might be informing their approach to and decision-making over buying shares.

The game Peter Culpepper is playing -- or perhaps put differently the strategy he is working to see unfold from a cash balance perspective but in the context of current and future company valuation -- is, rather obviously, trying very hard to close the dermatology deal, a mini-oncology transaction or two and/or a minority strategic equity investment. The upfront cash component of one or more of these transactions would be sufficient to fully fund company operations through the playing out of the end-game.

No comments:

Post a Comment