In investment management, there are several measures of risk-return (aka risk-reward), including alpha, beta and Sharpe Ratio (see, for example,

Forbes' Measuring Risk With Alpha, Beta and Sharpe Ratio by Richard Loth). Most investment professionals and retail investors do not outperform the market. Most investment funds, mutual, hedge or otherwise, after fees and expenses (and, more often than not, before too) do not generate alpha.

Alpha measures the value an investment manager adds to his or her fund portfolio. Warren Buffett,

Jim Simmons,

Ray Dalio, etc. established their reputations by generating lots of alpha for notable periods of times.

Beta measure volatility. A beta greater than 1 means a portfolio (or security) will be more volatile than the market (less than 1 means less volatile, and equal to 1 means the same volatility). Many hedge funds generate high beta; that is, when the market goes up they go up higher, and when the market goes down they go down more. Some funds are low beta ones; they go up less when the market goes up and go down less when the market goes down.

"Investors would most likely prefer a high alpha and a low beta." Sharpe Ratio measures risk-adjusted performance, and

"...tells investors whether an investment's returns are due to smart investment decisions or are the result of excess risk."

While far from a perfect analogy, many or most of the pharmaceutical industry's oncology drugs generate beta. Few, if any, generate real alpha. Most have forgettable Sharpes. Layer on the cost of treatment (i.e., mutual fund costs or hedge fund fees and expenses), only the most effective drugs (i.e., the very best investment managers) deliver a compelling patient (i.e., investor) value proposition.

As I have written before on the blog before, and continue with the above analogy:

- Pharmaceutical Risk = Safety,

- Pharmaceutical Return = Efficacy, and

- Pharmaceutical Fees & Expenses = Treatment Cost.

PV-10 for melanoma (or any of the solid tumor cancers for which it likely should have great potential) is like a very high alpha, very low beta, very inexpensive-to-own fund.

Safe. Efficacious. Broad spectrum of use. Low cost.

January 28th press release:

Provectus Announces PV-10's Assessment for Drug-Drug Interaction Potential is Subject of Article Published by Xenobiotica

Byline: Demonstrates Risk of Clinically Relevant Drug-Drug Interactions with Rose Bengal is Low

Key Statement:

- "The published research indicated that the risk of PV-10 causing clinically relevant drug-drug interactions is likely minimal."

- "Sorafenib is a competitive inhibitor of cytochrome P450 (CYP) drug metabolism enzymes and is reliant on the UDP-glucuronosyltransferase (UGT) pathway for efficient clearance. CYP and UGT enzymes help to biotransform small lipophilic drugs like sorafenib into water-soluble excretable metabolites."

- "As we discuss our clinical results with regulatory authorities, we continue to be intensely committed to building all sections of the prescribing information for a future package insert for PV-10."

The paper's Discussion section helps to place the conclusion of low risk of clinically relevant or significant drug-drug interaction in context, and discusses what is known, what can by hypothesized, what is not known, and what requires or deserves more work.

The paper and the PR begin to reveal more of PV-10's orthogonality (drug-drug interaction) potential. My posts on orthogonality are

here,

here,

here and

here.

Orthogonal, as you know, refers to the the idea of perpendicular, non-overlapping, independently varying or uncorrelated items. Two lines at right angles to each other are perpendicular, or orthogonal.

X, Y and Z axes conventions reflect axes perpendicular (or orthogonal) to each other.

I think there are at least two key takeaways from this work and PR.

First, clinical trial outcome. Sorafenib, co-developed and co-marketed as Nexavar by Bayer and Onyx Pharmaceuticals (

acquired by Amgen in August 2013) is the standard of care for the treatment of advanced hepatocellular carcinoma. The company currently is running

an expanded liver cancer Phase 1 trial comparing sorafenib (cohort 1) to PV-10 plus sorafenib (cohort 2). Sorafenib/Nexavar is not a very good drug, but it remains the go-to-solution for physicians for this disease.

By demonstrating low clinically relevant drug-drug interaction, all or most of the difference in efficacy between cohort 1 and 2 should be attributed, positively (more efficacy in 2 than 1) or negatively (less efficacy in 2 than 1), to PV-10. The trial is permitting

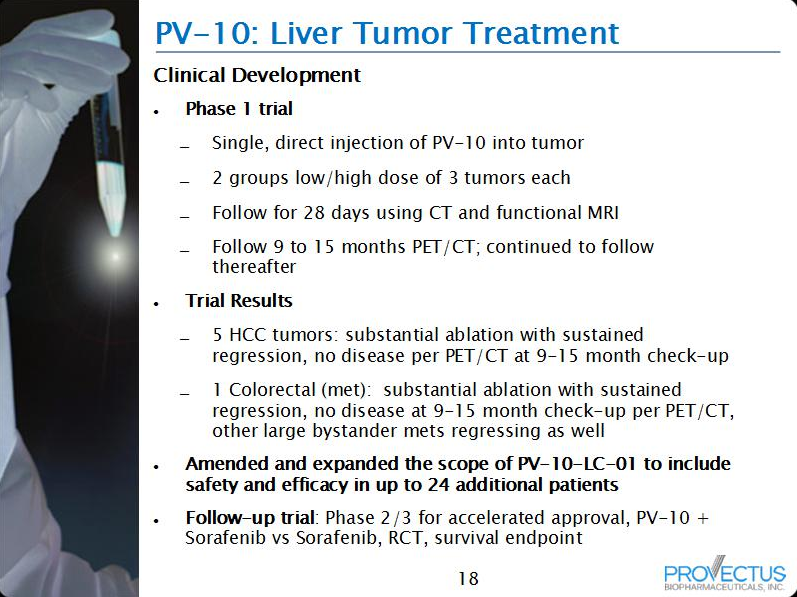

a single intralesional injection of PV-10 in patients with either recurrent hepatocellular carcinoma (HCC) or cancer metastatic to the liver. Success data (higher efficacy in cohort 2 v. cohort 1), likely measurements should include overall response (complete, partial, stable) of injected tumors, would inform the FDA and impress Big Pharma, particularly if they are even remotely close to what was demonstrated for locally advanced cutaneous melanoma. Provectus has not updated the market on its liver cancer Phase 1 trial save this old information from its current website presentation.

|

| Click the figure to enlarge it. |

This biochemistry work published today is very useful for when the company shows its expanded liver trial efficacy results and analysis to the FDA and Pfizer, er, Big Pharma.

Second, market opportunity. "Three fourths of worldwide liver cancer cases in males and two thirds in females occur in the fifteen Asian countries." Sorafenib is not well liked in Asia for its utility (more so than in the U.S.). Sorafenib/Nexavar's price certainly is not liked there either. Nevertheless, the drug is the standard of care, until it is not.

"The drug, which is particularly effective on late-stage kidney and liver cancer,

costs approximately $69,000 per year in India, so in March 2012 an Indian court granted a license to an Indian company to produce to the drug at a 97 percent discount" (quote source, and for the two quotes below, is

here) "Nexavar

costs approximately $96,000 per year in the United States, but Bayer assures “western patients” that they can have access to the drug for a $100 copay." [Bold and underlined emphasis is mine.] "In an interview with Bloomberg Businessweek, Bayer CEO Marijn Dekkers said that his company’s new cancer drug, Nexavar, isn’t “for Indians,” but “for western patients who can afford it.”"

A generic version of Nexavar may hurt Bayer/Amgen. PV-10 reducing Nexavar to near obsolescence certainly won't kill Bayer/Amgen, but the companies certainly will miss the sales (and that will impact earnings to an extent balance sheet financial engineering cannot fix). For example, in the U.S., $96,000 per year for Sorafenib/Nexavar, or a $20,000-30,000 "one shot, one kill," single use (multiple injections, if necessary) 100 mL vial of PV-10. The issue of treatment cost, in the U.S. and around the world, is far from resolved. The market opportunity for liver cancer for PV-10 still remains a very, very large addressable market times PV-10's likely very large market share times some price per treatment.

The lack of drug-drug interaction makes possible the combination of PV-10 and other drug therapies (chemotherapy, immunotherapies). That's, um,

Pfizer and Provectus' joint patent application (Combination of Local and Systemic Immunomodulative Therapies for Enhanced Treatment of Cancer), which should be fully approved later this year.

This biochemistry work published today, assuming expanded liver cancer Phase 1 study data is consistent with other PV-10 liver and other cancer indication tumor results and more work conducted on combination therapies including PV-10 is successful, should open very significant market opportunities for Provectus and PV-10