Last week Reuters' Bill Berkrot wrote an article on Provectus, its drug PV-10 and the drug's active pharmaceutical ingredient Rose Bengal entitled

Old red dye shows promise as new cancer foe. Provectus also initiated a new clinical trial last week entitled

A Phase 1 Study of PV-10 Chemoablation of Neuroendocrine Tumours (NET) Metastatic to the Liver. Some thoughts of mine regarding my takeaways from and questions about them are below.

Article. (1) By far the biggest takeaway for me from Berkrot's article was

the association, finally, between PV-10/Rose Bengal and an immune system response.

The article effectively labeled or categorized PV-10 as an

immunotherapy (at least a potential one), like Bristol-Myers' ipilimumab (Yervoy) and nivolumab (Opdivo), Merck & Co.'s pembrolizumab (Keytruda) and Amgen's talimogene laherparepvec (Imylgic), among others.

PV-10's consideration as an immunotherapy, or potential one, is nothing new given Moffitt Cancer Center's long-time work (presented and published since 2012; first pre-clinical, then clinical) and the University of Illinois at Chicago's more recent work (presented and published since 2015; pre-clinical to date). But, PV-10 hasn't been readily recognized as an immunotherapy or a potential one, despite both pre-clinical and clinical, company and third party work that should have at least encouraged such thinking. I believe this is changing, such as PV-10 and Rose Bengal's treatment in Garbe et al.'s 2016 review paper

Intralesional immunotherapy as a strategy to treat melanoma. See

T cells (February 24, 2016) on

the blog's Current News page for more information.

(2) Another major takeaway for me was the presentation of the article's content, which was came across as

a down-the-middle-of-the-fairway, opening journalistic piece, delivering facts and perspective with little or no opinion, and providing information about Rose Bengal's long, unique history.

Rose Bengal is an industrial chemical that has been around for well over a century. It's been used as a dye. It's been used as food coloring. It's been used as a diagnostic. It's inexpensive to manufacture. Berkrot and/or his editors could have colored some of that perspective, but I think wisely elected not to. In doing so, the article can be a foundational piece of information for those new to or unaware of Rose Bengal, PV-10 and Provectus' stories.

For example, the author wrote:

"While some doctors are encouraged by the research, government approval is years off and not guaranteed. The company must replicate its early results on a bigger scale, and a U.S. Food and Drug Administration decision is not expected before 2019."

Factually true. Provectus' pivotal melanoma Phase 3 trial, per

its ClinicalTrials.gov webpage, has an estimated study completion date of October 2017. Add to this some time for preparation of a new drug application (NDA), a 60-day NDA filing review period and normally a 10-month period for the FDA to review new drugs, and one can easily understand Berkrot's 2019 timeframe. Nowhere in a down-the-middle-of-the-fairway article could there be room for, say, management's guidance of a mid-year interim assessment of efficacy and safety or pursuing accelerated approval on the basis of such data.

In another example, Berkrot wrote:

"In a study of 80 people with advanced melanoma, half of the patients who had all of their lesions injected appeared cancer free after an average of two months. A year later, 11 percent continued to show no signs of cancer, according to a report published the Annals of Surgical Oncology. The lesions were destroyed from the inside with no apparent harm to healthy tissue, researchers said. Reported side effects included injection site pain and blistering."

Again, factually true. PV-10 treatment is safe and potentially effective.

The author does not broach the detail that patients who had all of their lesions injected in the above Phase 2 trial received a second injection of PV-10 into all of their melanoma tumors

two months after the first injection. In Provectus' ongoing Phase 3 trial, patients will have all of their lesions injected

once a month until their lesions go away.

In a third example Berkrot factually and crisply summarizes the goal of this Phase 3 trial, which is to demonstrate PV-10 can prevent or forestall the progression of Stage III melanoma to Stage IV (underlined emphasis below is mine):

"Final results from an ongoing 225-patient melanoma trial of the experimental drug compared to chemotherapy are expected in early 2018. The hope is that the drug, known as PV-10, will prevent melanoma from progressing beyond Stage III, in which the disease has spread but not yet to other organs, and allow patients with more advanced cancer to live longer."

(3) Another minor takeaway would be

Berkrot's take on the discovery of Rose Bengal's therapeutic benefit: an accident, but

what was the real accident?

That Japanese researchers investigating Rose Bengal's food dye version in the 1980s first observed its therapeutic benefit (i.e., dose-dependent survival) but did nothing, or that Big Pharma researchers in their global, decades-long attempts to boil the oceans in search of new drug compounds did not find this work?

(4) A final and minor takeaway is the author

not mentioning anything or making a "big deal" about the local agent's administration (i.e., no specific mention of intralesional (IL) delivery by name; rather, simply the observation PV-10 is injected).

Trial. Takeaways for and questions from me about the initiation of this new clinical trial include:

(1) It's a liver trial.

Specifically, it's a cancer metastatic to the liver or secondary liver cancer trial, rather than a hepatocellular carcinoma (HCC) or primary liver cancer trial.

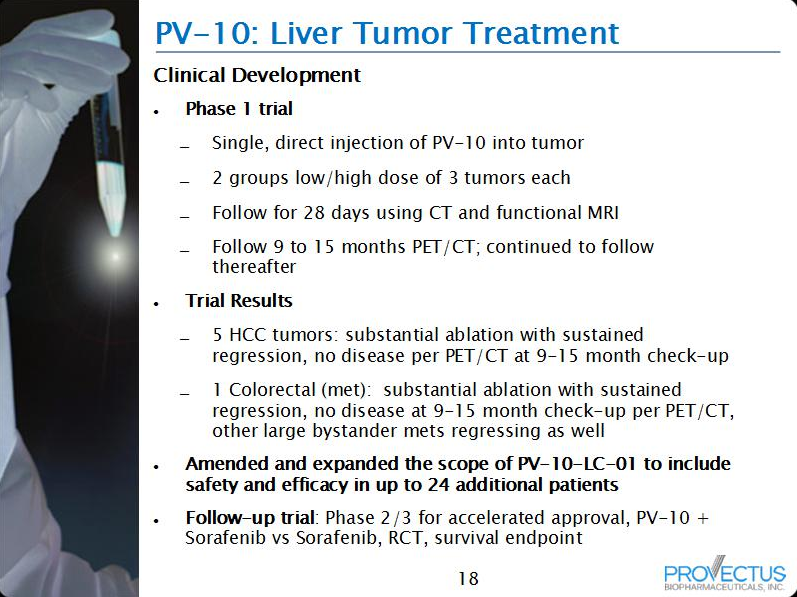

The company currently is running a Phase 1 liver trial,

A Study to Assess PV-10 Chemoablation of Cancer of the Liver, which has explored and is exploring HCC and cancer metastatic to the liver.

Preliminary results from this work noted the treatment of several different types or kids of liver mets including colorectal, non-small cell lung, melanoma, and ovarian. I also previously noted a NET metastatic to the liver had been treated with PV-10. See

New clinical study (February 26, 2016) on

the blog's Current News page for more information.

(2) Where is the previously management-guided progression of the original Phase 1 liver trial?

In

July 2015 presentations of Provectus' preliminary liver cancer data, both HCC and metastatic, the company's CTO Dr. Eric Wachter, PhD indicated the next step in this clinical program would be an Asia-Pacific Phase 1b/2 combination study of HCC (i.e., a single arm trial of regional standard of care + PV-10, followed by a randomized control trial of regional standard of care

+ PV-10).

Why was a NET metastatic liver Phase 1 trial initiated before the Asia-Pacific Phase 1b trial? What is the significance of NET mets?

(3) Dosing and the number of lesions that can be treated have increased.

The original Phase 1 liver trial permitted treatment of a single lesion up to a maximum PV-10 dose of 7.5 mL. As the trial expanded, an expansion cohort (Expansion Cohort 1, or EC1) was established where a single lesion was treated with up to a maximum PV-10 dose of 15 mL.

In addition, the same two-step dosing approach (two cohorts, low and high PV-10 doses: Expansion Cohort 2.1 or EC2.1 and Expansion Cohort 2.1 or EC2.1, respectively) was provided to patients already receiving sorafenib.

The new Phase 1 liver trial will permit treatment of, first, a single lesion up to a maximum PV-10 dose

of 15 mL, and second, if safety is established,

all amenable lesions to a maximum dose of 15 mL.

(4) The new liver trial will collect biomarker, symptom and quality of life data.

The original trial collected changes in markers of hepatic function, pharmacokinetics of PV-10 in the bloodstream following IL injection, and pharmacokinetics of sorafenib in the bloodstream following IL injection.

The full title of the new trial is

A Phase 1 Study to Assess the Safety, Tolerability and Effectiveness of PV-10 Chemoablation of Neuroendocrine Tumours (NET) Metastatic to the Liver in the Reduction of Biochemical Markers and Symptoms Caused by Secretory Products. Information to be collected includes:

- Change in NET biomarkers (chromogranin A or CgA, and/or 5-Hydroxyindole Acetic Acid or 5-HIAA),

- Reduction in major symptoms (diarrhea and flushing) using EORTC QLQ-C30 and GI.NET21 symptom scores vs. baseline values,

- Reduction in other symptoms (including bronchoconstriction and abdominal cramping) using the same approach immediately above, and

- Change in peripheral blood mononuclear cells (PBMC), which was measured by Moffitt Cancer Center's Phase 1 feasibility study.

See NET symptoms below:

(5) Initial efficacy data to be collected in the new liver trial will be objective response rates.

On February 26th the FDA approved Novartis' everolimus (Afinitor) for the treatment of adult patients with progressive, well-differentiated non-functional, NET of gastrointestinal (GI) or lung origin with unresectable, locally advanced or metastatic disease.

From Novartis' pivotal trial "...overall response rates were 2% in the everolimus arm and 1% in the placebo arm. At the planned interim analysis, there was no statistically significant difference in overall survival between arms...Everolimus was discontinued for adverse reactions in 29% of patients and dose reduction or delay was required in 70% of everolimus-treated patients. Serious adverse reactions occurred in 42% of everolimus-treated patients and included 3 fatal events (cardiac failure, respiratory failure, and septic shock)." {Underlined emphasis is mine}

One obviously cannot compare the following for many reasons, but I believe it is worthwhile to note that in Provectus' preliminary liver cancer data, a tumor-specific objective response rate of 50% was achieved -- in 4 patients, however.

(6) I imagine Provectus will press release more information about the new liver trial this coming week.