March Madness 2013

March Madness 2013 begins on Tuesday, March 19 and ends on Monday, April 8.

The Final Four will be played in

the Georgia Dome in

Atlanta, Georgia. I contend this period (including leading into it) will be an important time for the company, its more mainstream awareness, and the share price.

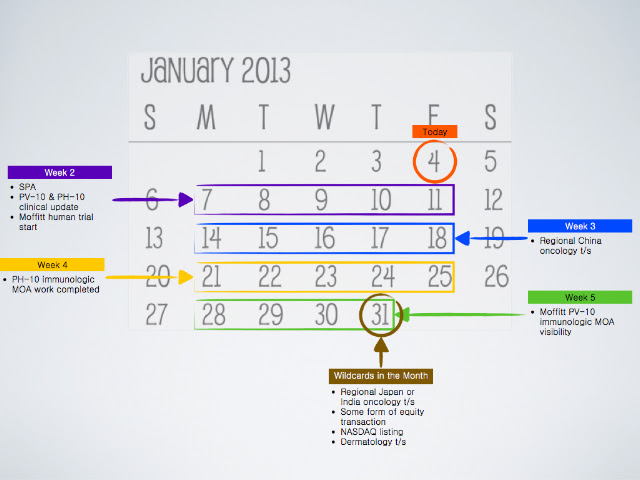

There is a lot of information to digest, from Craig's presentation at

the Noble Financial Capital Markets Ninth Annual Equity Conference to Peter's trip to New York City.

PV-10

Most of Pete’s time lately, probably more than anything else it seems (save for another effort), is focused on communicating PV-10's unique immunotherapeutic characteristics in the context of global oncology. You see this manifested in discussions with Big Pharma (as Craig commented at Noble: "interactions with potential global license partners," and by that he does not include just Pfizer) and continued visiting with life sciences investors (trying to get them off the sidelines and into the stock).

PV-10 + “other stuff”

I think

Craig et al.’s SITC work (PV-10 + systemic chemotherapy),

their upcoming AACR work (PV-10 + systemic immunotherapy), Foote et al.’s expanded work (PV-10 + radiotherapy), and Craig’s skunk works work on more combinatory explorations (e.g., intra-tumoral GM-CSF, systemic interleukin, anti-PD-1 antibodies/agents, etc.) is opening a lot of eyes at Big Pharma and the FDA very wide.

Management is contemplating an MM Phase 1 trial combining PV-10 and ipilimumab (while Craig mentioned this in his Noble presentation, I also followed up). Perhaps the protocol might include the assessment of safety and efficacy in a number of patients with metastatic melanoma (Cohort 1 receives PV-10) and in a number of patients who are taking ipilimumab, an approved treatment for MM (Cohort 2).

As I wrote earlier this week, this combination work of PV-10 + ipi clearly targets and is in response to serious interest from Big Pharma: Bristol-Myers Squibb & ipilimumab/Yervoy and Pfizer/MedImmune-AstraZeneca & tremelimumab (MedImmune in-licensed tremi from Pfizer in 2011 for global development rights to the drug while Pfizer retained rights to specified types of combination therapies).

The liver trials

Let's segue from combination therapies to the expanded liver P1 trial, and what the likely results will mean for the design and very likely outcome of the liver P2/P3 trial. I think there is enough information to speculate (of course, the foundation of the speculation merely is a framework, and not overly substantial) or project success of PV-10 + sorafenib (a systemic drug, so see

PV-10 + other stuff above) over the sorafenib-alone treatment arm. Interference studies and other work confirm PV-10 is orthogonal to sorafenib (and lots of other drugs, too): PV-10 does not interact negatively with sorafenib, and appears to enhance sorafenib's benefit by PV-10 first boosting the immune system.

When Provectus announces -- via an upcoming PR -- that patients have begun to be enrolled and treated in the expanded liver P1 trial, the timeline of results making their way to the FDA should not be lengthy. The same FDA group of folks reviewing Provectus’ pivotal MM Phase 3 trial design suitable for an SPA,

Division of Oncology Products 2 (DOP2), are the same folks (i.e., DOP2) who will review the company’s liver Phase 2/Phase 3 trial design suitable for accelerated approval.

The hard work, time, energy, resources, expense, etc. exerted to get the SPA for MM should pay-off when it comes time for management to request AA for liver.

The SPA

Barring another eleventh hour request or issue, it appears the SPA should arrive around March 15.

While it certainly is possible that the SPA arrives earlier, I am setting my own expectations for the Ides.

Shelf filings

The pulling of the two $50MM common stock filings still are in process with Provectus’ attorneys. Management believes the act of pulling them is form over substance, since the company will not be using them. I think communicating their intended action to pull them and/or the actual act and notification to the market of pulling them is substantive.

The regional license deal for China

Work continues, and the process of arriving at and consummating a deal progresses. Should Pete travel to China again (he visited there in late-November 2012), it would be to close the deal, the announcement of which should follow via PR and 8-K filing.

In terms of setting my own expectations for this item, a deal could get done by or around late-February. If

Celsion's China deal is worth several hundreds of millions of dollars (per the analysts and others commenting on valuation), by comparison I think you're looking at a Provectus China worth at least $1 billion (perhaps as much as $2 billion) with higher upfront, milestone and royalty payments.

India & Japan

As a result of a completed China deal, Provectus’ visibility should be much more pronounced. Deals in India and Japan could follow thereafter, but more of the deal process must progress before I would speculate about timing. India could be accelerate given the level of interest of the top Bio-Pharma players in the country. For now, I’m not setting any expectations.

Moffitt & Reproducibility

Craig expanded in some detail about Moffitt's work in his Noble presentation: their reproduction of his work, his reproduction of their work, their upcoming data release and presentation(s), etc. According to Craig, Moffitt's immunological MOA characterization work results (mouse and human) will be revealed imminently. I think Craig's comments related to reproducibility, particularly in the context of creating and making a product (i.e., PV-10, PH-10), were very important and very true.

I think it is easy, at this point, to connect the dots so as to speculate (identify) about which conference Moffitt will present their highly anticipated results. I still expect forthcoming visibility about these Moffitt results in late-January, and some data released in stages in March, prior to the full dataset being released at the expected conference in early-April.

More valuation-raising work to be done

When I wrote my blog post entitled

$PVCT: Immunologic Potential, and thus Value, I set a very lofty valuation for the company, particularly as it related to the expectation of management for an upfront payment ($3 billion at last check) at the end-game. You don't get from $67.65 million (Google Finance's market capitalization for the company as at 1/25/13) to $3 billion in one leap.

Rather, Provectus arrives there in several leaps and bounds, together with perhaps some end-game auctioning momentum and exuberance: China, India, Dermatology, momentum share buying, etc.

Peer-based management compensation proposal coming

As management noted in a previous filing, a peer company-based bonus compensation structure should be part of a new compensation plan that management should introduce with Provectus' next proxy filing likely in late-April.

PH-10

From a review of history, it appeared Provectus was on the cusp of securing a deal to license its dermatology business (i.e., inflammatory skin disorders) in early-2011. Up to that point, management's valuation expectations, on a net present value (NPV) basis, were about $500 million.

No term sheet materialized from the most serious prospective partner, which would have triggered the official hiring of the financial adviser (Bank of America Merrill Lynch) and an auction process involving the other prospective partners. I think the lack of certain desired information at the time, since fulfilled by the Psoriasis Phase 2c trial, created a valuation gap between the prospective lead and Provectus that prevented the parties from coming together on suitable top-line term sheet parameters. Hence, the prospective lead declined to extend a term sheet it knew would be turned down management.

As time progressed (i.e., as the psoriasis Phase 2c trial was completed), a process appears to have been established that paralleled Moffitt's work on PV-10. Namely, a world renowned cancer research center engaged in work, initially at their own expense, to explore and characterize the immunological mechanism of action of Provectus' oncology drug.

In addition to better understanding PH-10 immunologic MOA, and on a related note, more insight into the drug's distinct lack of toxicity is necessary to better inform the FDA and assist in the design of the eventual Phase 3 trial.

It is not unreasonable to analogize PV-10's path to PH-10's, and thus potentially explain the delay in getting to a dermatology license or sale transaction. Immunologic mechanism of action characterization work is being done on PH-10 by

a world-class institution to complete the understanding of certain prospective dermatology licensees before they fully commit to jumping into the pool. I think management's NPV figure for the dermatology business has increased significantly to at least $750 million (perhaps as much as $1 billion).

As for expectations, Craig did note in his Noble Presentation that we should look for the company to request a end-of-Phase-II (EOP2) meeting with the FDA. Presumably this announcement, if one is made by the company, or step precedes or signals the extension of a term sheet for dermatology is imminent, inbound or at least very close at hand.

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)