Links to news items from July 2013 to [earlier in] May 2016 may be found on the Archived News page.

Hey batta batta batta swing batta batta (October 19, 2016)

Updated below: 10/26/16.

In tracking (diligencing) Provectus intellectual property portfolio, two of three daughter patent applications -- all continuations of August 2015-awarded patent Combination of local and systemic immunomodulative therapies for enhanced treatment of cancer (#9,107,887) -- received final rejection notices from the US PTO; '309 (application #14/748,579) on September 23rd and '318 (#14/748,634) on October 12th. '165 (#14/748,608) remains in process as of October 17th. In trying to break my investment thesis while at the same time openly discussing my ongoing due diligence on Provectus, I believe it's important to highlight both successes and failures, or in this case more work that can and very likely will be done to become successful again.

Updated (10/26/16): '165 (#14/748,608) received a final rejection notice on October 18th.I do not read too much into these final rejections.

The process of prosecuting a patent application is a bit like going to bat in baseball, where there are, in general, three strikes before you are out (i.e., receive a final rejection). The are exceptions, however, such as when an examiner makes an office action "final" earlier if he or she feel the application is not advancing prosecution of the case, or when the applicant resets the strike counter by filing a "request for continued examination" (RCE) (which requires remittance of an additional fee to the US PTO).

- "Request for continued examination: A request for continued examination (RCE) is a request by an applicant for continued prosecution after the patent office has issued a "final" rejection or after prosecution "on the merits" has been closed (for example by a Notice of Allowance (NOA)). An RCE is not considered a continuing patent application - rather, prosecution of the pending application is reopened. The inventor pays an additional filing fee and continues to argue his case with the patent examiner." (source: "Continuing patent application" Wikipedia page

As a recipient of over 30 U.S. letters patent, Provectus CTO Dr. Eric Wachter, PhD has been at bat many times, struck out many times, but appears to have rarely failed to gain coverage of an invention.

Updated below: 10/18/16.

|

| Click to enlarge. Image source |

Intralesional PV-10 should be discussed:

|

| Click to enlarge |

- Dr. Jun Guo, MD, PhD, Peking University Cancer Hospital (China),

- Dr. Georgina Long, MD, Unversity of Syndey/Melanoma Institute of Australia (Austalia),

- Dr. Sanjiv Agarwala, MD, Temple University School of Medicine/St. Luke's (USA),

- Dr. Merrick Ross, MD, MD Anderson (USA),

- Dr. Axel Hauschild, MD, University Hospital, Schleswig-Holstein (Germany),

- Dr. Robert Andtbacka, MD, University of Utah/Huntsman Cancer Institute (USA), and

- Dr. Grant McArthur, MD, Peter MacCallum Cancer Center (Australia).

This or That redux. InvestorVillage poster pvct-whale (aka pvct in cleveland, PVCT Fixer) (newer discussion board [8/16-], old board [11/14-8/16]) listed purported catalysts and news items, and provided commentary too. I think it is worthwhile to review that post in the context of my table under This or That (October 15, 2016) below.

- 'Allegedly', 2 pretty serious suitors for ph-10 offering upfront money. Their ph10 consultant and their industry thought leaders going through the 'process'. What are the names of the serious suitors (e.g., has one of them been here/there before)?

- Liver by end of year. Has a decision been made to present expanded liver Phase 1 data at ESMO Asia 2016 in December (Singapore) or APASL 2017 in February (2017)? See An Incomplete Story (October 5, 2016) below.

- pediatric combo trial with NYC hospital by end of year. Is it PV-10 as a monotherapy, or in combination with another drug or agent? Is it one hospital or a consortium of institutions? Has preclinical work been conducted? Has drug been shipped?

- If possible pediatric use of PV-10 is true, how absolutely baffling would that be? [partly sarcastic] An unapproved, "local" agent being contemplated for the treatment of systemic disease in children. "Crazy!"

- another Reuters article 'shortly" Why not?

- combo data 1stQ of 2017. I believe the goal is to have data in a form for prospective partners to review by the end of the year, although such timing of course could slip. I imagine data in presentable or poster form would be ready in the new year at the earliest. See An Incomplete Story (October 5, 2016) below.

- 6 more sites coming on line by end of year & interim pushed back 8-12mths from now Timing, subjective as it is because of the [somewhat] subjectivity of the number of events required to trigger an interim analysis of Provectus' pivotal melanoma Phase 3 trial, depends of course on the number of sites and the number of patients each site recruits. See 81 (October 12, 2016) below. Eight to twelve months is a WAG, but then again my "clinical trial math" could be too.

- Peter, Eric, and Tim all ponying up big for the rights offering. Peter selling his gold and putting half his net worth into this next raise. Why wouldn't they, if they did not believe in the drug and its potential (or likely) approvability, which is essential and fundamental to any investment thesis. We heard at the end of the 2000s that melanoma had been solved. Sadly, for patients, this proved not to be true. We hear today that immuno-oncology (IO) is the key to beating cancer. But, as Dr. Jim Allison, PhD observed at the Vatican Conference on Regenerative Medicine in April, we need to make big advances to move from occasional cures to routine cures. This will take multiple tools. Provectus CTO Dr. Eric Wachter, PhD has invested almost 20 years in one tool, so I believe his position is clear. [Company COO and interim CEO] Peter and his gold...what a strange cat :)

- Network1 says they have the solution and that they can fix this company. Mngt shakeup, and get their people on the board so they can control it. Oh and wants Peter to put up the ip as collateral for this next raise in case the company goes under. Have you met or spoken to Damon Testaverde (or, in the case of his son Keith, received an email from him...) or Bill Hemming, among other Network 1 folks? I suppose we could be who we are, unless we work hard to be who we think and hope it's better, more productive, more contributory, more collaborative, and more fun to be. It is unlikely brown shoe stock brokers would have a meaningful, substantive and potentially successful solution to fix Provectus, to the extent some parts of it require modifications, additions and changes. But I can't be too mad at Damon and his crowd, or Maxim or whomever... Peter and the independent directors employed them after all in roles and capacities when better decisions and choices clearly could have been made and implement.

Will you be there at the end, and why?

When it absolutely, positively has to be there... (October 17, 2016)

Updated below: 10/17/16.

H/t a regular hatter (AL): More blocking and tackling [work] to advance the PV-10 trademark:

Updated (10/17/16): Explanation: To validate the trademark pending application for "PV-10," it was necessary to show use of the mark in commerce. In this case, the example illustrates a shipping container used for transport of vials of PV-10 from one party to another. To stanch any conclusion that "in commerce" meant Provectus was selling PV-10, this could include non-commercial examples. The above is an example of the label used for shipment of PV-10 to any recipient (e.g., clinical site, testing laboratory, etc).

Updated below: 10/17/16.

H/t a regular hatter (AL): More blocking and tackling [work] to advance the PV-10 trademark:

- October 14th: Trademark Snap Shot Amendment & Mail Processing Stylesheet, and

- September 26th: Specimen

|

| Click to enlarge. |

|

| Image source |

Updated below: 10/15/16, 10/16/16 {twice}, 10/17/16 {thrice} and 10/18/16.

While persevere in this evening's press release could be viewed as the ridiculous use of a word with a negative connotation in this context (dedicated might have been better messaging), Provectus' COO and interim CEO Peter Culpepper made an interesting comment: "...we intend to be active in our communication with stockholders up to and including our quarterly investor conference call in November..." I would speculate the call might held during the second week of November (the week of the 7th); the special shareholder meeting is on the following week on the 14th.

Does one buy common shares now ("this"), or wait until the rights offering in December to buy by participating ("that"), or both? What's the value proposition or risk-reward of this versus that? I believe, like others, that the answers depend on what if any news comes out between now and the deal's pricing, and thus the potential impact on the share price as a result. Does one buy before the supposed news, or wait and see what if anything materializes before deciding to buy?

A very real challenge to Peter's intent to be "active" in company communications to stockholders, however, will be Provectus CTO Dr. Eric Wachter, PhD, and what Eric feels comfortable saying on the call about clinical development program progress -- outside of expected or possible newsflow in the coming weeks and before the end of the year. That is, Eric is much more likely for information to be made public by others before he is willing or understanding enough to provide prior guidance.

All that truly is known in regards to timing (SITC 2016, November 9th to 13th) is Moffitt Cancer Center's poster presentation of murine model work combining PV-10 and chemotherapy (standard of care gemcitabine, I speculate) for pancreatic cancer. I imagine management's eventual decision, presumably for 2017, is whether to initiate an early-stage clinical trial for this tumor type (and thus whatever cancer indication is appropriate).

Updated (10/15/16).1: I had shared an October 7th article from The Cancer Letter entitled "With 20 Agents, 803 Trials, and 166,736 Patient Slots, Is Pharma Investing Too Heavily in PD-1 Drug Development?" (author: Laura Brawley) with Eric.

Provectus is not doing the same thing everyone else is doing: e.g., a small molecule, no biosafety restrictions, no cryogenic cold chain, no treatment over and over and over, etc. I can appreciate it must be more than a little frustrating to Eric that he isn't pursuing an oncolytic virus, which probably would be easier* -- but then he knows fully well he'd have to give up on the potential to actually change the standard of care in cancer treatment.

* I'm jesting here, or being sarcastic, in some regards.

Updated (10/16/16).2: Returning to the core thought underlying this news entry, Peter's very real challenge regarding Eric's current handling of data and, I believe, desire not to publicly communicate such data (and, as importantly, rationale [among other things] for generating it) quicker, as I noted above, all that is known in regards to timing is Moffitt's poster presentation of preclinical work combining PV-10 and chemotherapy for pancreatic cancer. I speculate (guess) away below, however (the below is very much a work in progress):

Updated (10/16/16).3: Data drive deals. Given the issues, perhaps among others, of (i) the complexity of pertinent dataset and (ii) Eric's desire for rigorous scientific validation, can he prepare the various datasets in a form and format for the company to achieve critical deal, collaboration, relationship or transactions milestones? In some ways the answer to this question drives the answers to those I first asked: e.g., does one buy common shares now, or wait until the rights offering?

Updated (10/15/16).1: I had shared an October 7th article from The Cancer Letter entitled "With 20 Agents, 803 Trials, and 166,736 Patient Slots, Is Pharma Investing Too Heavily in PD-1 Drug Development?" (author: Laura Brawley) with Eric.

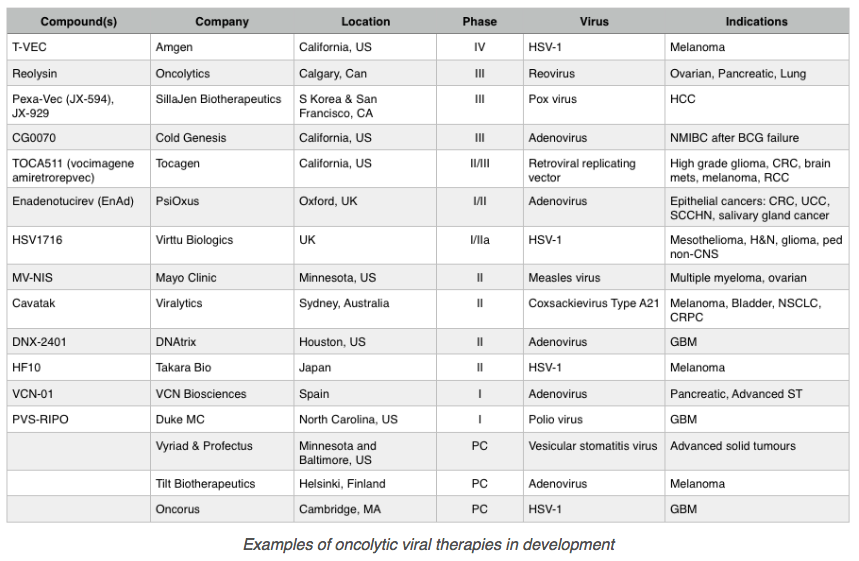

What could possibly be wrong with putting all eggs in one basket? But this is indeed a common theme in the industry. Once an approach is validated “everyone” follows it. I was struck at ESMO by the number of studies in the intralesional space, just in melanoma. This is to a smaller extent an example where Imlygic’s approval has “validated” the concept and makes it more attractive for companies to pursue.Consider oncolytic virus companies Takara Bio (Japan, agent: HF10, trial protocol) and Genelux (San Diego & Germany, GL-ONC1, trial protocol). These examples illustrate Eric's point (I'd put it another way) about the biopharmaceutical industry being filled with followers and me toos.

Clearly these sponsors are attempting to duplicate the success of Imlygic with equivalent products. The study designs shown at ESMO for these products were all remarkably similar, down to the details of administration (dose schedule).It's hard not to address the 800 lb gorilla in this room, which is why all of these oncolytic viruses (e.g., herpes, coxsackie, vaccinia, etc.) need to be given (a) so often and (b) for so long. They are purported to replicate and spread, and are detected throughout the patient. They also produce "flu-like" symptoms, which presumably means they are causing active infections. But, in contrast, prophylactic vaccines do not require 12 to 20 courses, and exposure to the wild types of these viruses that typically leads to disease on minimal initial exposure.

Provectus is not doing the same thing everyone else is doing: e.g., a small molecule, no biosafety restrictions, no cryogenic cold chain, no treatment over and over and over, etc. I can appreciate it must be more than a little frustrating to Eric that he isn't pursuing an oncolytic virus, which probably would be easier* -- but then he knows fully well he'd have to give up on the potential to actually change the standard of care in cancer treatment.

* I'm jesting here, or being sarcastic, in some regards.

Updated (10/16/16).2: Returning to the core thought underlying this news entry, Peter's very real challenge regarding Eric's current handling of data and, I believe, desire not to publicly communicate such data (and, as importantly, rationale [among other things] for generating it) quicker, as I noted above, all that is known in regards to timing is Moffitt's poster presentation of preclinical work combining PV-10 and chemotherapy for pancreatic cancer. I speculate (guess) away below, however (the below is very much a work in progress):

|

| Click to enlarge. |

Two key opportunities potentially/possibly present themselves this quarter. First, one could presume a PH-10 license deal requires a successful end-of-Phase 2 (EOP2) meeting with the FDA. For when is the meeting scheduled? Second, a multi-indication collaboration between a Big Pharma and its immune checkpoint inhibitor, and Provectus and PV-10, presumably requires (a) preliminary data from the Phase 1b study of PV-10 and pembrolizumab for advanced melanoma and (b) some or whatever data from the Provectus' immune biomarker work. When could Eric provide this information to prospective partners?

Of course, if management pulls one or both of the above off, would there be a need for the rights offering?

Updated (10/17/16).4: [i] I am grateful to a shareholder who shared [what I nerdily and rightfully refer to as] due diligence materials he or she recently gathered. My perspective along this journey has long been influenced by fellow retail shareholders who are smart and intelligent, are outsiders and not insiders, and who may or may not know how the game is played or be able (or choose not) to play it, but always have been willing to share data, information and knowledge in hopes that collectively we are better prepared to survive and potentially (hopefully) prosper (i.e., garner a return on capital, rather than a return of a fraction of capital) from the "game." Yet, without such input and insight, we truly are left at the mercies of those who have more information (I tell my students Wall Street isn't necessarily smarter that Main Street, but typically or usually better at information arbitrage than the rest of us). I have encouraged him or her to share their information with the newer InvestorVillage Provectus stock discussion board.

[iii] It is clear some folks are taking sides, so to speak. I don't believe Network 1 believes Provectus will achieve any key bridge events (my terminology, not theirs) before a rights offering is done.

[iv] A new Merck & Co. location visited the blogging, reading (among other things) September 5, 2015 blog post Trendwatching, and exiting via the linked picture below.

[v] Terminology. The end of the valuation and transactional bridge should the outcome of the pivotal melanoma Phase 3 trial (one could reasonably argue several aspects of it, like a data monitoring committee pre-call, an interim data readout, preliminary full data, etc.). Bridge events would include a PH-10 license, a co-development collaboration combining PV-10 with another checkpoint inhibitor, etc.

Updated (10/17/16).5: [a] As I noted below under An Incomplete Story (October 5, 2016), InvestorVillage Warlord is a good recent follow. For this news entry update, see here and here. In his latter post Warlord wrote "No bp has seen the ph-10 Moa because it has to go to FDA first. The top researchers and management has seen this and it should be big when it gets out. But bp needs to wait." In my best IV poster STARLIGHT66 impression, I am led to believe prospective partners have seen mechanism of action data.

[b] Another round of PH-10 rumors surfaced today regarding intellectual property (IP). Speaking of STARLIGHT66, he engaged in such here. In doing deals where IP is important, let alone critical, addressing the topic [in detail] as part of a transaction often is done after a "go" business decision (as opposed to "no go") has been made. So, it is likely upfront, milestone and royalty payment discussions already have been had.

[c] I noted under Friday (September 23, 2016) the rumor that mechanism of action data is/has been available for prospective partners (and that Seth Orlow has been doing the rounds with it). Some days thereafter STARLIGHT66 posted (and later deleted his post) regarding [some] prospective deal terms in reply to IV poster canis_star; it was something to the effect of a $30-40 million upfront payment and a $1B deal value. With his (STARLIGHT66's) follow-up post regarding "all or nothing at all" on the IP, which clearly undervalues the company (i.e., oncology + dermatology* vs. dermatology only), it strikes me folks could be beginning to price Provectus.

* If am to read STARLIGHT66 properly.

[d] Visitor. Wachtell, Lipton, Rosen & Katz recently visited the blog. The law firm has been Pfizer's outside M&A counsel (e.g., Allergan, Anacor, Medivation).

Clinical Trial Status Update: Melanoma P3 (October 13, 2016)Of course, if management pulls one or both of the above off, would there be a need for the rights offering?

Updated (10/17/16).4: [i] I am grateful to a shareholder who shared [what I nerdily and rightfully refer to as] due diligence materials he or she recently gathered. My perspective along this journey has long been influenced by fellow retail shareholders who are smart and intelligent, are outsiders and not insiders, and who may or may not know how the game is played or be able (or choose not) to play it, but always have been willing to share data, information and knowledge in hopes that collectively we are better prepared to survive and potentially (hopefully) prosper (i.e., garner a return on capital, rather than a return of a fraction of capital) from the "game." Yet, without such input and insight, we truly are left at the mercies of those who have more information (I tell my students Wall Street isn't necessarily smarter that Main Street, but typically or usually better at information arbitrage than the rest of us). I have encouraged him or her to share their information with the newer InvestorVillage Provectus stock discussion board.

Updated (10/18/17).7: InvestorVillage poster pacificnorthwest1 posted the due diligence material I referred to above, her notes of a conversation with a Maxim Group (and former Network 1) stock broker historically involved with Provectus.[ii] In response to InvestorVillage poster leave_the_gun, I implicitly assumed a third possibility, of buying after the rights offering, was part and parcel of the second possibility of participating in the offering itself -- because (appealing to the efficient markets hypothesis, in context and FWIW) I assumed one would get as good a price in the deal as after it (where I assumed the stock market wouldn't dramatically over or under react to the transaction). leave_the_gun appropriately corrects me in that some existing or prospective shareholders would want to see, as a further datapoint, how the stock market would reacts (ingests information) to the rights offering pricing.

[iii] It is clear some folks are taking sides, so to speak. I don't believe Network 1 believes Provectus will achieve any key bridge events (my terminology, not theirs) before a rights offering is done.

[iv] A new Merck & Co. location visited the blogging, reading (among other things) September 5, 2015 blog post Trendwatching, and exiting via the linked picture below.

|

| Click to enlarge. Visitor exit link |

Updated (10/17/16).5: [a] As I noted below under An Incomplete Story (October 5, 2016), InvestorVillage Warlord is a good recent follow. For this news entry update, see here and here. In his latter post Warlord wrote "No bp has seen the ph-10 Moa because it has to go to FDA first. The top researchers and management has seen this and it should be big when it gets out. But bp needs to wait." In my best IV poster STARLIGHT66 impression, I am led to believe prospective partners have seen mechanism of action data.

[b] Another round of PH-10 rumors surfaced today regarding intellectual property (IP). Speaking of STARLIGHT66, he engaged in such here. In doing deals where IP is important, let alone critical, addressing the topic [in detail] as part of a transaction often is done after a "go" business decision (as opposed to "no go") has been made. So, it is likely upfront, milestone and royalty payment discussions already have been had.

[c] I noted under Friday (September 23, 2016) the rumor that mechanism of action data is/has been available for prospective partners (and that Seth Orlow has been doing the rounds with it). Some days thereafter STARLIGHT66 posted (and later deleted his post) regarding [some] prospective deal terms in reply to IV poster canis_star; it was something to the effect of a $30-40 million upfront payment and a $1B deal value. With his (STARLIGHT66's) follow-up post regarding "all or nothing at all" on the IP, which clearly undervalues the company (i.e., oncology + dermatology* vs. dermatology only), it strikes me folks could be beginning to price Provectus.

* If am to read STARLIGHT66 properly.

[d] Visitor. Wachtell, Lipton, Rosen & Katz recently visited the blog. The law firm has been Pfizer's outside M&A counsel (e.g., Allergan, Anacor, Medivation).

Updated (10/17/16).6: Wachtell Lipton last visited September 2015.

Updated below: 10/13/16 {thrice}, 10/14/16 and 10/15/16.

H/t a regular hatter, PV-10 vs Chemotherapy or Oncolytic Viral Therapy for Treatment of Locally Advanced Cutaneous Melanoma, new site:

|

| Click to enlarge |

Updated (10/13/16).2: Thing one. Trading on the NYSE MKT in common stock (PVCT) and warrants (PVCT.WS) was suspended because the common share price dropped below 6 cents.

Updated (10/14/16).4: Provectus issued a press release today related to the above mentioned trading suspension and re-trading of the stock and warrants on another exchange, "Trading in Provectus Biopharmaceuticals Common Stock and Warrants Suspended by NYSE MKT." As of this writing no associated 8-K was filed.

Of note to me were two statements and quotes. First: "In an effort to regain compliance with the listing standards of the NYSE MKT, the Company filed a preliminary proxy statement with the SEC on October 5, 2016 to request that its stockholders approve, at a special meeting of stockholders to be held on Monday, November 14, 2016, at 1:00 p.m. Eastern Time at 265 Brookview Centre Way, Suite 600, Knoxville, Tennessee 37919, among other items, a reverse stock split, which will be at the discretion of the Company's board of directors to effectuate if the proposal receives the requisite stockholder approval at the special meeting. The reverse stock split, if approved by stockholders and effectuated by the Company's board of directors, will combine each 10 to 50 shares of common stock (with the exact ratio to be determined in the sole discretion of the Company's board of directors) into one new share of common stock, and will increase the price of the Company's common stock accordingly. A reverse stock split will be necessary for the Company to maintain its listing on the NYSE MKT, unless the Company's stock price begins trading at higher levels for a sustainable period of time.

There can be no assurance, however, that the Company's stockholders will approve the reverse stock split. Even if stockholders approve the reverse stock split and the Company effectuates the reverse stock split, the Company may still be subject to delisting if the price of its common stock again falls below $0.06 or fails to rise above $0.20 and the Company is not otherwise able to meet applicable listing requirements of the NYSE MKT."

I would imagine stockholder approval of an increase in the number of authorized shares is more likely than approval of a reverse split. I am hard pressed to believe management wants a reverse split.

Second, "Peter R. Culpepper, Interim CEO and COO of Provectus, stated, "we are committed to persevere in our efforts for both patients and stockholders to win, and we intend to be active in our communication with stockholders up to and including our quarterly investor conference call in November, which is planned to coincide with the filing of our Quarterly Report on Form 10-Q for the quarter ended September 30, 2016 with the SEC.""

I'm pleased to know Peter (and presumably Eric) are committed to persevering, like the protagonist in the Unbroken story; however, Louis Zamperini was a former Olympic track star. As such, both persistence and competence, among other important traits, come into play. I certainly do not think Peter and Eric, individually and collectively, have been as competent in each of their respective roles and various responsibilities as they could have been. If we don't seek to examine different ways of doing things that are best practices at best (or better practices than we're currently engaged in at worst), especially if they are in fields or areas where we have no or little experience, we might be persistent but all that crosses the finish line is the withered carcass of underwater stockholders.Thing two. Provectus COO and interim CEO Peter Culpepper is speaking to two groups of shareholders on the East Coast today. Feedback from one such meeting (i.e., folks who I think are purely shareholders, as opposed to the other group who include broker-dealers) was a tad startling. These folks have had a historically poor view of management, including and especially of Peter, who has been their primary interface over the years. Without putting too many words in their collective mouth, it probably is not too far from the truth to say they previously despised him (at least that's my interpretation or read of the situation). Yet, they apparently walked away being impressed with Peter, presumably both in what he said and how he said it. One attendee now appears convinced core management will prevail. Of company CTO Dr. Eric Wachter, PhD (I assume), said individual also now believes he no longer is the wise guy trying to get things done outside of normal FDA guidance.

Updated (10/14/16).4: Peter [apparently] also met with Network 1 folks (management, I believe, and not necessarily clients). There was a rumor circulating today that the firm, presumably through the selling of clients' Provectus holdings, was responsible for driving the share price below the 6-cent listing threshold on Thursday morning. I wouldn't have thought Network 1 would have that those many shares to drop the share price nor the intent to do so. But what do I know?

While the meeting may have been a positive one for either or both parties (Network 1, Peter), I have to wonder how Network 1 can be of help to Provectus. What is Network 1's current motivation to help, assuming of course the rumor of getting clients to previously sell out of their Provectus positions is true? I would have to imagine it is the millions and millions of non-tradeable warrants the firm and its clients still hold. You have to wonder whether (and under what circumstances) they could or would ask Peter for (or demand from him) a repricing of these warrants' exercise prices.

Updated (10/15/16).5: I do not have a favorable opinion of management and employees of Network 1 and Maxim. I have tried over time to coach (I use this term somewhat lightly, and do not mean to be overly presumptuous) Peter in regards to aspects of his role and responsibilities. Eric and he have grown as executives, managers and industry professionals on the dime of past and present retail shareholders. Peter has been, at various times, one or more of inexperienced, naive, lazy, forced, etc. in his use of these firms to fundraise. That he may or may not have been ripped a new one is of no consequence (I appreciate him taking one for the "team") if he does not further use or kowtow to Network 1.

As an aside, I have been a paid or volunteer board member, board observer, advisory board member, and committee member for nearly 20 privately held companies and nonprofits over the years. Speaking of potential new orifices, I currently sit on the audit and finance committee of one of the largest (sadly) non-profits of its kind in the country (to provide some domain expertise the committee previously was lacking). It has an annual budget far in excess of Provectus'. I am humbled every quarter by a fellow committee member's intelligence, pragmatism, detail-orientedness, persistence and outspokenness (when appropriate) when reviewing entity materials and discussing them with management (sometimes I am almost humiliated by the degree of her competency, and find myself always grateful to her for the learning experience).Updated (10/13/16).3: Immune biomarkers. In an August 2016 paper led by an OncoSec-related clinical investigator, Dr. Adil Daud, MD, "Tumor immune profiling predicts response to anti–PD-1 therapy in human melanoma," it was noted that:

"It is becoming increasingly clear that the immune composition in tumors is markedly different from that observed in peripheral blood. Thus, robust biomarkers that predict response to immunotherapy will most likely be derived from tumor tissue."I asked Eric if he needed to address immune biomarkers with tissue samples? The Phase 1b study combining PV-10 and pembrolizumab in patients with advanced (Stage IV) melanoma had as one of its secondary endpoints change in immune biomarkers (peripheral blood mononuclear cells [PBMCs] assessed versus baseline values for changes in T cell populations).

He replied: These two aspects of immune response are not directly related. In our case, markers in blood are upstream indicators of immune activation by PV-10 ablation. In the work you cite, it is being noted that the presence of immune cells in tumors, and certain genetic characteristics of tumors (such as extent of PD-L1 expression) are prognostic for response to checkpoint inhibition. This latter concept is proving highly relevant in lung cancer (n.b., recent differences in the outcomes of Phase 3 studies of anti-PD-1 in lung cancer using different thresholds for PD-L1 expression). For melanoma the jury is at best still out regarding such relevance.

81 (October 12, 2016)

I believe Provectus management, specially company CTO Dr. Eric Wachter, PhD, needs to start an accurate, understandable, honest dialogue with shareholders -- sooner rather than later -- of the status of the company's clinical development program's many parts.

As I noted under Biological basis (October 11, 2016) below, Eric said (on Provectus' August 10th business update call) the triggers for the interim and final interim assessment of efficacy and safety for the company's pivotal melanoma Phase 3 trial were the generation of 81 and 162 events, respectively. The contemplated trial enrollment (N) is 225, so that 81 events for an interim analysis would have been designed out of 113 patients (or half of N).

Since the trial is randomized two-to-one (treatment arm-to-control arm), of the 81 events that are assumed to occur or needed to occur in order for the interim analysis to be triggered, 54 of them would or are needed to fall in the treatment arm and 27 in the control arm. This equivalent or same behavior is the so-called "null hypothesis;" that is, both arms are assumed to behave the same.

The prevalent or consensus thinking is that (i) few-to-no events would occur in the PV-10 treatment arm because there would be no progressions of the injected target lesions, while (ii) many-to-all progressions (events) would occur in the chemotherapy and oncolytic virus (T-Vec) control arm. So, while the null hypothesis (at the outset of the trial) is that the two arms behave the same, the alternative hypothesis (borne out by the trial's outcome) is that the two arms behave very differently (i.e., there are far fewer events in the treatment arm, and far more in the control).

If 27 events are required, the study then must recruit 81 patients, or maybe more, to generate 27 ( you can see I am playing around in absolutes for ease of math).

But does the trial need to register 27 events in the control arm in order to trigger an interim analysis? I don't believe so; however, I think the threshold figure is a subjective decision (that would be made by the study's data monitoring committee (DMC). I point to Eric's comments from the August 10th call:

"And so, we are able to monitor at the terminal end of the study, and if the clinical trial data monitoring committee determines that it's in the best interest to end the study, it could end before we had all of the progression events occurring. I doubt that'll happen. It will be a very unusual circumstance, but it would probably be positive for the drug because it would suggest that a large number of patients weren't progressing because of the majority of the patients in a two-to-one randomized study are from the PV-10 arm, and that probably would imply that the PV-10 patients weren't progressing."As I also noted below, one cannot consider the 27 or less [expected] control arm events (out of 27 patients) in a vacuum, but rather in relation to the number of events generated in the treatment arm -- the [expected] "imbalance."

In the eyes and minds of the DMC, what is the presumably subjective (but with some form of objectivity vis a vis statistical significance) imbalance threshold that would allow them to establish what indeed is in the best interests of the study's patients?

27 control arm events vs. zero or a few treatment arm ones? 20-to-0 or a few? 15-to-0 or a few?

Multiply these numbers by three, and you arrive at the number patients required to be treated (assuming, of course, extreme arm performance): 81, 60 and 45, respectively. I've written about this before; see August 13, 2016 blog post The Untrigger, where I projected enough patients by/in January 2017 (1Q17):

"Rather than hash out or re-hash my work/writing about prescribed event and time triggers, the number of patients needed to be enrolled to hit 81 events, etc., I'd like to state (speculate) the following -- [I believe] there is a trigger Eric does not want to explicitly speak about or affirm, which could/would be an imbalance in the number of events between the treatment and control arms, which could/would cause a statistical and ethical dilemma for the study's IRC. What would an imbalance look like or comprise? In the extreme, or potentially actually, there would be no events in the PV-10 treatment arm, and events of whatever frequency or magnitude in the chemotherapy/oncolytic virus control arm. Takeaway: The pivotal trial does not have to reach 81 events for the interim analysis to be triggered...

The statistical dilemma is having a treatment arm with no or very few events, and a control arm with many, many more (like 0 and 15, or 0 and 20). The ethical dilemma is a treatment arm that works and works very, very well (i.e., no disease progression), and a control arm that demonstrates what everyone already predicted (i.e., everybody progresses).

The question then would be, "how many events in total and across the two arms would be required for the IRC to recognize an imbalance, and thus trigger the interim analysis?" Twenty events in the control arm (and none in the treatment arm)? Thirty? A two-to-one study randomization then would suggest enrollment and treatment of 60 patients. Or 90.

Math, math, math."What leads me to believe some number less than 27 is required has been Eric's insistence on utilizing a handful of clinical trial sites. Notwithstanding gaudy efficacy (albeit more locally oriented than systemic) and near-pristine safety results, breakthrough therapy designation (BTD) was denied on the basis of a paucity of data (not poor data). There was chatter coming from management that some key opinion leaders (KOLs) believed the Phase 3 trial design was unethical because of the inclusion of chemotherapy as the original and initial comparator for this patient, where clinical trial is the preferred approach to treatment. Yet, setting aside the process and time taken to account for the approval of fellow intralesional (IL) T-Vec (for advanced melanoma), 20 months into the study Eric only has six sites recruiting in the U.S. and Australia. Rather than say site activation was/has been "in process" (Provectus COO, and interim CEO Peter Culpepper's words), I believe Eric chose to have a smaller number of high quality sites (sites where he knew experienced investigators could administer PV-10 properly and effectively) to get to his low threshold of control arm events, rather than a larger number of sites to potentially get there faster but with perhaps greater uncertainty over the predicted outcome.

Except that, and this was well established prior to the commencement of the trial, it was going to be a challenge to recruit patients because of the trial design, particularly only being allowed to use as target lesions those cutaneous melanoma/disease locations. In addition, it also appears to me that sites were not providing him with the expected numbers of patients, particularly in Australia. And all he needed was a "few" patients whose outcome was reasonably well predicted in both arms to generate the information he needed to drop into the data module of the new drug application that was ready to go...

Not that patients were not being recruited. Not that something was "wrong" with the trial protocol. Not that he "couldn't" get sites up and running. Not that something, somewhere was "wrong."

Rather, after having his butt handed to him Eric wanted to him when he thought BTD was a done deal (and, likely now in hindsight, with a [this] pivotal trial as what would come with it), he wanted to be certain the pivotal trial would win, will win. That he chose a certain way, but that way was going slower than expected even if the outcome was assured (in his view). This approach, which I can't say I wholly disagree with, of trying very hard to be certain and risking the perfect being the enemy of the good or really good, is denigrated when you say nothing, or say it cryptically or poorly.

And when you let time elapse. The merits of your approach are denigrated by your silence and the passage of time.

There truly may be things that indeed are wrong, like, you know, checkpoint inhibitors are going to cure melanoma so there's no need for PV-10... But here's some math that could be more right than wrong (at least I believe so):

- Let's assume Provectus' pivotal melanoma Phase 3 trial has treated about 20 patients (range: say, 15-25) by the end of October among the current six sites recruiting as denoted on CT.gov, and

- Let's also assume sites can recruit one patient per site per month (if not more) as a result of the proposed protocol refinements (subcutaneous lesions now can be target ones), which become effective at month-end when a handful of European Union (and maybe Australian) sites could come online (yes, WAGs) -- to make the math easier, I'm simply saying just add per month the number of sites that are then recruiting to 20.

How long would it take to arrive at 45 (15 events), 60 (20) or 81 (27) patients, from here on out? Again, depending on assumptions and math, three to six months?

Starting a dialogue with shareholders to say some of the above would help, and giving realistic timing that isn't that hard to model with reason also would help too.

I'm led to believe... Should the share price drop below six cents, trading would be suspended until the ticker was moved to over the counter, after which trading would resume. Setting aside administrative matters and process, the ticker would be up-listed after the share price achieved the $0.20-level (although I am unsure for how long, etc.).

So, in addition to giving management and the independent board members discretion over more shares outstanding, which has merit, shareholders are being asked to given them discretion over a reverse split (whether one is necessary or not), which given their lack of experience, knowledge, intelligence and intent might be a bridge too far.

Biological basis (October 11, 2016)

Updated below: 10/11/16.

Provectus issued a press release and made an associated 8-K filing related to potential changes in the clinical trial protocol of its pivotal melanoma Phase 3 study, "Announces Poster Presentation on PV-10 at European Society of Medical Oncology 2016 Congress Now Available Online." The ESMO 2016 trials-in-progress poster is here.

I though the poster's conclusion's focus on PV-10's branding as an ablative immunotherapy was nice.

|

| Image source |

"In particular, allowing patients with primarily or exclusively subcutaneous melanoma (that is, melanoma below the skin surface) and those with larger tumors should not significantly affect the biological basis for our phase 3 study, but could substantially expand the fraction of patients with locally advanced disease that can participate in the study."Possible refinements are noted at the bottom of the screenshot of the relevant portion of the poster, below:

|

| Click to enlarge. Image source |

Lesion size. Previously, work by Australian compassionate use program (special access scheme) site Princess Alexandra Hospital noted smaller lesion size (and younger age) were predictors of response; however, investigators were dealing with small lesions: " In the current study, lesion size was also found to be predictive. Of the five patients who achieved a complete response, the average lesion diameter was 3 mm compared to the cohort average size of 6.3 mm." Lesion size of upto 5 cm is comparable to fellow intralesional drug T-Vec/Imlygic's upper lesion size treatment range; prescribing information is here.

Subcutaneous injection. Recurrent, satellite or in-transit locally advanced cutaneous or subcutaneous melanoma metastases comprise AJCC Stage IIIB, IIIC or Stage IV M1a with no active nodal metastases. T-Vec's pivotal Phase 3 melanoma permitted subcutaneous disease to be injected as target lesions (for purposes of determining response). Provectus has allowed subcutaneous disease to be injected from the beginning; however, the proposed change of permitting subcutaneous lesions to be TARGET lesions.

The company had been hesitant to permit subcutaneous lesions as target lesions because study photography would not be particularly compelling for lesions that are not visible on the skin surface. Tumor measurement approach RECIST does not require photography. In this case, radiologic assessment of subcutaneous lesions that are target ones would allow RECIST determination. Provectus expects to permit subcutaneous lesions to be target ones because a significant portion of patients with locally advanced disease have primarily subcutaneous disease. The current criteria appears to unnecessarily exclude patients that have the same biologic characteristics as those currently allowed.

As such, there is no change to the biological basis of the trial. Eric noted to me: "The disease characteristics and natural course are equivalent to these patients vs those eligible under the current criteria. Thus, the biology is the same."

According to Provectus, anecdotally, sites like MD Anderson (Dr. Merrick Ross, MD) (zip code 77030) and Huntsman Cancer Institute (Dr. Robert Andtbacka, MD) (84112) were recruiting 10-20 patients per site per month for IL agent Allovectin-7's pivotal melanoma Phase 3 trial. Target enrollment of that trial was 390, and there were 88 study location.

Takeaways:

- If these potential changes are proposed to and acknowledged (accepted) by the FDA, it would appear to me Provectus certainly has further increased the patient population within Stage IIIB-IV M1a to which PV-10 is applicable, for both faster/greater trial enrollment and label purposes,

- I cannot see an interim data readout analysis by year-end; hence, the indications of a readout in Q2 may (and probably) have merit; see An Incomplete Story (October 5, 2016) below, and

- Taking an optimistic viewpoint, the potential increase, within the category, of patients with measurable disease presents an interesting "twist." More patients with more measurable or target disease would permit more event generation, and thus potentially increase enrollment and increase the rate of event generation (in those patients whose disease progresses in the control arm, and then who would crossover into the treatment arm).

Updated (10/11/16): He was against management before he was for Peter before he was for Eric before he was against Eric? I am "hearing" the potential protocol changes displayed at ESMO 2016 should be implemented, but what do I know...?

CTAs. Eric noted on the ESMO 2016 poster that clinical trial agreements for the pivotal melanoma Phase 3 trial were underway with/at European Union sites, and Russia was added to anticipated geographies, compared to what was on the ASCO 2016 trials-in-progress poster.

Amendments. Multiple amendments to trial protocols, particularly smaller ones and refinements, like one of the ones Eric modeled the Phase 3 trial after seem par for the course, particularly in a fluid (oncology) industry setting.

In-line. H/t InvestorVillage poster canis_star who linked to a melanoma combination therapy poster at ESMO 2016 of an IL agent (CAVATAK, an oncolytic virus) and anti-CTLA-4 drug ipilimumab. The poster included a helpful table comparing other IL agents like T-Vec and HF-10. CAVATAK + ipi produced an in-line response rate with a better safety profile.

|

| Click to enlarge. Image source |

How many such events would have to occur in the control arm for an interim assessment to be performed? Eric went into a long discussion regarding the null hypothesis (I have written about this extensively in relation to triggers visible and invisible, clinical trial math, etc.), where one assumes both arms -- the control arm, and the treatment arm -- behave the same.

The figure could be anywhere from 0 to 75 (i.e., 225 ÷ 3), but the null predicts it would be about 27 events (81 ÷ 3), since the study is randomized 2:1 and it is assumed one third of the events would occur in the comparator arm (per the null, it is assumed 54 events [81 ÷ 3, then × 2] would occur in the PV-10 arm). If the number of events in the control arm is much less than 27, PV-10 is not faring well, whereas if the number is much greater than 27, things are going well for PV-10.

So, does the company need a trial enrollment of somewhere around 81 patients or so (randomized on a two-to-one basis), or maybe a little to a lot less (like 45-60, a number I've thrown out there before), if there is a large imbalance in events between the two arms), in order for an interim analysis to be conducted? If I speculate enrollment is in the teens to about 20, it would seem clear to me the protocol change to allow subcutaneous target lesions is/was crucial. How long do six current sites plus future sites at some point(s) in time get Eric an additional 25-60 patients? It's just a race to the data and a question of how much is left when the time comes.

I am struck by... (October 10, 2016)

Updated below: 10/10/16 {twice}.

a. Following data releases at ESMO 2016 (it continues until tomorrow), the further drop in Bristol-Myers' share price, which as of this writing was below $50. When I wrote August 30th blog post The Day Big Pharma's Earth Stood Still, which Bristol-Myers locations visited a few times, the price was over $57. The stock last saw $75 on August 4th.

b. The messaging of journalists reporting on the checkpoint inhibitor competition between Merck & Co. and Bristol-Myers. See, for example, Endpoints' John Carroll's October 9th "Merck’s glorious victory in lung cancer marks a Russian winter for Bristol-Myers" and Forbes' Matthew Herper's October 9th "Bristol's Opdivo Disappoints in Lung Cancer, Losing Ground To Rival Merck."

c. Bristol-Myers now saying anti-PD-1/PD-L1 drugs and agents are the same.

|

| Image source |

|

| Image source |

e. The lack of separation of non-small cell lung cancer survival curves between Keytruda + chemotherapy, and chemotherapy alone.

f. Merck & Co. having no pivotal (registration) combination therapy trials (aside from utilizing chemotherapy) for Keytruda in gastrointestinal cancer.

g. Non-immunogenic (versus immunogenic) being further divided into immune exclusion and immune ignorance, which correspond to Provectus CTO Dr. Eric Wachter, PhD's points regarding immune suppression and tumor non-immunoactivity. See Kobayashi Maru (October 4, 2016) below.

Updated (10/10/16).1: h. I'm not struck by this, but it's worth noting here.

|

| Image source |

|

| Click to enlarge |

|

| Click to enlarge. Image source |

Updated (10/10/16).2: i. Either or both of independent board members Al Smith and Jan Koe not tapping out by now, given how in over their heads they must find themselves (e.g., not understanding what to do, not knowing what to do, etc.) for the purported experience they bring to the table as directors.

For example, they should (i) instruct Provectus COO and interim CEO Peter Culpepper and CFO John Glass to smartly reduce monthly cash burn (likely much more than Peter has done, an is willing to do or capable of doing), (ii) require Peter and John to create a 6-month (illustrative timeframe) monthly cash burn projection (I don't believe Peter did such a crucial and prudent exercise during his tenure as CFO) that the board then would require Peter/John to update every two weeks or month, (iii) swiftly evaluate (it would not take too long) and then dismiss (as appropriate) several of Peter's lower quality vendors (with eye to replacing them or having Peter do the work), and (iv) assist company CTO Dr. Eric Wachter, PhD with (i.e. wrest control from him) communications of what clinical and preclinical work Provectus is undertaking and when to communicate it. There are several other straightforward things they could do to right the ship as they race towards the data. There also are several shareholders willing to replace Smith and/or Koe to effect these changes.

j. How challenging must it be for the board to deal directly with Eric when you don't know the questions to ask him, and you don't understand what he is saying in the situations when he answers you. The board has deferred to Peter, who continues to defer to Eric in regards to communicating what, and what when. If you don't know or understand what what is, how can do determine what what is important to what degree, and when you might communicate each relevant what?

An Incomplete Story (October 5, 2016)

Updated below: 10/6/16 {thrice}, 10/7/16 and 10/8/16.

Provectus issued a press release and made several SEC filings today related to the company seeking (i) an increase the number of authorized shares of common stock, par value $.001 per share from the current figure of 400 million to 1 billion, (ii) to raise up to $21 million from existing shareholders (record date not yet determined) via the issuance of common stock (price not yet determined) that also would include warrant coverage (amount not yet determined), and to effect a reverse stock split between 1-for-10 and 1-for-50. Filings included an 8-K (of the press release of the above), a proxy filing/Schedule 14A (a shareholder meeting on November 14th) and a registration statement/S-1. There is much to read in the various components of the filings that were made today, and several topics to analyze and address, such as the potential delisting of the company's common stock from the NYSE MKT.

Stepping back for a moment, it would seem simple and straightforward to observe that Provectus has until November 14th (or by when votes comfortably could be made, such as at least 48 hours before the voting deadline) to compellingly convince existing shareholders (of whatever record date the company decides) to buy into/buy up the rights offering through the issuance/generation of news and/or release of data, whatever this item or these items may be. It could not convince non-tradeable warrant holders through several iterations of the warrant exchange program(s). Make the case this time and Provectus could well pave the way to one or more catalysts for itself and the share price. Fail to make the case, and that row becomes exceedingly tough to hoe (to reach its hoped or desired for end).

Updated (10/6/16).1: Some further thoughts this morning, with thank yous to the numerous people to whom I spoke, texted and e-mailed yesterday about all things Provectus:

- Is the global pharmaceutical industry market for oncology setting up well for Rose Bengal and PV-10? I believe so,

- Can Rose Bengal/PV-10 potentially achieve pathologic complete response (ablation) so as to induce a potentially robust immune response in the body (immunotherapy) against cancer? I believe so,

- Thus, can PV-10/Rose Bengal potentially improve, and potentially dramatically so, cancer patient outcomes around the world? I believe so,

- Can these outcomes be achieved across some, many or all solid tumor cancers? I believe so,

- Do data drive deals? Of course,

- Does Provectus have enough data? Not yet,

- Is there a better sense of timing around such and other data? I believe so,

- Have I been wrong about former and current management, and former and current independent board members, in context? Certainly,

- Have I been right about the drug substance (Rose Bengal) and/or drug products (PV-10, PH-10)? Near-certainly yes, and

- Would I support the board and management's recommendations for the proxy vote? Yes, in context; however, the board of directors requires new independent members (as part of a clear transition facilitated by the fundraising and vote) who have proper intent, sufficient competence and constant vigilance to oversee and direct management to and over the finish line for the benefit of shareholders.

It is not yet clear to me whether to buy shares prior to and/or participate in the rights offering, as I believe there should be news flow of one sort or another that may positively influence the details of the offering*. I may do one or the other or both.

Updated (10/6/16).2: More thoughts follow:

- It will take time for the SEC to make Provectus' S-1 effective. I would be surprised if the rights offering is completed sooner than early- to mid-December. As I noted under Kobayashi Maru (October 4, 2016) below, and setting aside the share price-related listing requirement, given enough cash and stockholders' equity at third quarter's end, the fundraising could have been extended towards the end of the audit/audit reporting cycle (i.e., early-December).

- But, Provectus now has a share price-level listing concern. The only benefit for shareholders to agree to (vote for) a reverse split is to mitigate this concern, remain on the NYSE MKT, and not provide a distraction to the company and its story as the quarter unfolds. Otherwise, what's the point of a reverse split?

- Do I really want to allow Provectus management and its independent board members to have discretion and control over more authorized shares and a reverse split decision (as sought in the recently filed proxy)? Each of them, in their own special and respective ways, has demonstrated himself to be lacking as a decision-maker,

- We can argue about most any assumption as it relates to most any analysis; however, I do not believe one can argue about math (or the ideal gas law). For someone pursuing a CFA charter, his analysis does not bode well for passing Level I (a good reply is here). In the end, analysis matters,

- InvestorVillage poster Warlord is, I believe, a Provectus shareholder from/in Denmark, along with other Danish shareholders, and a worthwhile read. At least four helpful and potentially insightful points were made in a recounting of a local meeting with management (ESMO 2016 this week will be held in Copenhagen):

Updated (10/8/16).5: Warlord continues to provide helpful information from the Danish investor meeting.

- The end of the Phase 1b combination therapy trial of PV-10 and pembrolizumab for advanced (solely Stage IV) cancer is [could be] 1Q/2Q17. As an aside, I believe preliminary data will be presented at HemOnc Today Melanoma 2017 in late-March,

|

| Image source |

Updated (10/7/16).4: On Provectus' August 10th 2Q16 business update call Eric said, in regards to the timing of the availability of interim Phase 1b study results, "Okay, Bill. I will try to address those in the order that they were asked. It’s possible that we would report some initial data from the Phase 1 b portion of the study this year. If that is the case, it would be some form of interim data. It is much more likely that will be in the first half of next year, picking up into the 2017 oncology cycle. If we submitted an abstract today to a major meeting, that wouldn’t be recorded until sometime late in the fourth quarter, so we have to acknowledge that it’s likely that a public readout of those data would not be until sometime in the first half of next year. That is not to say that in the context of confidential discussions with potential corporate partners, there may not be some opportunity to share those data with partners, but that is also, again, pure speculation at this point." Understanding that Eric guided "possible" (by year-end) during the summer, it may well be that he meets this "expectation."

- The interim pivotal melanoma Phase 3 trial analysis is [could be] 2Q3Q17. It would seem to me, as I have recently thought about this topic, that aside from an imbalance of events themselves between the two arms (PV-10; chemotherapy or oncolytic virus), PV-10 could now have to beat fellow intralesional (IL) agent T-Vec on the primary endpoint of progression-free survival (PFS), which takes (requires) time (to elapse), and

- There may be another amendment to the Phase 3 trial protocol to further ease patient enrollment restrictions, and

Updated (10/7/16).4: I'd like to see the detail of these protocol amendments or changes that could substantially speed up enrollment. For now, however, as I reevaluate enrollment rates, my estimate of patients already recruited to this trial may be less than 20 as of "now."

|

| Click to enlarge |

Updated (10/8/16).5: I agree with InvestorVillage poster STARLIGHT66 regarding the timely communication of potential or prospective protocol changes. Eric very, very likely (undoubtedly) could have communicated this on the August 10th 2Q16 business update call. I continue to believe adult supervision is required for management (because they continue to embarrass themselves as business leaders), and Provectus' independent board members are no adults (although many children are far smarter and more responsible). As an aside, it might be nice if STARLIGHT66 was his usual helpful and informative self, was less cryptic and less Maxim/Network 1'ish, and did not take posts down.

- There is an expectation of certain news flow in advance of the shareholder meeting to approve the proxy vote proposals (November 14th) and the rights offering (early-December).

Updated (10/6/16).3: Some final things I think:

- I think any license deal for PH-10 would have to envision the completion of an end-of-phase 2 meeting with the FDA to address the issue of toxicity, or in PH-10's case the near-complete if not complete lack thereof. I would imagine any pivotal psoriasis Phase 3 trial protocol already has been developed, perhaps such as a variation of the mechanism of action study (A Phase 2 Study of Cellular and Immunologic Changes in the Skin of Subjects Receiving PH-10) and/or the prior randomized controlled trial (Randomized Study of PH-10 for Psoriasis),

Updated (10/7/16).4: Deal comps on upfront dermatology/psoriasis payments: $115 million, global/US, July 2016 (licensee: AstraZeneca, licensor: Leo Pharma, tralokinumab/brodalumab); $50 million, Europe, July 2016 (Almirall, Sun Pharma, tildrakizumab); $50 million, U.S., March 2016 (Dr. Reddy, Xenoport, XP23829);...$80 million, global, September 2014 (Sun Pharma, Merck, tildrakizumab)

Updated (10/8/16).5: It's not clear to me whether Provectus' expectations have been socialized with prospective licensees (buyers and sellers in potential transactions each have their own expectations of course); however, the point of making a cursory list of comparable (dermatology/psoriasis) transactions' upfront payment component is to potentially note the seriousness of the advisor's consideration of PH-10's possible clinical worth in that market. There could/would be other components, such as regulatory and/or commercial milestone and royalty payments.

- I think it's interesting that Rose Bengal as I-131 was used for evaluating jaundice in children,

- I think it would be very difficult to envision either Al Smith or Jan Koe, both independent Provectus board members, continuing in their roles for much longer if the company is ever to make good on its promise and potential. To different extents, in different situations, each director has been, is, and more than likely would continue to be in over their heads,

- I think a good board member is as much an a@$-kicker of management as he or she is a cheerleader of them,

- I think it would be a great idea for management to hold an investor conference call to discuss the rights offering (e.g., an explanation of the structure and how it could or would be priced, the rationale for undertaking it [as obvious as that sounds, hearing it directly from management is meaningful in my view], potential timing, etc.). It also would be a good idea for the company's CTO Dr. Eric Wachter, PhD to use the same call to provide potentially non-overlapping (with the subsequent 3Q16 business update call) commentary of various aspects of work under his purview,

- As I previously noted, the value proposition of the current rights offering is no different than the prior warrant exchange programs. Management must do their best to make it compelling and a "no brainer" for existing investors to [over-]subscribe. To not do so (understanding that some things are within their control and others are not) is a clear cut case of business malpractice, and

- I think it's just a race to the data and, for existing shareholders like me with a much higher cost basis than the current share price, a question of how much is left when the time comes.

Updated (10/7/16).4: I lied. I have more things I think. I believe there is a decision-making tug of war about presenting the expanded Phase 1 liver data at either ESMO Asia 2016 (Singapore) in December and the Asian Pacific Association for the Study of the Liver (APASL) (Shanghai) in February 2017.

Updated (10/8/16).5: For only the third time (I believe) in the company's too-long history, a third party might issue a press release about Rose Bengal. How crazy is that (given, for example, the joint patent combination therapy portfolio with Pfizer)? Prior releases would have been Moffitt Cancer Center's August 2013 "Single Injection May Revolutionize Melanoma Treatment, Moffitt Study Shows" and Boehringer Ingelheim (China)'s July 2015 "Boehringer Ingelheim and Provectus biopharmaceutical companies signed letters of intent - the two sides will cooperate to promote melanoma and liver cancer research in new drugs in Chinese mainland, Hong Kong and Taiwan."

I believe Provectus is expecting "media awareness," although I think Warlord is being illustrative about the New York Times.

Visitor. Merck & Co. (Kenilworth), via a Merck Europe router (I now am using better geolocation tools), recently visited the blog again, this time traversing September 2016 blog posts like September 26, 2016' SITC 2016: Intralesional injection with Rose Bengal and systemic chemotherapy induces anti-tumor immunity in a murine model of pancreatic cancer.

Updated (10/8/16).5: For only the third time (I believe) in the company's too-long history, a third party might issue a press release about Rose Bengal. How crazy is that (given, for example, the joint patent combination therapy portfolio with Pfizer)? Prior releases would have been Moffitt Cancer Center's August 2013 "Single Injection May Revolutionize Melanoma Treatment, Moffitt Study Shows" and Boehringer Ingelheim (China)'s July 2015 "Boehringer Ingelheim and Provectus biopharmaceutical companies signed letters of intent - the two sides will cooperate to promote melanoma and liver cancer research in new drugs in Chinese mainland, Hong Kong and Taiwan."

I believe Provectus is expecting "media awareness," although I think Warlord is being illustrative about the New York Times.

Visitor. Merck & Co. (Kenilworth), via a Merck Europe router (I now am using better geolocation tools), recently visited the blog again, this time traversing September 2016 blog posts like September 26, 2016' SITC 2016: Intralesional injection with Rose Bengal and systemic chemotherapy induces anti-tumor immunity in a murine model of pancreatic cancer.

|

| Image source |

- Inhibitor: Pembrolizumab for patients with advanced prostate adenocarcinoma: 13% objective response (no complete responses), measurement by RECIST 1.1; NCT02054806 and

- Stimulator: Pfizer's OX40 for patients with advanced cancer: 4% objective response (no complete responses), measurement by both RECIST and irRECIST; NCT02315066.

Consider Provectus CTO Dr. Eric Wachter, PhD's references to cutaneous and uveal melanoma under Kobayashi Maru (October 4, 2016) below. Consider also the references to these melanoma indications in the October 3rd GEN article by Dr. Jeffrey Buguliskis, PhD entitled "The Future of Immunotherapy Is Not Stopping at the Checkpoints." I followed up with Eric on my original questions to him below. Was he saying, say for uveal melanoma or another suitable example (like cutaneous melanoma), that the primary and potentially PV-10-injectable site could/is immunogenic, while the secondary site such as on the liver could/is non-immunogenic? How much "power" could be gotten from injecting an immunogenic site versus injecting a non-immunogenic one? Has Provectus undertaken any of that kind of analysis? I would imagine one would like to hit both "sets" of tumors, like for cutaneous melanoma, those on the skin and those on the liver, for the best benefit, but I also could imagine the nature and definition of immunogenicity belies the idea of an immune response emanating from the PV-10 injection.

Think about this in regards to uveal melanoma: "Uveal melanoma (UM) is a rare disease that can be deadly in spite of adequate local treatment. Systemic therapy with chemotherapy is usually ineffective and new-targeted therapies have not improved results considerably. The eye creates an immunosuppressive environment in order to protect eyesight. UM cells use similar processes to escape immune surveillance." {source}

Clearly for cutaneous melanoma the mets to the liver are relatively non-responsive to IO agents (PD-1, etc.) whereas the lung mets are highly responsive. As I noted earlier, we are still learning. This is to be determined, several projects are in the works since this is, for obvious reasons, an area of great interest in the oncology community.

canis_star also posted intralesional (IL) agent HF10 + anti-CTLA-4 drug ipilimumab in patients with advanced melanoma (at ESMO 2016); best overall response 39.5% (11.6% complete response) with measurement by irRC (NCT02272855).

Melanoma, IL and Rose Bengal key opinion leader Dr. Sanjiv Agarwala has discussed this pairing, among others.

|

| Click to enlarge. Image source |

The following table discusses additivity and synergism:

|

| Click to enlarge |

Prior data for HF10 and ipi had suggested synergism between the two (despite no response for HF10 in melanoma as a monotherapy). That HF10 and ipi are synergistic is consistent with the belief fellow oncolytic virus T-Vec is synergistic with ipi, while only being additive with anti-PD-1 drug pembrolizumab.

Visitor. Roche (Basel, Switzerland) recently visited the blog again, this time traversing October 23, 2014 blog post More of Better > More or Less of Worse, exiting images here and here.

Visitor. Roche (Basel, Switzerland) recently visited the blog again, this time traversing October 23, 2014 blog post More of Better > More or Less of Worse, exiting images here and here.

Kobayashi Maru (October 4, 2016)

Updated below: 10/4/16.

H/t InvestorVillage poster rmgillis for linking to an animation of PV-10's mechanism of action from Provectus' old website (pvct.com; the new website is provectusbio.com). A "screenshot video" of it is below:

Prostate cancer. In an October 3rd TargetedOncology article by Lisa Miller entitled "Prostate Tumors May Not Be Immunologic, Says Expert," I note:

"Perhaps prostate cancer is not an immunologic solid tumor because it is not as hypermutated as other cancer types, Slovin said. A signifcantly higher proportion of somatic mutation frequencies are found in bladder cancer, both lung adenocarcinoma and lung squamous cell carcinoma, and melanoma—the most hypermutated of 27 different cancer types tested.

Even after genomic profiling and various clinical trials, it is still unclear why the few patients with prostate cancer who do respond to immunotherapy treatments stand apart from the majority of patients who do not. However, Slovin noted that there are a few exceptional responders in this area who have durable responses lasting several years.

[Dr. Susan F. Slovin, MD, PhD of Memorial Sloan Kettering Cancer Center] noted that prostate cancer immunotherapy trials have not shown any abscopal effects or T-cell response potentia- tion either, further adding to the expectations that the prostate may not be immunologic. The possibility remains, however, that with a boost to the immunologic signals of the organ with other immunotherapy strategies or combinations, the immune system could indeed respond in time."I asked Provectus CTO Dr. Eric Wachter, PhD about this (slightly edited below for readability).

Three main theories are being applied when IO is less effective than expected: (i) T cell exhaustion, (ii) immune suppression, and (iii) a non-immunoactive tumor. The last often is attributed to low mutation rate. This may be true, but the immune system is very sophisticated so I suspect (iii) is accompanied by one or more of the others. Pfizer's Dr. Craig Eagle, MD teaches that the immune system can be trained to recognize tumor, addressing at least (ii) and (iii). Uveal melanoma (melanoma from the retina) is non-immunogenic when metastatic to the liver. It is unlikely that this is due to mutation load. Similarly, cutaneous melanoma metastases in the liver are relatively non-responsive to IO. So I think Slovin has a point, but I don't know whether it is a major or minor point. We are still learning!What's good for the goose is good for... National Institute for Health and Care Excellence (NICE) guidance for T-Vec, published September 28th:

"Approximately 10-15% of patients have troublesome locally advanced or 3c/M1a disease. Whilst these patients are likely to benefit from the current NICE-approved agents, they are also the group of patients who will benefit from TVEC. Increasing treatment options for patients (ie targeted therapy and immunotherapy) have already been shown to improve survival in advanced melanoma, so it is logical to further expand new treatment options for eligible patients." {my underlined emphasis}Takeaway: Addressable market for PV-10 as a monotherapy upon its approval for locally advanced cutaneous melanoma.

Cash concerns. A quick 'n dirty cash burn analysis I shared with another shareholder..."By the time of the second Maxim raise, around the end of August, I imagine Provectus had around $1.9-2.1 million on hand. They ended June with about $4.9m. The company may have current cash burn rate of about $1.5 million per month (April was exceedingly high at $1.85 million, while May and June averaged about $1.51 million). Provectus raised about $5.4 million (net), giving it around $6 million as of the beginning of October. The NYSE MKT listing threshold is a total stockholders' equity (TSE) of $6 million, which means adding about $4 million to the cash figure at any point in time (i.e., assets minus liabilities, ex-cash). The stockholders equity could be about $10 million (although I need to get a better handle on the impact of the preferred stock on TSE, and as such this analysis doesn't reflect that). We can do the math. It is possible, but how probable is another question, that the company could go through the end of December and still have about $1.5-2 million of cash left and, maybe, a TSE of $5.5-6 million, especially if the company has reduced cash burn."

Shares outstanding. Some people believe the anti-dilution provision of the August Maxim-led raise, when tabulated, would require Provectus to seek additional shares because the amount the company currently has authorized but that are not yet issued is insufficient. I currently do not subscribe to that view, based on Baker Donelson's opinion letter and comments by management on the topic.

Updated (10/4/16): I believe management is being consistent in what they say about the above topic to whomever asks. Provectus of course requires shareholder approval for any in increase the number of authorized of common (and/or other class[es] of) shares. My point, however, was the company's outside counsel provided a legal opinion based on Provectus having enough shares as is. I find it hard to believe (but am open to being wrong) the law firm (irrespective of how aggressive or conservative they are, and they are too conservative in their work for/with Provectus for my tastes) would not have included some kind of caution in said opinion regarding what otherwise is an open-ended share issuance commitment as a function of a certain future share price formula calculation, because there can be no guarantee a share increase at some point in the future, if sought, would receive shareholder approval.

Perhaps a larger issue, for met at least, is over a public discourse of this topic. Existing and prospective shareholders of course must always do their own due diligence...always. You can't [always] trust management. There always is benefit to sunlight, and to proper disclosure as well. Saying some things publicly and possibly other potentially inconsistent things privately, despite useful and insightful analysis from time to time, how much better are you than Maxim and Network 1 Financial?Predictive and Prognostic (October 3, 2016)

Under Catching on to Craig about a decade later: "Intratumoral Immunization: A New Paradigm for Cancer Therapy" (April 17, 2014) on the blog's Archived News I page, I had written: