In investment management, there are several measures of risk-return (aka risk-reward), including alpha, beta and Sharpe Ratio (see, for example, Forbes' Measuring Risk With Alpha, Beta and Sharpe Ratio by Richard Loth). Most investment professionals and retail investors do not outperform the market. Most investment funds, mutual, hedge or otherwise, after fees and expenses (and, more often than not, before too) do not generate alpha. Alpha measures the value an investment manager adds to his or her fund portfolio. Warren Buffett, Jim Simmons, Ray Dalio, etc. established their reputations by generating lots of alpha for notable periods of times. Beta measure volatility. A beta greater than 1 means a portfolio (or security) will be more volatile than the market (less than 1 means less volatile, and equal to 1 means the same volatility). Many hedge funds generate high beta; that is, when the market goes up they go up higher, and when the market goes down they go down more. Some funds are low beta ones; they go up less when the market goes up and go down less when the market goes down. "Investors would most likely prefer a high alpha and a low beta."Sharpe Ratio measures risk-adjusted performance, and "...tells investors whether an investment's returns are due to smart investment decisions or are the result of excess risk."

While far from a perfect analogy, many or most of the pharmaceutical industry's oncology drugs generate beta. Few, if any, generate real alpha. Most have forgettable Sharpes. Layer on the cost of treatment (i.e., mutual fund costs or hedge fund fees and expenses), only the most effective drugs (i.e., the very best investment managers) deliver a compelling patient (i.e., investor) value proposition.

As I have written before on the blog before, and continue with the above analogy:

Pharmaceutical Risk = Safety,

Pharmaceutical Return = Efficacy, and

Pharmaceutical Fees & Expenses = Treatment Cost.

PV-10 for melanoma (or any of the solid tumor cancers for which it likely should have great potential) is like a very high alpha, very low beta, very inexpensive-to-own fund.

Safe. Efficacious. Broad spectrum of use. Low cost.

Byline: Demonstrates Risk of Clinically Relevant Drug-Drug Interactions with Rose Bengal is Low

Key Statement:

"The published research indicated that the risk of PV-10 causing clinically relevant drug-drug interactions is likely minimal."

"Sorafenib is a competitive inhibitor of cytochrome P450 (CYP) drug metabolism enzymes and is reliant on the UDP-glucuronosyltransferase (UGT) pathway for efficient clearance. CYP and UGT enzymes help to biotransform small lipophilic drugs like sorafenib into water-soluble excretable metabolites."

"As we discuss our clinical results with regulatory authorities, we continue to be intensely committed to building all sections of the prescribing information for a future package insert for PV-10."

The paper's Discussion section helps to place the conclusion of low risk of clinically relevant or significant drug-drug interaction in context, and discusses what is known, what can by hypothesized, what is not known, and what requires or deserves more work. The paper and the PR begin to reveal more of PV-10's orthogonality (drug-drug interaction) potential. My posts on orthogonality are here, here, here and here.

Orthogonal, as you know, refers to the the idea of perpendicular, non-overlapping, independently varying or uncorrelated items. Two lines at right angles to each other are perpendicular, or orthogonal. X, Y and Z axes conventions reflect axes perpendicular (or orthogonal) to each other.

I think there are at least two key takeaways from this work and PR. First, clinical trial outcome. Sorafenib, co-developed and co-marketed as Nexavar by Bayer and Onyx Pharmaceuticals (acquired by Amgen in August 2013) is the standard of care for the treatment of advanced hepatocellular carcinoma. The company currently is running an expanded liver cancer Phase 1 trial comparing sorafenib (cohort 1) to PV-10 plus sorafenib (cohort 2). Sorafenib/Nexavar is not a very good drug, but it remains the go-to-solution for physicians for this disease.

By demonstrating low clinically relevant drug-drug interaction, all or most of the difference in efficacy between cohort 1 and 2 should be attributed, positively (more efficacy in 2 than 1) or negatively (less efficacy in 2 than 1), to PV-10. The trial is permitting a single intralesional injection of PV-10 in patients with either recurrent hepatocellular carcinoma (HCC) or cancer metastatic to the liver. Success data (higher efficacy in cohort 2 v. cohort 1), likely measurements should include overall response (complete, partial, stable) of injected tumors, would inform the FDA and impress Big Pharma, particularly if they are even remotely close to what was demonstrated for locally advanced cutaneous melanoma. Provectus has not updated the market on its liver cancer Phase 1 trial save this old information from its current website presentation.

Click the figure to enlarge it.

This biochemistry work published today is very useful for when the company shows its expanded liver trial efficacy results and analysis to the FDA and Pfizer, er, Big Pharma.

"The drug, which is particularly effective on late-stage kidney and liver cancer, costs approximately $69,000 per year in India, so in March 2012 an Indian court granted a license to an Indian company to produce to the drug at a 97 percent discount" (quote source, and for the two quotes below, is here) "Nexavar costs approximately $96,000 per year in the United States, but Bayer assures “western patients” that they can have access to the drug for a $100 copay." [Bold and underlined emphasis is mine.] "In an interview with Bloomberg Businessweek, Bayer CEO Marijn Dekkers said that his company’s new cancer drug, Nexavar, isn’t “for Indians,” but “for western patients who can afford it.”"

A generic version of Nexavar may hurt Bayer/Amgen. PV-10 reducing Nexavar to near obsolescence certainly won't kill Bayer/Amgen, but the companies certainly will miss the sales (and that will impact earnings to an extent balance sheet financial engineering cannot fix). For example, in the U.S., $96,000 per year for Sorafenib/Nexavar, or a $20,000-30,000 "one shot, one kill," single use (multiple injections, if necessary) 100 mL vial of PV-10. The issue of treatment cost, in the U.S. and around the world, is far from resolved. The market opportunity for liver cancer for PV-10 still remains a very, very large addressable market times PV-10's likely very large market share times some price per treatment.

The lack of drug-drug interaction makes possible the combination of PV-10 and other drug therapies (chemotherapy, immunotherapies). That's, um, Pfizer and Provectus' joint patent application (Combination of Local and Systemic Immunomodulative Therapies for Enhanced Treatment of Cancer), which should be fully approved later this year.

This biochemistry work published today, assuming expanded liver cancer Phase 1 study data is consistent with other PV-10 liver and other cancer indication tumor results and more work conducted on combination therapies including PV-10 is successful, should open very significant market opportunities for Provectus and PV-10

A Bloomberg article earlier in the week discussed "breakthrough status" for drugs to "...have closer communication with top FDA staff to move drugs for serious diseases to market more quickly, potentially with data from an expanded Phase 1 trial." Breakthrough status would be more applicable to Provectus' liver work than the company's melanoma work.

I asked management if Provectus submitted a request for Breakthrough Therapy designation for PV-10. As with the SPA process, it is unlikely the company will publicly discuss submissions for this process. Rather, should management secure this designation for PV-10, the market will read about it via a company PR.

The Celsion deal essentially was a license transaction call option owned by

Hisun. Positive ThermoDox results were necessary for Hisun to exercise its

option to further negotiate an eventual license transaction for China, Hong

Kong and Macau. While Hisun is not one of the top pharmaceutical

companies in mainland China (according to 2011 market caps), based on the table (below) I previously published, I must acknowledge I previously was incorrect about suggesting or implying the no name-ness of Hisun, which launched a joint venture with Pfizer in September 2012, Hisun-Pfizer Pharmaceuticals Co.

I am a big fan,

proponent and practitioner of process. Good process doesn’t make a bad deal

good, but can make a good deal great. In the case of Provectus, management’s

good process could make a good China deal a great one.

Success in China for

Western companies appears based on working with that country's federal government as

a partner, rather than acting antagonistic, ignoring it or not involving it in

one's process.

Engaging in business in China as a foreign entity can be a very challenging endeavor for the largest of multinational corporations, let alone a small biotechnology company like Provectus. Two issues usually arise, the positive resolution of which typically bode well for success: the presence or lack of government support and, depending on the industry sector and business application, sufficient or insufficient intellectual property protection.

Many companies have enjoyed success because of a fruitful and “eyes wide-open” relationship with the Chinese state. When I traveled there a few years ago, that was the message of the CFO of Intel’s Dalian-based organization: see and seek the government as your partner, not your opponent. Just ask how successful Google and Paypal, among others, have been in trying to thwart or circumvent the Chinese government.

A nanotechnology company in which I am a very active shareholder spent a good amount of time, money and resources as it struggled to gain sufficient protection for its products, technologies and intellectual property as it hammered out a relationship with Foxconn to provide certain hand held electronics parts, componentry and coatings to several smartphone OEMs. The end consumer market was not China, but rather the company had to utilize China for manufacturing of products that ultimately would be sold in the U.S. and Europe. In the end, with the necessary support and promises of enforcement of its larger partners, the small nanotechnology company felt sufficiently comfortable and compelled to move forward in China. As a small company, time, money and resources are scarce and have to be adjudicated wisely, sometimes leading to nothing in the end.

A regional oncology deal in China between Provectus and a Chinese Big Pharma company has been in the works for several calendar quarters. The making of a deal emerged earlier this year in the spring. The company has worked through a process of due diligence, evaluation and negotiation to arrive where it is today.

In late-November, after a good amount of groundwork was laid, Peter traveled to China to meet with potential strategic partners and a bevy of government officials. There are multiple prospective partners for now (all of whom apparently are on the list of the top local pharmaceutical companies according to market cap above), and Provectus still is assessing the optimal one. On the government side, Pete and his intermediaries met, differently, with senior leadership of the office of the Premier of the People’s Republic of China, the Ministry of Health, the Ministry of National Defense, and the State Food & Drug Administration.

It appears he left China having established a good

working relationship with the government and government officials, a relationship that since has permitted Provectus and its advisors to now work with prospective strategic partners to finalize a license

transaction with a down-selected one on top-line terms and

conditions blessed by the government. Government support of Provectus, PV-10 and the business relationship between the company and the eventual strategic partner has been established, as I think has been the intellectual property protections afforded Provectus (with which I think management is mostly comfortable, or understanding or realistic of how the relationship might work in the context of their IP and its protection or lack thereof).

When Pete returns from his late-February trip to China (this assumes, of course, he does travel), he could bring home a signed deal and the contemplated upfront cash payment. These monies could fund the pivotal MM Phase 3 trial, to-be-finalized HCC (liver cancer) Phase 2/Phase 3 trial and, possibly, and one or two more Phase 1 trials, and contribute to other corporate use of funds.

An interesting situation arises, since the prospective partners all appear to be from the table above, with the China subsidiaries (WFOEs/WOFEs, which I think is unlikely, or acquired domestic subs) of key Western Big Pharma companies. I need to do more homework on this aspect or facet of a potential China deal.

Of course, Pete may not be successful. Deals break down or do not come to fruition for both substantive

and silly reasons. As cliched as the phrase is, only time will tell.

Though rare in the west, liver cancer is serious in Asia due to the prevalence of hepatitis B infection, which is as high as 10 percent in China's population of 1.3 billion people. Chronic hepatitis B infection can result in liver cirrhosis and liver cancer later in life..."But in China, even 10 percent of liver cancer patients would be an incredible number," Jiang said. In China, there are about 350,000 new liver cancer cases each year, or half of the world's total.

Provectus' share price has bounced above, below and around the 60-cent level following last month's terminated PVCTP "IPO." The SPA process has taken a toll on the stock in 2012. The market and life science investors' "certain" view the company will be forced to undergo substantial dilution to raise the necessary money for key and pivotal clinical trials (MM Phase 3, HCC expanded Phase 1 and Phase 2/3, pancreas Phase 1) weighs heavily on the share price too.

While management explored the opportunity to execute an "IPO," quarterly filings for Q2 and Q3 2012 indicated other avenues for seeking cash, such as from outlying geographic licenses (e.g., Australia, China, Japan, MENA).

2Q12 10-Q Filing -- Click on the figure to enlarge it.

3Q12 10-Q Filing -- Click on the figure to enlarge it.

The horse race, which previously had a dermatology transaction and geographic-specific oncology deal in the lead (unless a company-friendly "IPO" could have been had to overtake them; in hindsight, it could not), now might see (for now at least) an outlying geography deal for oncology assume the lead. I am not sure if Provectus is in the homestretch in this regard, but we could shortly see if it is.

In the past 12 months, Provectus' notable PRs included:

October 29, 2012: Provectus Presents Nonclinical Data on Antitumor Immune Response to PV-10 Immuno-Chemoablation (very key),

October 17, 2012: Provectus Pharmaceuticals Terminates Proposed Convertible Preferred Stock Offering (the failed IPO),

October 2, 2012: Provectus Pharmaceuticals Presents Final Phase 2 Melanoma Data at ESMO 2012 (key),

September 28, 2012: Provectus Pharmaceuticals' Patent Application Published for Combining Local and Systemic Therapies for Enhanced Treatment of Cancer (the joint Pfizer-Provectus patent app),

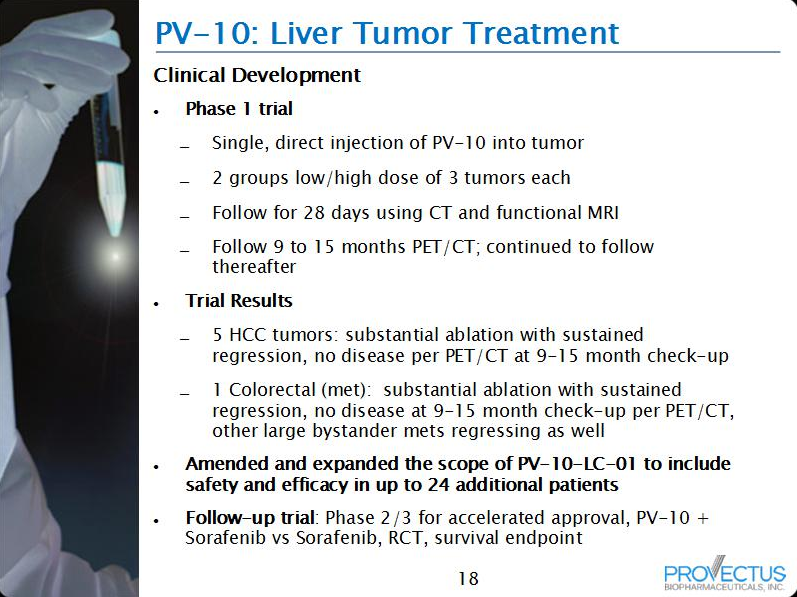

September 27, 2012: Provectus Expands Protocol for Phase 1 Liver Cancer Study (important),

June 26, 2012: Provectus Pharmaceuticals Presents Final Phase 2 on PV-10 At 2nd European Post-Chicago Melanoma Meeting 2012 on June 22, 2012 (visibility),

May 30, 2012: Doug Ulman, National Cancer Survivorship Advocate, Joins Provectus Pharmaceuticals' Corporate Advisory Board (a great get),

May 14, 2012: Provectus Pharmaceuticals Forms Independent Board to Meet Corporate Governance Requirements (an important corporate governance advance),

April 10, 2012: Phase 2 Data on Provectus's PV-10 to Be Presented at the HemOnc Today - Melanoma and Cutaneous Malignancies Conference on April 13, 2012 (visibility),

March 26, 2012: Intralesional PV-10 Treatment Leads to the Induction of Anti-Tumor Immunity (very key),

March 23, 2012: Mechanism of Action Data On PV-10 Demonstrates Therapy Induces Immunologic Response (very key),

March 19, 2012: Provectus Announces Top Line Phase 2 Data For PH-10 in Its First Randomized Controlled Psoriasis Study (important), and

January 18, 2012: Provectus Receives Guidance From FDA On Pathway to Approval for Phase 3 Trial of PV-10 For Metastatic Melanoma (important regulatory step).

As for the blog itself, readership has steadily grown.

Provectus released its 10-Q filing for Q3 2012 today. See here.

Quarter-over-quarter ("QoQ") -- Q3-over-Q2 -- monthly cash expenditure decreased by 23.3% (v. +3.6% Q2-over-Q1) to ~$745K per month (v. ~$969K). Ending Q3 cash was $1.8MM. The company raised ~$2MM in October (Q4). I think, based on some assumptions, that Provectus might have $3-$3.3MM of cash as of the filing date. QoQ R&D expenses decreased by 47% (v. +5.6%). QoQ G&A expenses decreased by 7.1% (v. +0.5%). Operating expenses include both cash and non-cash charges.

Click on the figure to enlarge it.

Management noted in the filing's MD&A section:"By managing variable cash expenses due to minimal fixed costs, we believe our cash and cash equivalents on hand at September 30, 2012, together with cash proceeds received during October 2012, will be sufficient to meet our current and planned operating needs until well into 2013 without consideration being given to additional cash inflows that might occur from the exercise of existing warrants or future sales of equity securities, although we may, in our sole discretion, direct Lincoln Park Capital Fund, LLC (the “Fund”) to purchase up to an additional $29,950,000 of our common stock per an existing agreement with the Fund." I would expect the company to continue to do private placements, raising money as necessary to maintain enough cash on hand to satisfy the external auditors, until such time as a dermatology deal or a mini-oncology deal or two are consummated to provide Provectus with the necessary cash to effect the pivotal MM Phase 3 trial. I think the minimum cash figure acceptable to the auditors is around $3-4MM, but this is not a hard floor or range; rather, having the ability to continue to support 12+ months of cash burn should be helpful in Provectus' representations.

The company expanded on their Q2 filing statement related to the strategic investment program: "We are seeking to improve our cash flow through both the licensure of PH-10 on the basis of our Phase 2 atopic dermatitis and psoriasis results, and the geographic licensure of PV-10 on the basis of our Phase 2 metastatic melanoma and Phase 1 liver results in certain areas of the world, as well as pursuing a strategic investment strategy, including equity sales to potential pharmaceutical and or biotech partners, and continuing with the majority stake asset sale and licensure of our OTC products as well as other non-core assets." This refers to the mini-oncology deal transactions the company is exploring in Australia, China, Japan and MENA.

I have written on this topic in the past. For example, see here. As I understand the lead indications and potential geographies of current discussions:

Fratres! Three weeks from now, I will be harvesting my crops. Imagine where you will be, and it will be so. Hold the line! Stay with me! If you find yourself alone, riding in the green fields with the sun on your face, do not be troubled. For you are in Elysium, and you're already dead! Brothers, what we do in life... echoes in eternity. -- Maximus Decimus Meridus in Gladiator

I want to:

Share my speculation about what I think happened towards the end of the third quarter and how it relates to the temporal nature of the PVCTP "IPO,"

Explain why I will invest a token amount of money in the "IPO" if it happens, and

Write about management's poker hand, the hand they have dealt shareholders, and how both of them might be played.

I think management was convinced the SPA would arrive by the end of Q3 and the PVCTP "IPO," which was supposed to have been in the right place at the right time, was being teed up to follow it.

As we know, Provectus and Peter have been working several financing options:

The "IPO,"

A dermatology license deal,

One or more geography-specific oncology license deals, and

A strategic investment from a Big Pharma entity like Pfizer as the sale of common stock at a premium to the share price (or, as mentioned above, an "IPO" led or co-led by a Big Pharma company).

Each of these has its own value proposition (i.e., pros and cons), but the propositions are temporal, having greater or lesser value as a function of time.

For example, the best option today for shareholders would be an optimally valued (i.e., net present value) and structured (i.e., upfront, milestone and royalty payments) dermatology or geographic-specific oncology license deal yielding an upfront payment sufficient to at least pay for the pivotal MM Phase 3 trial. Optimality, however, might be more likely to be achieved later rather than sooner, in November or December.

A sale of common stock to a Big Pharma company would be "more optimal" if the price at which these shares would be sold was much, much higher than Friday's close of $0.59, like at least $4. But why approach or ask a Big Pharma company like Pfizer for this kind of strategic investment unless you have or need to ask? In my view you ask after the SPA is in hand and if you determine (a) the PVCTP "IPO" is not feasible and (b) dermatology or mini-oncology optimality is later rather than sooner.

Up next is the PVCTP "IPO," which, for a certain period of time, provides attractive and pragmatic ways to begin driving company valuation dramatically upwards:

Attractively: A NASDAQ listing would facilitate new buyers, who could not buy the common while it remained an over-the-counter stock, and more national media attention from major journalists and reporters, who would not cover Provectus until it traded on a major stock exchange and was in Phase 3 trials.

Attractively: A smart IPO, led by Pfizer (and J&J or a life sciences investor like OrbiMed) and with a conversion ratio and warrant coverage good for existing common shareholders, would draw many more new buyers to the preferred stock listing itself over time.

Pragmatically: A $15-20MM raise at an acceptably high valuation, while creating dilution that a dermatology or a so-called mini-oncology license deal would not, fully funds the pivotal MM Phase 3 trial. There would be no need to force or rush dermatology or oncology deals, nor completely rely on them to commence the MM trial. The trial could start within 30 days of the SPA PR and move Provectus and its shareholders closer to the interim analysis of at least the first half of the trial's patient population.

A smart PVCTP "IPO" is a better temporal option in October than a dermatology or mini-oncology license. In November, it might not be.

Back to the SPA PR. It was the first domino to have fallen in a hoped for series of them, whether the next temporally best one was a license deal or the "IPO."

But the SPA did not arrive by the end of September, despite very ernest and serious expectations set to the contrary by folks directly interacting with the FDA. It is coming, but it was not nor is not here yet.

To compound these missed expectations were:

Shorting of the stock (end-of-September short interest was nearly 100% greater than the end-of-August figure) for whatever reason(s),

Selling of shares (September's monthly amount of traded shares was nearly double that of August's) for whatever reason(s), and

The PVCTP "IPO" process, and particularly the aspect undertaken by Maxim Group's retail banking side.

Th "alleged" sloppy "IPO" process was made much more so by "alleged" disgusting behavior by some Maxim retails reps spreading baseless "facts" about the "IPO's" details. I used "alleged" because, while Paul LaRosa from Maxim's capital markets part of business agreed Maxim reps should not have been saying what they were saying, the reps themselves probably would say they were doing nothing wrong. "Alleged?" I crack myself up.

The rep revenue model is predicated on the number of transactions they encourage and facilitate. The revenue model is not based on asset appreciation.

I now have what I think is a better handle on the increase in short interest, and will wait until October reporting dates to confirm this. In the interim, am I concerned? No. Am I annoyed and irritated? Yes.

There is the thought one very determined seller has been and is getting out of the stock. Could he/she/it have thrown in the towel for whatever reason(s)? Most likely yes. Does he/she/it know something we do not? I am betting my share ownership (note: no sales of any shares bought) the answer is "no."

Funds holding Provectus preferred and/or common shares have much different pressures than entities and individuals. The quarter-to-quarter reporting to investors and limited partners funds in this group (as opposed to a venture capital or private equity fund) are required to provide make it difficult to hold to an investment thesis because of complaints of poor performance by these very investors and LPs. Such theses turn into trading ones, if they did not start out as such. Did someone's patience runout? Probably.

So, here we are today, observing an IPO that keeps getting pushed out, from the week of:

October 1st to

October 8th to

October 15th to, likely,

October 22nd.

While the preferential path to financing might be a dermatology deal, the "IPO," for the reasons I presented above and others, is temporally better. I think, however, it needs an SPA PR to launch it, and I do not see the "IPO" occurring until after an SPA PR is issued. As such, if the "IPO" does not occur in October, management will probably pull the plug on it because other financing options would have become temporally better.

2.I got your initial public offering RIGHT HERE! (w/gesture)

If the PVCTP "IPO" goes off, I will participate in a very small way. I prefer buying common stock.

I work hard to maintain an objectively dispassionate investment case to buy and hold Provectus stock, but I am not always successful as emotion does creep in from time to time. I have an emotional attachment to this situation. Seriously folks, who blogs this much about one company or stock if they are not part of it? Participating in a token way in the "IPO" is something to add to "the box" that holds the collection of my life memories.

Emotion aside, however, the ROI from buying common stock should exceed the ROI of buying preferred stock (when compared together and presented as a choice of whether to buy the "IPO" or spend the equivalent amount of money buying the common stock), irrespective of what a Maxim retail rep tells you. Of course, you could always trust Chris Varick.

Let us make some assumptions to frame this analysis -- and please let me know if you disagree with my work below (as I am open to feedback and being corrected). I will toggle these later under certain circumstances to make some illustrative points. Nevertheless, the key assumption underlying my belief of a better common share ROI is that Provectus will not do a dumb IPO.

Let us assume you have $100,000 to either spend on the "IPO" or just buy common stock. In this analysis, you cannot buy both. Furthermore, since you do not know if and when the "IPO" goes off, you have to make a reasonably timely decision: wait for the "IPO" to happen or buy common stock before the SPA PR is issued. The SPA, which management surely knows they now have, should not affect the terms of the "IPO" but should increase the price of the common stock post-announcement.

Do you buy the "IPO" whenever it goes off, or do you buy common stock, say, starting Monday?

I assume about 150MM fully diluted number of shares of non-listed preferred and common stock, stock options and warrants. PVCTP deal terms then suggest some more shares. "As converted" means I used the conversion ratio above (i.e., 1) to convert the PVCTP shares and warrants on PVCTP shares into the appropriate but requisite number of common shares.

On an as converted basis, your $100,000 gets you (a) 35,000 PVCTP-derived common shares or (b) 166,500 common shares.

Let us assume the company is acquired for, among other things, a $1B upfront payment (i.e., the preferred shares you bought when converted into common stock or your common shares you bought are exchanged for your pro rata share of $1B) on December 17, 2013. Let us also assume the IPO still happens: you either participated in it, or you bought common shares and did not. I make this assumption only to simplify the analysis in some ways. If you buy common stock and the IPO does not go off (i.e., it is November and Provectus completes a license deal), the fully diluted shares outstanding figures remains at $150MM and your common stock ROI is higher.

Let us also assume you convert & exercise/sell your preferred shares and warrants, or your common stock, when the acquisition transaction occurs.

The outcome makes sense. A smart IPO implies a healthy valuation at which PVCTP "IPO" shares were sold and, thus, a substantial uptick (about an order of magnitude) from today's market capitalization. Under this scenario, one should of course buy the common stock, say, starting Monday, then wait and buy the IPO.

Hold on a second! Didn't your stock broker, er, Maxim retail rep "allegedly" tell you to flip the preferred shares and hold onto the warrants as "a lottery ticket?"

The flipping-your-preferred-shares ROI is less than the hold-your-preferred-shares ROI, which should be much less than the buy-common-stock ROI.

Maxim's "alleged" story only works -- that is, you make out like a bandit by indeed cashing in a lottery ticket -- if the conversion ratio and, to a lesser extent, warrant coverage is very punitive to existing common stock shareholders, such as 6- or 7- or 8-to-1 and 60%, respectively. That is, the "IPO" is a dumb "IPO."

A 2-to-1 conversion ratio (and, say, 50% warrant coverage), worse than my initial example above but far from punitive more than doubles your return from buying the "IPO;" however, one makes more money, again, by just buying common stock soon.

To be fair, a dumb IPO produces a result where buying PVCTP and eschewing the common stock is the better course of action.

3."Poker is not a game of cards played with other people, it is a game of people played with cards."

Right now, Provectus only needs money to literally keep the lights on and the water running (note: hyperbole). Fixed costs are low. The burn rate can be turned down and compensation deferred, with a focus on those activities, and whatever variable costs are associated with them, that drive value (e.g., the end-of-phase 2 meeting with the FDA for psoriasis, remaining toxicity study parameter elucidation, etc.) until money targeted for key, pivotal and other trial work is raised or obtained.

In this game of poker, management will play the hand they think they have the way they see fit. I think:

The company's hand is very strong,

Management thinks the hand is a royal flush (I think the hand is a royal flush, too),

Provectus has enough chips (cash on hand, and temporal cash needs) to play it well, and

Management will play it well (i.e., not raise money in a dumb way).

I am betting my share ownership on this. Of course, I could be quite wrong (note: the usual economist's conviction of "on the one hand, ..." but "on the other hand, ...," which is why we need more one-armed economists).

Now, what kind of poker hand do you think it is: a straight flush, four of a kind, a full house, worse or one that can be beaten? Which hand you have is up to you to determine. How you play it also is up to you.

There is no doubt of the battering the share price has taken since the beginning of September, let alone this year or over the last several years. I see it. I feel it. I understand it.

You got to know when to hold 'em, know when to fold 'em, Know when to walk away and know when to run. You never count your money when you're sittin' at the table. There'll be time enough for countin' when the dealin's done.

The company needs money, but not in the way the markets and most observers think Provectus does. Management has indicated they will do a smart IPO if they do one at all, and that raising money below $1.12 is not in the cards (pardon the pun). Anonymous wrote "[p]oker is not a game of cards played with other people, it is a game of people played with cards."

Playing your poker hand requires you to ask yourself how management will play their hand.

Disclaimer:This blog is neither intended to be nor is investment advice. The author of this blog (the "Author") is not a registered investment advisor. Under no circumstances should any content from this blog be used or interpreted as a recommendation of a trade or investment in Provectus Pharmaceuticals, Inc. Trading and investing can be hazardous to your wealth, health or both. Any investment decision must, in all cases and without exception, be made by the reader or by his or her registered investment advisor. This blog is only and strictly for educational and informational purposes. The Author may have a position in Provectus Pharmaceuticals, Inc. at any given time that is not disclosed at the time of publication. All opinions expressed by the Author are subject to change without notice. You, the reader, should always obtain current information and perform the appropriate due diligence before making any investment or trading decision. All efforts are made to ensure the information contained in the blog and/or a blog post is factual and accurate; however, the Author does not guarantee its accuracy under any circumstances.

I have been blogging a lot this month. There has been a lot about which to write. Month-over-month blog readership is up 30-60% across all major metrics (e.g., visits +46%, unique visitors +31%, pageviews +57%, average visit duration +41%, etc.). There will be as much or more to write about next month.

I think this there is an outcome much of the market currently does not see coming. I wrote yesterday about the market confusion regarding the PVCTP "IPO" and the current depression of the share price. At this point in time the market is about expectations. And those expectations, unfortunately, are not high going into ESMO 2012 and October.

We await regulatory clarity of the path to approval of PV-10 for metastatic melanoma (i.e., the SPA PR). We know the company requires money to conduct pivotal, key and other trial work (e.g., MM Phase 3, expanded liver Phase 1, liver Phase 2/3, pancreas Phase 1, psoriasis Phase 3, etc.). $15-30MM certainly substantially or fully covers this work. The market is unsure of the timing of the SPA PR. It also thinks the company will incur substantial dilution to achieve this fund raising.

What happens to market expectations of the company and common stock share price if the SPA PR is followed by a license deal announcement, whether dermatology or geographic-specific oncology, that provides most or all of the money above? This outcome causes a complete and utter upside surprise to the market, given what it thinks right now. The share price should blow upward because Provectus not only would have exceeded expectations but destroyed them through a non-dilutive "financing" event.

Below is my current take of the horse race of financing and "financing" options to secure monies for more trial work. I hope to update this more frequently as facts change and events transpire.

Provectus issued a PR today regarding the expansion of the liver cancer Phase 1 trial. More on the study can be read here. Changes to the initial study may be found here. This trial expansion is a necessary (required) "pre-study" to the eventual Phase 2/3, since safety has not yet been established using PV-10 and sorafenib. Expanding the initial trial, rather than running another Phase 1 trial, is more efficient since the expansion merely is an extension of an already approved safety study.

It seems that the plan is to present a series of good news next week in order to drive the SP above USD 2 and keep it there for the 5 days needed to be listed on NASDAQ. How do you see this?

Whether this week or next, a series of PRs (e.g., SPA, liver, ESMO, Moffitt, etc.) could drive the common stock share price onto the NASDAQ.

This news-driven common stock share price rise may be insufficient to effectively raise $20-30MM (via the existing shelf filing) to conduct pivotal, key and other trials. Getting onto the NASDAQ via the common stock is good and important, but a company's currency is its stock and dilution could be substantial or large (a $30MM raise at $2.50 per share is something like a 10-11% dilution).

The possibility exists this near-term series of news could be insufficient to push the common stock onto the NASDAQ. As a result, raising money becomes more expensive.

Management has maintained their first choice to minimize dilution and secure necessary trial monies, obviously, is to use significant or sizable upfront payments from a dermatology deal and/or mini-oncology deals (e.g., China, Australasia, etc.). Getting the right deal (e.g., valuation, upfront and milestone payments, royalty percent, etc.) in the context of completed and contemplated regulatory meetings and clinical data may take more time.

Life sciences players currently not in the stock understand Provectus needs to raise capital soon to run certain trials. These investors want to see how this money is raised -- i.e., understand the risk-reward profile -- before jumping into the PVCT pool: sell common stock, do a license deal or two, sell part of PVCTP to a strategic investor, etc. Once the picture is clear, investors should buy.

The PVCTP preferred stock offering vehicle, if led by a less price/valuation sensitive strategic investor, provide several benefits at once: raises valuation, facilitates effective fund raising, brings some or many investors off the sidelines, gets a Provectus security on the NASDAQ, goes toward reducing dilution, etc.

What is management thinking and what situation(s) are they currently facing?

Several thoughts about the PVCTP preferred stock offering vehicle have been bouncing around inside my head since it was first revealed through an SEC filing on September 4th. What was management's strategy for its utilization? Initial reactions by many were less than positive: fund raising, now?, more dilution?, how?, why?, when?, etc.

Provectus had established structural access to capital via the Lincoln Park equity line of credit and mixed securities shelf filing. Interest to invest by institutional and fund investors remained very strong. Fund raising at September prices would be painful of course, but there was no immediate need for capital.

Furthermore, management first spoke of a strategic investment strategy in its early-August 10Q filing, where strategic referred to Big Pharma companies.

The common stock could be used to facilitate a minority investment by Pfizer or J&J or another Big Pharma company, but the premium afforded PVCT.OB most likely would be limited on an absolute basis. Acquisitions tend to be viewed differently than investments by corporations. A 30%, 40% or 50% premium could work (typical of recent investment deals, suggesting a deal price of $0.90 to in excess of a $1.00 per share), but could a 1,000% premium be achieved (i.e., a $7 or thereabouts share price)? With time and news, the common stock could climb to the minimum $2 share price over 5 consecutive days and list on the NASDAQ as PVCT. But at current price levels, any fund raising would be more superficial than substantive (i.e., a "token" investment of several millions of dollars) rather than a signaling investment of of $20MM to do the pivotal MM Phase 3 trial. How long would the company have to wait for the common stock share price to rise to do a subsequent fund raising (assuming the initial one was a "superficial" one with Big Pharma) to sufficiently capitalize the trial?

I suppose a non-listed convertible preferred stock could be created out of the mixed security shelf specifically for a Big Pharma company. The preferred stock might garner a higher or much higher as converted common stock premium. The common stock might respond well as a result, with a Big Pharma company like Pfizer entering the capitalization table. But would that be enough to jolt Provectus' valuation? With time and news, the common stock could climb to the minimum $2 share price over 5 consecutive days and list on the NASDAQ as PVCT. Similar follow-up comments apply here, too.

If the company was not going to dilute its capitalization unnecessarily, how was PVCTP going to work and why?

Provectus never enjoyed a true or real IPO. In order to carry-out post-September 11th fund raising, the formerly privately held company did a reverse merger into a public shell. As a result, one of the biggest hurdles Provectus historically has faced and continues to face is being an over-the-counter stock.

So what does PVCTP really achieve? A lot, I think, and at different levels, too, from:

The more awareness and credibility that comes from a NASDAQ listing (relative to an over-the-counter listing), to

The monies to signal the intention to move forward with the pivotal MM Phase 3 and other key and pivotal trials (e.g., HCC expanded Phase 1, HCC Phase 2/3, pivotal psoriasis Phase 3), to

The significance of a lead corporate investor, who clearly could be an acquirer of Provectus, to

The addition of life sciences and other name investors as shareholders, to

A robust valuation [for PVCTP] out-of-the-gate, to

Reasonable but nowhere excessive PVCTP deal parameters (e.g., per share price, conversion ratio or price, warrant coverage), to

Facilitating greater mainstream media coverage by virtue of a NASDAQ-listed security together with a Phase 3 trial commenced, to

Eventually pulling PVCT.OB onto the NASDAQ and turbo-charging its trajectory thereafter.

Whew! That is a mouthful! In many ways, PVCTP, should the company utilize the preferred stock offering vehicle, is an IPO (forgiving the usage of the phrase given that PVCT.OB already publicly trades).

How does this happen? Here are my thoughts:

Lead investor: Pfizer, at a minimim.

There could be a co-lead.

For the round to be successful (to management and existing shareholders) a strategic investor like Pfizer, J&J or another Big Pharma company, who are much less sensitive to valuation and deal parameters (that also impact valuation) than financial investors, is required.

Other investors: 299 or more other lot holders

300 lot holders are required for PVCTP to list on the NASDAQ. That number very likely will include new life sciences, name and other investors as well as existing shareholders.

Offering amount (of PVCTP): ~$30MM

$15MM is the minimum amount to list on the NASDAQ.

An amount closer to $20MM at a minimum fully funds the pivotal MM Phase 3 trial. A higher number like $30MM provides more flexibility to fund other trials, like the HCC expanded Phase 1, the HCC Phase 2/3 trial, the Phase 1 pancreatic cancer trial and the pivotal psoriasis Phase 3 trial, and other pre-clinical and clinical work, etc.

I doubt the figures rises much beyond $30MM.

Demand for the offering also will play a role in the amount. If the offering is robustly oversubscribed, management may agree to a higher amount; however, oversubscription also plays a role in the determination of the valuation/per share price, conversion ratio and warrant coverage.

Valuation: $1B pre-money

A WAG, using actual and rumored historical datapoints. Maybe higher, or maybe lower.

Per share price (PVCTP): $1B pre-money

I think at least $5-6. $4 is the minimum price to list on the NASDAQ. Price obviously is influenced by supply (the amount of money management wants to raise for both operations, cosmetic and valuation reasons) and demand (over or undersubscription).

Conversion ratio: ?

I do not have a good handle on this yet, and therefore cannot really speculate.

1-to-1 would be nice; that is, each share of preferred stock would convert into one share or common stock. Maybe higher (i.e., each preferred share converts into more than one common share, which is less favorable to existing shareholders), but unlikely to be lower (i.e., more favorable to existing shareholders).

Warrant coverage: ?

40-50% is a datapoint I have been told. That is not bad, but the final figure may be higher (less favorable) or lower (more favorable).

Rights & Provisions: Customary

Per the offering prospectus supplement. There may be certain revisions or refinements if the vehicle is used.

Potential dilution: ~6%. Ultimately a single digit figure, so the final figure maybe higher or lower than the above number. Dilution would be based on or influenced by (i) the fully diluted number of existing shares, options and warrants (assumed for purposes of potential dilution calculation as 150MM), (ii) the number of shares (6MM) in the PVCTP offering, as well as warrant coverage (50%), (iii) the price ($5) and size ($30MM) of the offering, (iv) the offering's conversion ratio (1-to-1), and (v) whether the valuation is pre- ($1B pre-) or post-money (at this valuation level and given the offering amount, there is not much difference). Changes to my placeholder assumptions changes dilution. Much more information about the offering is likely going to be available mid-week.

An "IPO" is made more effective (better terms for the company, better on-the-day and post-"IPO" share appreciation and buying) the more demand there is for PVCTP. Demand comes from pre- and post-"IPO," PVCTP share price-moving news. If the vehicle is used, the "IPO" could occur during or around the week of October 8th (U.S. equity markets are not closed on Columbus Day), perhaps earlier like the end of the week of October 1st or later like the week of October 15th. Early- to mid-October makes sense because of the news going into and throughout the fourth and last quarter of this calendar year:

We await the SPA PR in Q3,

ESMO occurs as September becomes October, and PRs should reflect what is revealed by the company at this conference,

Craig speaks in early- and late-October about immunology and MOA,

More Moffitt data will be revealed and released,

Potentials in dermatology and/or mini-oncology should be consummated in Q4,

High profile peer review publications are expected, and

High profile mainstream media coverage is expected.

Management still may not utilize the PVCTP preferred stock offering vehicle. If they do use it, I think it will be in the manner I described above (or a derivation thereof) and will look forward to watching all of them ring the NASDAQ bell.